Asset Management

A Dream of Spring Amid Crypto Winter

Key Takeaways:

- With investors still digesting the latest crypto winter, amid the improvement in on-chain positioning, the crypto market continues to face conditions that may challenge the durability of any near‑term strength.

- A dream of spring may be on the horizon. However, in our view, attractive entry points relative to a year ago may not be enough to bring new attention into the market. Ultimately, each investor must assess current market conditions through the lens of their own objectives, risk tolerance, and market outlook.

- Adoption, one of the major long-term drivers of bitcoin's price, may see lower growth this year relative to recent years—even if the CLARITY Act is passed into law. That said, should the bill pass, it may offer a new narrative for the crypto market, on top of a relatively neutral macro backdrop.

House Stark in George R.R. Martin's A Song of Ice and Fire series was known for their motto "Winter is coming." This served to remind residents of Northern Westeros to be prepared for harsh times ahead. Following the 8x return that bitcoin experienced from its November 2022 low through its October 2025 peak, bitcoin fell into its fourth "crypto winter"—deep bear markets that have seen bitcoin's price fall by more than 50%, with altcoins experiencing much deeper selloffs.

In A Feast for Crows, a member of the Night's Watch said to Jon Snow, "Summer friends will melt away like summer snows, but winter friends are friends forever." New crypto investors may see cryptocurrency as a summer friend given the past six months, but for investors who have experienced multiple crypto winters, this latest was modest in comparison to others—which saw bitcoin's price fall over 75% from its peak. It has now been six months since this latest crypto winter began. While it may be too early for a very bullish perspective on the crypto market, even in the depths of winter there is always a dream of spring on the horizon.

We have published several reports to provide a framework for investing in cryptocurrencies. These reports addressed macro drivers for bitcoin and ether, an industry model and bottom-up method for evaluating cryptocurrencies, key debates, how to interpret on-chain data, and frameworks for valuing cryptocurrencies By incorporating all these methods, we have established our intermediate-term (six to 12 months) perspective on the crypto market.

Crypto market perspective

The winds of winter have been blowing since the crypto market kicked off a new bear market on October 10. From peak to trough, bitcoin experienced a 50% correction. Bitcoin appears to have bottomed near its 200-week moving average according to data from Bloomberg, which was also near its cost of production, according to data from Glassnode—levels at which past bear markets have bottomed, following bitcoin's previous three crypto winters. It is important to note that past performance is no guarantee of future results. On-chain metrics (data recorded directly on a blockchain) are starting to improve from very low levels, providing further evidence the bottom may be in. The macro environment is relatively neutral for cryptocurrencies. While positive earnings revisions in global equities may be supportive of a risk-on market, the primary driver of bitcoin is monetary growth, which presents a more neutral backdrop. Ultimately, the crypto market is a momentum market and likely needs a new narrative to reset that momentum—which could be the potential passing of the CLARITY Act.

In this type of environment, large-cap, foundational networks have historically outperformed the broader crypto market.

Risks that could impact this perspective include a sharp rise in unemployment or a sustained tightening of financial conditions given recent geopolitics in the Middle East. The bank and crypto lobby are currently experiencing a clash of kings as the two industries battle over the status of stablecoin rewards in the CLARITY Act. Depending on how long this issue takes to be resolved, should the midterms dramatically alter the current makeup of congress, priorities may shift from legislation to investigations.

Macro

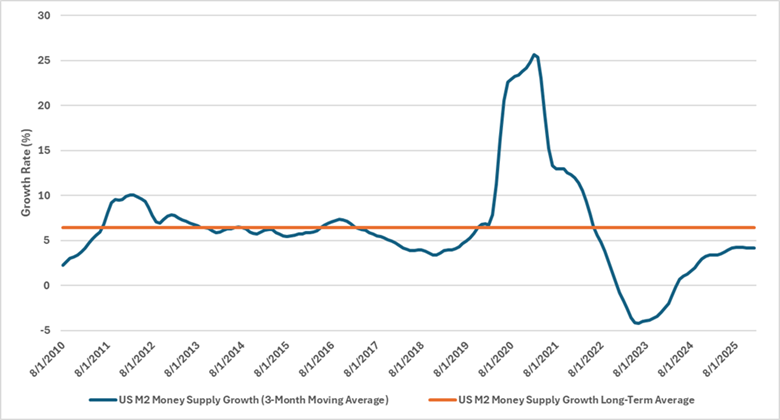

A weaker dollar and lower rates may be supportive in the back half of the year, which could result in an acceleration in M2 growth (M2 money supply is an estimate of liquid assets, including cash on hand, money deposited in checking accounts, savings accounts, and other short-term saving vehicles such as money market funds and certificates of deposit). M2 growth has been below its long-term average growth rate for several years. The M2 acceleration is positive for crypto, but this below-trend environment is unlikely to be supportive of a strong crypto rally. There do not appear to be any catalysts (large quantitative easing by the Federal Reserve, stimulus checks, very low interest rates) for a large acceleration in M2 in the near term. Any sharp rises in M2 that would result in any of these catalysts are likely to be preceded by downside volatility.

Investors appear to be discounting a near-term resolution to the recent conflict in the Middle East. If that were to change, the dollar may rise and expectations for rate cuts may be pushed out as investors seek position in safe havens like the dollar, and rising inflation expectations due to higher oil prices result in the Federal Reserve pausing or even hiking interest rates.

U.S. M2 growth has been below trend in recent years

Source: Bloomberg, Schwab Center for Financial Research. Data as of 3/6/2026.

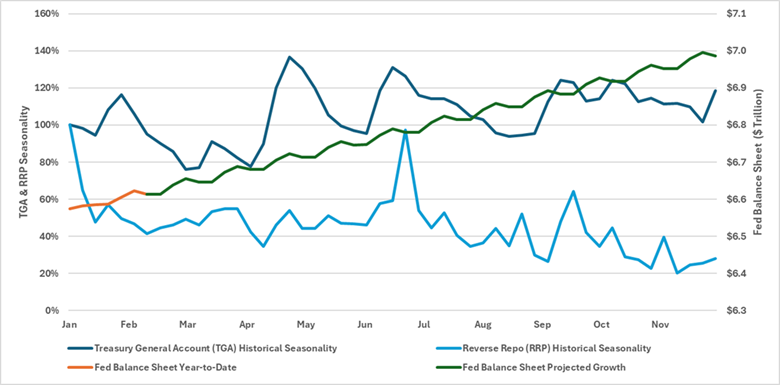

Liquidity has been tight ever since the reserves held in the Federal Reserve's reverse repo facility were depleted. These reserves reached a peak of over $2.5 trillion in 2022 as a result of COVID-19-era stimulus programs. Historically, banks have added excess deposits to the reverse repo facility at month-end and quarter-end, pulling them out in the beginning of the next month/quarter. The Treasury General Account follows seasonal patterns, at time injecting liquidity into the economy, while pulling from it at other times. On a positive note (for liquidity), the Federal Reserve is expanding its balance sheet, but the $40 billion a month expansion is still relatively modest compared to post-2008 global financial crisis history.

Core components of liquidity may follow historical seasonal patterns

Source: Bloomberg, Schwab Center for Financial Research, data as of 3/6/2026.

Note: Treasury General Account historical seasonality and Reverse Repo Historic Seasonality is calculated as the average month over month change for calendar years 2013-2025. Fed balance sheet year to date growth is January 2025-March 2025, Fed projected growth is March 2025-December 2025.Fed Balance Sheet Projected Growth is calculated as the annualized growth rate based on year-to-date balance sheet growth as of 3/6/2026.

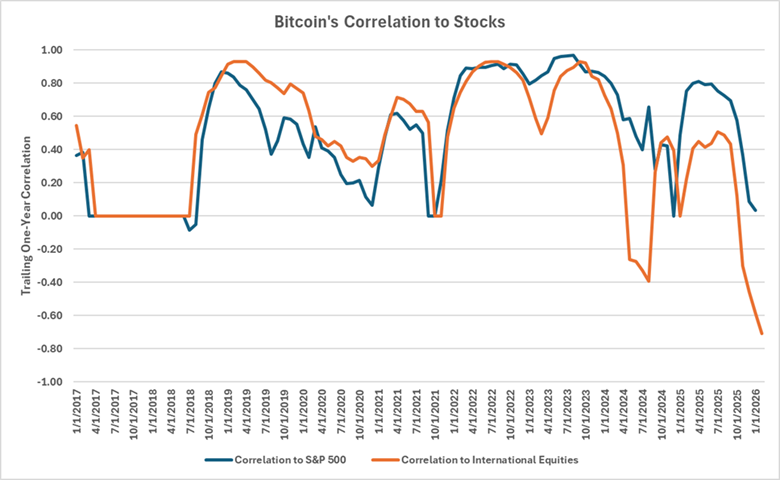

This year has seen earnings revisions move higher for both domestic and international equities, which historically is supportive of risk assets. The caveat is that bitcoin has been one of the areas that had outflows in recent months with the market rotating to new leadership. Given its falling correlation with equities, aside from a positive environment from risk assets, economic growth is not a factor for bitcoin's price. Ultimately, the macro backdrop is relatively neutral for cryptocurrencies, even if it is attractive for risk assets. Bitcoin's primary driver is monetary growth as opposed to economic growth.

While crypto investors may think a sharp acceleration in monetary growth would be positive, they would first have to come to terms with the fact that these actions typically follow risk-off events—which would likely pressure crypto markets. As Lord Petyr Baelish put it, "It doesn't matter what we want. Once we get it, then we want something else." If crypto investors get a sharp acceleration in monetary growth, they may realize they were better off without it.

Bitcoin's trailing 1-year correlation to equities is falling

Source: Bloomberg, Schwab Center for Financial Research. Data from 1/31/2017 to 2/28/2026.

Bitcoin is represented by bitcoin spot price. U.S. equities are represented by the S&P 500 index. International equities are represented by the MSCI ACWI ex. US index. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results. For illustrative purposes only and are no guarantee of future performance or success and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment. Correlation is a statistical measure of how two investments historically have moved in relation to each other, and ranges from -1 to 1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated.

On-chain metrics

On-chain activity may be increasing after more than six months of low activity. In summer 2025 most spot crypto transaction activity dried up, resulting in exchange-traded products (ETPs) being the source of new demand, while spot volumes and on-chain transaction fees were very low. Large digital natives had been selling (crypto investors who own over 1,000 bitcoin and have historically bought through spot markets) though they began buying again in late 2025, according to data from Glassnode as of March 9, 2026. ETPs have now seen several weeks of inflows according to data from Glassnode as of March 9, 2026. There are 11 ETPs included in this metric.

Digital Asset Treasuries (companies that use equity issuances and debt issuances to acquire cryptocurrency as a buy and hold strategy) continue to accumulate crypto in spot markets according to data from Glassnode as of March 9, 2026. There also appears to be less leverage in the crypto market according to data from Glassnode as of March 9, 2026.

Potential catalysts

The major catalyst we are watching for is Senate approval of the CLARITY Act. The House of Representatives passed the bill in July 2025, but it remains in the Senate. The passing of this bill might pave the road for institutional investors—many of whom have been hesitant to invest in crypto given the lack of regulatory clarity—to start investing. While some institutions have been investing through spot exchange-traded products (ETPs) passage could open the doors to institutions buying spot cryptocurrencies and using decentralized finance (DeFi) applications. Regardless of how fast that adoption occurs, it could provide a fundamental narrative shift, which is important in a momentum-driven market.

Midterm elections could also serve as a catalyst. While digital assets have bipartisan support in Congress, a major shift in the congressional makeup could impact the market perception of having a "crypto-friendly administration," as priorities in Congress could shift from legislation to investigations.

Meanwhile, "cockroaches" keep appearing in private credit markets. These isolated signs of distress recall JPMorgan CEO Jamie Dimon's remark on a Q3 2025 earnings call that "when you see one cockroach, there are probably more." If these issues do turn out to be more widespread than expected, and it is determined that banks have more exposure to bad debt than realized, this could serve as positive catalyst for the crypto market. Bitcoin was born out of the financial crisis, and it rallied in 2023 as several large banks went under. If there is a perception of broader financial contagion, it could benefit as a safe haven given its monetary authority is not linked to the traditional banking system. That said, bitcoin has not historically behaved as a safe haven in risk-off markets that are not related to financial contagions, and there is only one example where it may have behaved as a safe haven.

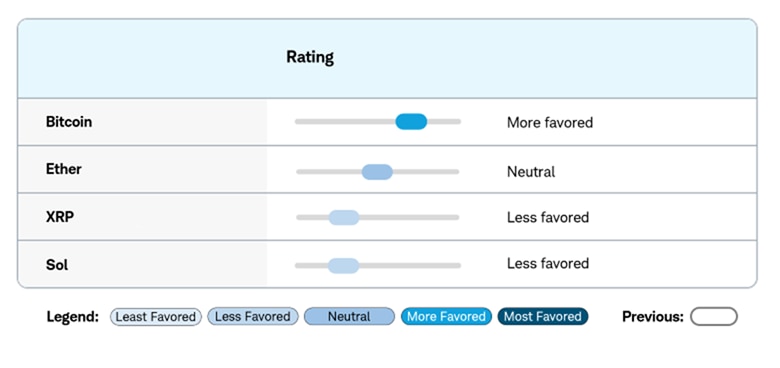

Below are our current views on four of the oldest and largest (by market cap) cryptocurrencies. These favorability views are our preferences for cryptocurrencies relative to their peers. The views reflect a six- to 12-month outlook and may change as markets evolve.

Nothing in this report should be interpreted as a recommendation to invest in cryptocurrencies or cryptocurrency-related products (including spot cryptocurrencies, crypto-related stocks, ETPs or derivatives). Investing in cryptocurrencies involves risk, including the risk of total loss of principal invested. Cryptocurrencies such as bitcoin, ether, XRP and sol are highly volatile, are not backed or guaranteed by any central bank or government; are not deposits; are not FDIC insured; are not SIPC-protected; and lack many of the regulations and consumer protections that legal-tender currencies and regulated securities have. Due to the high level of risk, investors should view digital currencies as a purely speculative instrument.

Cryptocurrency perspectives

Bitcoin: More Favored. We have a more favorable perspective on bitcoin relative to other cryptocurrencies. Altcoins experienced larger losses than bitcoin during the recent bear market. In past bear markets, the recovery has usually favored bitcoin. Once there is sustainable momentum in bitcoin, altcoins typically see more sustainable growth. Assuming passage of the CLARITY Act, relative positioning across crypto assets could shift, with larger networks potentially exhibiting greater resilience than the broader market. On March 31, 2026, bitcoin's price was 47% below its October 2025 all-time peak, according to data from Bloomberg.

The key risk for bitcoin would be a loss of confidence in the network. Most bitcoin investors perceive it as a store of value, and a change in that perspective could be detrimental to the value of the network.

Ether: Neutral. This could be the year that ether finally puts its "scalability" debate to bed. The upcoming Glamsterdam network upgrade follows last fall's "Fusaka" upgrade. Additionally, major financial institutions are beginning to accelerate the shift of real-world assets onto blockchains. Given Ethereum's leading market share and standing as the industry standard smart-contract blockchain, it is strongly positioned to benefit from increases in this activity. Alongside regulatory clarity, the potential for increased on-chain activity from tokenization comes at a time where ether is trading toward the low end of the trading range since January 2022, and reflects the weakness exhibited across the entire cryptocurrency market. The crypto market has rewarded more speculative cryptocurrencies over the past three years, up until the bear market in the fall. Perhaps investors will focus on ether's fundamentals in 2026. Given this, we have a more favorable perspective on ether relative to other altcoins, though we are still neutral on ether. As of March 31, 2026, ether was 58% below its all-time peak set in August 2025, according to Bloomberg.

The key risk to Ethereum is competition. Over the past few years, other smart-contract platforms have emerged that offer faster transaction speeds. If users were to move to one of these competitor networks, it could have a material impact on both the price of ether and the long-term viability of the Ethereum network. It also could be perceived to have "key-man" risk, as it is a founder-led protocol. If the founder, Vitalik Buterin, were to move on, investors could lose confidence in the network.

XRP: Less Favored. Historically during bear market recoveries investors have favored larger-cap assets. Since February, market leadership has tended to concentrate in larger capitalization assets, which may continue to play a more prominent role relative to smaller alternatives. That said, we are more skeptical on XRP in the long run due to the debate about what its key function is (a store of value or a smart-contract platform). It also does not have the leading market share in either of these categories, nor does it have industry standard network effects. That said, while fundamentals take the backseat to momentum driven investing, given its market structure and capitalization, cryptocurrencies such as XRP may be positioned differently than smaller tokens as market participants reassess risk exposure. As of March 31, 2026, XRP was 64% below its all-time peak set in July 2025, according to Bloomberg.

The key risk to XRP is related to its key debate. The XRP Ledger is neither the leading decentralized store of value, nor is it the leading smart-contract platform. In both categories it faces steep competition from other cryptocurrencies. If the market were to consolidate around the leading blockchains, XRP would be negatively impacted.

Sol: Less Favored. Most of the activity on the Solana blockchain comes from meme trading, the speculative buying that leads to viral popularity on social media. While stablecoins and tokenization of real-world assets are a growing use case, Ethereum is the market share leader for both of those areas. Given the steep losses experienced in meme coins during the crypto bear market, investors may be less motivated to engage in that behavior in the coming months. As a result, changes in transaction activity on the Solana blockchain could influence network usage metrics, which may factor into how market participants assess SOL over time. On March 31, 2026, Sol's price was 74% below its September 2025 all-time peak, according to data from Bloomberg.

The key risk for sol is that it is a utility token in competition with ether. If scaling solutions put the scalability debate to rest for the Ethereum network, network participants could question the need for building on top of the Solana blockchain.

Summary of characteristics

- Cryptocurrency

- Sector

- Industry

- Industry Standard Network Effects

- Leading Market Share

- Scalability

- Tokenomics

- Key Debate

- Trading Range

- Current Valuation

-

CryptocurrencyBitcoinSectorFoundational NetworksIndustryStore of ValueIndustry Standard Network Effects

✔️

Leading Market Share✔️

Scalability❌TokenomicsBelow AverageKey DebateQuantum riskTrading Range0.75x-2x Inefficient Miner ProductionCurrent Valuation0.8 Miner Production-

CryptocurrencyEtherSectorFoundational NetworksIndustrySmart Contract PlatformIndustry Standard Network Effects

✔️

Leading Market Share✔️

Scalability❌TokenomicsAverageKey DebateEthereum scalabilityTrading Range40x-70x Market Cap/"GDP"Current Valuation33x Market Cap/"GDP"-

CryptocurrencyXRPSectorFoundational NetworksIndustryStore of ValueIndustry Standard Network Effects❌Leading Market Share❌Scalability

✔️

TokenomicsBelow AverageKey DebateStore of value or smart contract?Trading Range0.1x to 0.4x Market Cap/Transfer VolumeCurrent Valuation0.2x Market Cap/Transfer Volume-

CryptocurrencySolSectorFoundational NetworksIndustrySmart Contract PlatformIndustry Standard Network Effects❌Leading Market Share❌Scalability

✔️

TokenomicsAbove AverageKey DebateExpand beyond meme trading?Trading Range20x-100x Market Cap/"GDP"Current Valuation18x Market Cap/”GDP”Summary of Schwab's cryptocurrency views

Note: These favorability views are our preferences for cryptocurrencies relative to their peers.

The views reflect a six- to 12-month outlook and may change as markets evolve. Views do not guarantee future returns and are not a forecast that an asset will rise or fall. They are not a recommendation. An unfavorable view does not mean the investment should be avoided, nor does a favorable view mean the asset must be included in a portfolio. An asset can be held for diversification. We suggest using these views as a guide, incorporating the accompanying rationale and other insights.

The views are positioned across a five-point spectrum: Least Favored, Less Favored, Neutral, More Favored and Most Favored. The Schwab Center for Financial Research (SCFR) sets these views. The investment approach incorporates a wide range of quantitative data and qualitative inputs that assess the current market environment relative to historical context. Past performance is no guarantee of future results.

A dream of spring

Jon Snow recalled a conversation with his father in A Storm of Swords. "It is a dream for spring though," Lord Eddard had said. "Even the promise of land will not lure men north with a winter coming on."

With investors still digesting the latest crypto winter, amid the improvement in on-chain positioning, the crypto market continues to face conditions that may challenge the durability of any near term strength. A dream of spring may be on the horizon. However, in our view, attractive entry points relative to a year ago may not be enough to bring new attention into the market. Ultimately, each investor must assess current market conditions through the lens of their own objectives, risk tolerance, and market outlook. Adoption, one of the major long-term drivers of bitcoin's price, may see lower growth this year relative to recent years—even if the CLARITY Act is passed into law. That said, should the bill pass, it may offer a new narrative for the crypto market, on top of a relatively neutral macro backdrop.

About the author

Jim FerraioliDirector of Digital Currencies Research and Strategy

Jim FerraioliDirector of Digital Currencies Research and Strategy