Asset Management

Gambler's Blues: Betting Isn't Investing

Key takeaways

- A long-term investment strategy means holding claims on productive assets and future cash flows, while gambling products are designed with a negative expected return for participants in the aggregate.

- Casino-like interfaces and prediction-market marketing obscure risk. The data show most participants lose over time, often more than they realize. The true cost is not just the losing bet, it is the compounded future value of the investment that was never made.

- When exploring the key differences between investing vs. gambling, know that in personal finance owning beats hoping and discipline beats speculation, with the long run belonging to those who invest in it.

There is a concept that has long anchored the philosophy of long-term wealth creation: owning. When you invest in a stock, a bond, or a diversified portfolio, you are acquiring a claim on future cash flows and productive assets—on the compounding engine of capitalism itself. You are not spectating. You are not wagering on an outcome and walking away with either a windfall or nothing. You are a participant in the ongoing enterprise of wealth creation, and that distinction matters more than it may seem at first glance.

Gambling operates on an entirely different logic. The gambler hopes. The investor owns. Both involve uncertain outcomes, and both require accepting the possibility of loss. But the underlying architecture of each is fundamentally different. A diversified portfolio of equities and bonds (and other alternative asset classes for some investors)—held through cycles and volatility—historically has rewarded patience and discipline with real, compounding returns, although past performance is no guarantee of future results. The house in casino gambling, a sportsbook, or a prediction market is structured to help ensure that, in the aggregate, it wins, and the participants, in the aggregate, do not.

A generation receiving the wrong message

This distinction has never been more important to articulate clearly. The youngest generation of investors is being inundated with the message that investing and gambling are essentially the same thing. The platforms and personalities delivering that message have worked hard to make the experience look and feel like a casino, emphasizing entertainment, instant gratification, and the thrill of placing a bet on nearly anything.

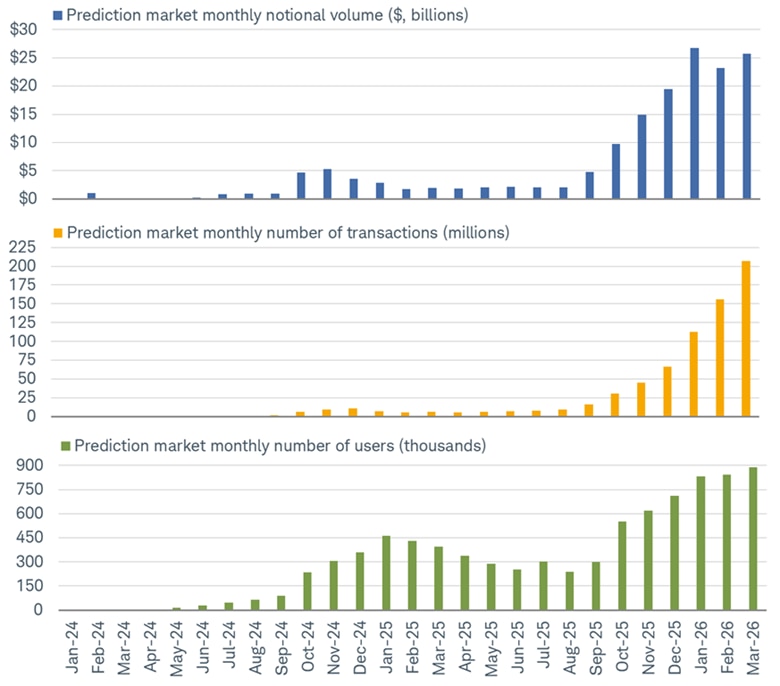

Prediction markets have grown exponentially, as shown in the chart below. It's not just monthly volume growth, which has risen to more than $25 billion since 2024 according to Dune. It's also total transactions, which have skyrocketed from about 240,000 to more than 200 million, while monthly active users have grown from about 4,000 to almost 900,000 (Dune). At the same time, a March 2026 report from Citizens JMP Securities covering the period from July 2025 to mid-March 2026, showed that prediction market users experienced higher losses than users of other gambling products, with a median loss of 8% compared to a loss of 5% for sports bettors.

Betting goes bonkers

Source: Charles Schwab, Dune, as of 3/31/2026.

The language often used to advertise these platforms is seductive. However, nearly absent from this messaging is any serious acknowledgment of the financial risks involved, or any honest reckoning with what the data actually show about outcomes.

This is not a minor cultural shift. Frankly, it is a financial literacy crisis in the making. UC San Diego Rady School of Management studied more than 700,000 online gamblers over five years through 2023, tracking digital payment records across 32 states. Researchers found that fewer than 5% of online sports gamblers have withdrawn more money from their gambling apps than they deposited. Let's flip that sentence: More than 95% of participants are net losers over time. This is not a feature of bad luck or poor timing—it is the mathematical inevitability built into these products by design.

The research is unambiguous

A landmark 2024 working paper by economists Scott R. Baker, Justin Balthrop, Mark J. Johnson, Jason D. Kotter, and Kevin Pisciotta—"Gambling Away Stability: Sports Betting's Impact on Vulnerable Households"—provides some of the most rigorous evidence yet of what is actually happening to household finances as online betting spreads across America. Using transaction data from more than 60 million Americans and analyzing behavior in roughly 230,000 households from 2010 through September 2023, the researchers explored the staggered state-by-state legalization of online sports betting following the Supreme Court's 2018 ruling to isolate the causal impact of gambling access on financial outcomes.

The findings are jarring. When online sports betting became available in a state, participation spread quickly and it did not slow down. Users who were net losers did not gradually learn their lesson and step back; instead they bet more. The research found not only an expansion among new users, but a pattern in which losing participants increased their wagering over time, a dynamic consistent with the addictive behavioral profile these platforms are designed, consciously or not, to cultivate.

Critically, the increase in gambling spending did not come at the expense of other entertainment, e.g., dining, concerts, or existing lottery and poker spending. It came at the expense of savings and investment. For every dollar directed toward sports betting, net investment in equities and other financial instruments fell by just over two dollars. The money flowing into these gambling sites was not discretionary leisure spending. It was likely wealth that would otherwise have been building toward long-term financial security.

The burden falls on those least able to bear it

Perhaps the most consequential finding in the working paper is the distributional one. The adverse effects of sports betting legalization were not evenly shared. They concentrated overwhelmingly among financially constrained households—precisely those for whom the loss of savings capacity carries the most devastating long-term consequences. Among this cohort, credit card debt rose, available credit fell, overdraft frequency increased, and net investment declined at rates far more severe than among their less financially strained counterparts.

This pattern has a self-reinforcing quality that should concern policymakers and practitioners alike. Research on the broader consequences of gambling legalization shows that it is associated with deteriorating credit scores and rising bankruptcies at the state level, according to the working paper. The households most likely to be drawn to the promise of a lottery-like windfall through online betting are, almost by construction, the ones with the least financial cushion to absorb the near-certain losses that follow. The platforms are frictionless by design—a bet can be placed in seconds, from a phone, at two in the morning—however, the financial consequences are anything but.

Impact of pandemic

To say that much changed in the aftermath of the pandemic is a simplistic understatement. Much of the post-pandemic era has been dominated by what Kevin coined as a "vibepression." For several years, there has been a depression in consumer sentiment and confidence metrics, despite a growing economy, impressive stock market gains, and several record highs in household net worth. The initial catalyst was the inflation spike in the immediate aftermath of the COVID-19 pandemic and Russia's invasion of Ukraine in 2022. For younger millennial and Generation Z folks who have never experienced significant price increases, it was a particularly shocking and strange environment—not least because the economy escaped a recession, home prices surged, and stocks recovered relatively well.

Then came the second phase: labor market struggles driven by the "Liberation Day" (April 2, 2025) tariff shock, as well as fears over artificial intelligence (AI) leading to mass unemployment for entry-level jobs. It's no secret that payroll growth has slowed significantly over the past year, and the unfortunate low-hire, low-fire nature of the labor market has meant that younger individuals have been disproportionately impacted. We know this given the much larger increase in the unemployment rate for 16- to 24-year-olds over the past three years, per Bureau of Labor Statistics data. Layer on the fears of AI taking a large share of jobs and you have a potential recipe for the vibes to get even worse.

At the heart of this issue is the fact that younger people today continue to see solid "hard" economic data—such as resilient gross domestic product (GDP), surging AI business capital expenditures, and low initial jobless claims—but they feel very little, if any, benefits. The traditional mechanism that translates better data into better sentiment has weakened, if not broken, as affordability has taken over as the chief issue. That has helped pave the way for more speculative efforts to build wealth, with the belief that it can happen faster compared to what are thought of as more traditional methods, like purchasing a house or investing in the stock market.

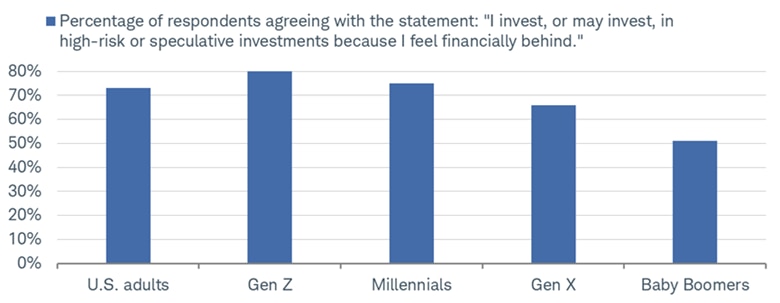

A recent survey from Northwestern Mutual—conducted by The Harris Poll—provides supporting evidence for that. As shown in the chart below, when asked if they agree with the statement, "I invest, or may invest, in high-risk or speculative investments because I feel financially behind," 80% of Gen Z respondents said yes. That compares to 75% of millennials, 66% of Gen Xers, and 51% of baby boomers.

Younger speculators

Source: Charles Schwab, Bloomberg, Northwestern Mutual's 2026 Planning & Progress Study, as of 3/9/2026.

As humans, we are prone to thinking in extremes, especially when it comes to markets. Of course, just because a high percentage of Gen Z investors say they are open to speculative investments to build wealth, doesn't mean they aren't also looking at more practical, less risky methods of investing. We just think there needs to be a clear, decisive distinction between investing and gambling.

Investors broadly need to be aware of how central things like prediction markets are to the vibepression. Unfortunately, there isn't yet evidence that the gap between hard and soft economic data is closing anytime soon; and now, with stocks struggling under the weight of the war in Iran, more speculative money-betting methods might look even more enticing to those who are seeing their portfolios struggle.

Risk of false equivalence

The conflation of investing and gambling is not entirely new. Critics of financial markets have made the comparison for as long as markets have existed. But there is a meaningful difference between a cynical critique and a deliberate business model built around blurring the line. Prediction markets and sports betting platforms are increasingly marketing themselves to the same demographic that the financial services industry is trying to reach with a very different message—one about the importance of saving, compounding, and investing for the long term. The competition for mindshare and wallet share is real and consequential.

For those who understand what they are doing and can afford to lose what they wager, responsible gambling is a legitimate form of entertainment. There is nothing inherently wrong with placing a bet on a football game, just as there is nothing inherently wrong with buying a lottery ticket. The problem arises when that activity is dressed up to look like a wealth-building strategy, when the risks are obscured behind engaging interfaces and social reinforcement, and when a generation of potential long-term investors comes to believe that outcomes are random regardless of what approach they take.

They are not. That is precisely the point.

We are in the outcomes business

There is a bright line between placing a bet on a football game and investing to potentially achieve better financial outcomes over the long term. That line is not arbitrary, and it is not merely philosophical. It is grounded in the mathematics of compounding, in the historical record of equity and fixed income market returns, and in the behavior of patient capital versus speculative capital across every market cycle.

Investing is a discipline. It involves goals, time horizons, risk tolerance, and the willingness to stay the course when volatility makes that difficult. It is not about excitement or entertainment, though markets certainly provide plenty of both, uninvited. Research makes it clear that dollars diverted from equity/bond markets and savings vehicles into betting platforms are not being redeployed into equivalent forms of risk-taking. They are being consumed…the expected value is negative…the platform wins. The bettor, statistically and on average, loses—and loses more than they realize. The true cost is not just the losing bet, generally it is the compounded future value of the investment that was never made.

Indulge a Charles Schwab "commercial"

At Schwab, we are in the outcomes business. Our purpose is to help investors build and help protect wealth over time—not to make the pursuit of financial security feel like a night in Las Vegas. The best thing we can do for the next generation of investors, particularly given the noise they are navigating, is to be unflinching about that distinction. Owning beats hoping. Discipline beats speculation. And the long run, as it always has, belongs to those who invest in it.

About the authors

Liz Ann Sonders