Asset Management

Preferreds Might Offer Value Amid Volatility

Key takeaways

- Yields for preferred securities, a type of hybrid investment that shares characteristics of both stocks and bonds, have risen recently, which might make them more attractive to income-oriented investors.

- Preferred securities, or preferreds, in the ICE BofA Core Plus Fixed Rate Preferred Securities Index tend to have higher credit ratings than high-yield bonds, but lower credit ratings than investment-grade corporate bonds.

- Preferreds can also potentially offer tax advantages. Many, but not all, preferred stocks pay qualified dividends that are subject to lower tax rates than traditional interest income. But it's important for investors considering preferreds relative to other investments to consider what type of account they'll be held in—taxable or tax-advantaged.

- Preferreds tend to be a bit more volatile than corporate bonds, so investors need to be prepared to ride out the potential ups and downs to earn those high-income payments.

Preferred security yields have risen recently and the risk/reward balance might seem more attractive to investors. As such, we currently have a more favorable view on preferreds compared to other fixed income investments.

Preferred securities are a type of hybrid investment that shares characteristics of both stocks and bonds that might offer higher income payments than many other fixed income investments. Preferreds have a few notable benefits, including:

- Attractive yields compared to investment grade and high-yield corporate bonds

- Potential tax benefits

While the higher yields they currently offer can be a nice benefit for income-oriented investors, those higher yields do come with additional risks, including:

- High-interest rate risk, where rising long-term yields could pull their prices lower

- Potential volatility given the ongoing conflict in the Middle East

But since they might currently be attractive to investors, we'll get into the potential ups and downs that preferreds offer.

Preferred securities generally offer high yields today

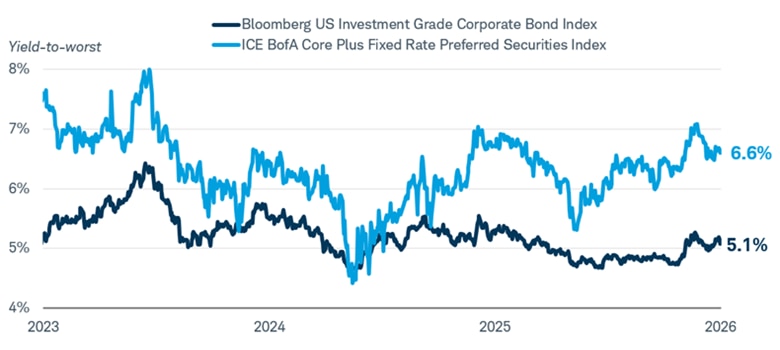

The ICE BofA Core Plus Fixed Rate Preferred Securities Index offered a yield-to-worst (the lowest possible yield a bondholder can receive from a bond with a call feature, barring default) of 6.6% on May 7, 2026, near the high end of its 15-year trading range. Since the index's inception in 2012, that yield hadn't risen much higher than 6% for a sustained period until 2022.

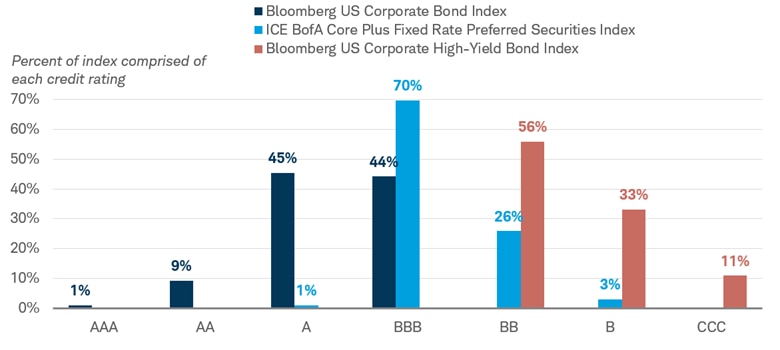

Preferred securities are issued by corporations, so it's generally appropriate to compare their yields to the yields offered by corporate bonds. The credit ratings for preferred securities tend to fall in between the credit ratings of the investment grade and high-yield corporate bond markets, with 70% of the preferreds in the ICE BofA Core Plus Fixed Rate Preferred Securities Index falling in the BBB category.

Credit rating breakdown of preferred securities, investment grade corporates, and high-yield corporates

Source: Bloomberg, as of 5/6/2026.

Most of the issues in the ICE BofA Core Plus Fixed Rate Preferred Securities Index are rated investment grade, although many are generally rated BBB, the lowest rung of the investment grade spectrum. Roughly 29% of the index is rated BB or below, or what is called "junk."

The average ratings of the Bloomberg US Corporate Bond Index—an all investment-grade index—tend to fall in the A and BBB range, with just 10% of the index rated AA or above. The average credit ratings of this index are higher than those of the preferred index.

The average credit ratings of the Bloomberg US Corporate High-Yield Bond Index are sub-investment grade, also "junk." However, more than half of the index is comprised of BB rated issues, which is at least at the upper end of the junk scale.

In short, the securities in the ICE BofA Core Plus Fixed Rate Preferred Securities Index tend to have higher credit ratings than high-yield bonds, but lower credit ratings than investment grade corporate bonds. How do their yields stack up?

Preferred securities tend to offer higher yields than investment-grade corporates, and recently that advantage has been widening. The average yield of the preferred security index has risen from just 5.3% in September of 2025 to 6.6% in early May, a more than 100-basis-point increase (a basis point is a unit of measurement equal to 1/100th of one percent, or 0.01%). It rose as high as 7.1% in late March following the increase in Treasury yields (which move inversely to Treasury bond prices) and stock market volatility following the start of the conflict in the Middle East.

Meanwhile, investment grade corporate bond yields have not risen as much. The average yield of the Bloomberg US Corporate Bond Index is up just 40 basis points since last September, from 4.7% to 5.1%. The yield advantage that preferreds offer above investment grade corporates has risen to 1.5%, or 150 basis points, compared to a modest 60-basis-point advantage last September.

Source: Bloomberg U.S. Corporate Bond Index (LUACYW Index) and the ICE BofA Core Plus Fixed Rate Preferred Securities Index (P0P4 Index). Daily data from 5/7/2023 to 5/7/2026.

Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

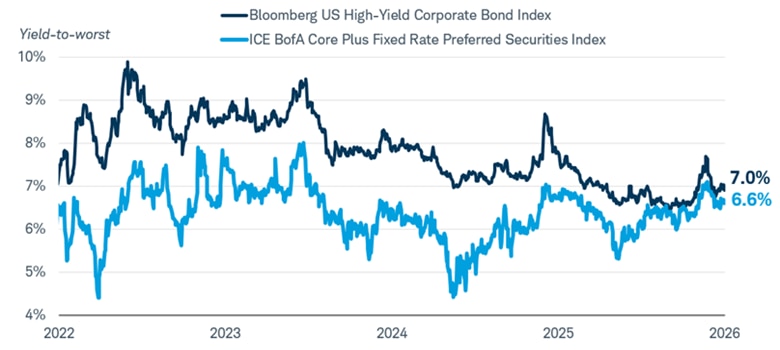

Preferreds appear attractive when compared to high-yield bonds as well. High-yield bonds typically offer higher yields than preferreds due to their lower credit ratings, but the difference between their yields has narrowed lately.

The Bloomberg US Corporate High-Yield Bond Index offered a yield of 7.0% in early May, compared to the 6.6% for the preferred index. The gap between high-yield bond yields and preferred yields has been relatively narrow for the past few months, that 40-basis-point yield advantage that high-yield bonds offer is the near its five-year lows.

As the chart below highlights, the average yield of the high-yield index is near its three-year low, while preferred yields are more than 100 basis points above their three-year lows.

Source: Bloomberg U.S. High-yield Corporate Bond Index (LF98YW Index) and the ICE BofA Fixed Rate Preferred Securities Index (P0P4 Index). Daily data from 5/7/2022 to 5/7/2026.

Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

Comparing preferreds to investment-grade corporates and high-yield corporates isn't an apples-to-apples comparison, but their yields appear attractive compared to both. The 150-basis-point yield advantage they offer above investment grade corporates is toward the high end of its recent range, and the narrow gap between preferred yields and high-yield bond yields suggests investors may be better off in preferreds given their higher credit ratings.

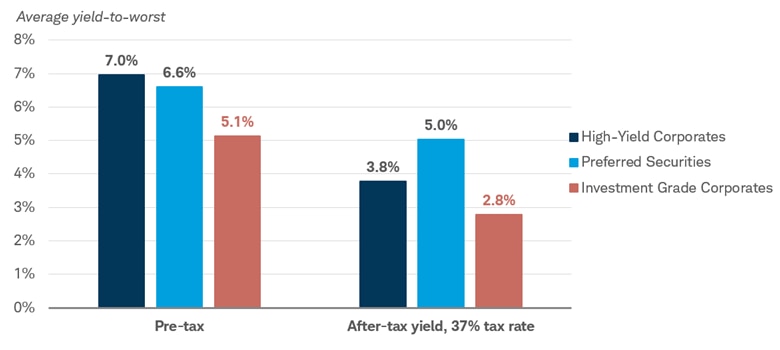

Preferreds can also potentially offer tax advantages. Many (but not all) preferred stocks pay qualified dividends that are subject to lower tax rates than traditional interest income. Investors considering preferreds relative to other investments should always consider what type of account they'll be held in—taxable or tax-advantaged. If they are held in taxable accounts, investors should also consider the after-tax yield.

Not all preferred stocks or securities pay qualified dividends—some pay interest that is taxed as ordinary income—so it's important to know what you own and what the tax consequences might be. Qualified dividends are generally taxed at 0%, 15%, or 20% rates, depending on income limits. Those lower rates can be an advantage for investors in high tax brackets because the income payments from most taxable bond investments are taxed at income tax rates.

The chart below includes the potential after-tax yields assuming the top federal tax rate of 37%, but preferreds that pay qualified dividends generally offer higher after-tax yields for tax rates below the top tax bracket as well. The after-tax yields will vary depending on each individual's situation.

Preferred securities can offer tax advantages

Source: Bloomberg, as of 5/7/2026.

Indexes represented are the Bloomberg U.S. Corporate Bond Index, Bloomberg U.S. Corporate High-Yield Bond Index, and the ICE BofA Core Plus Fixed Rate Preferred Securities Index. The "after-tax" column makes the following assumptions: Investment-grade corporate and high-yield corporates include a 37% federal tax, a 5% state tax, and the 3.8% ACA net investment income tax (NIIT); Preferred securities assume a 20% qualified dividend tax and the 3.8% Affordable Care Act (ACA) tax. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Schwab does not provide tax advice. Clients should consult a professional tax advisor for their tax advice needs. Past performance is no guarantee of future results.

There are risks with preferreds of course. They tend to be a bit more volatile than corporate bonds, so investors need to be prepared to ride out the potential ups and downs to earn those high-income payments.

Since preferreds have long maturities, or no maturity dates at all, their yields (and therefore their prices) tend to be influenced by the direction of long-term Treasury yields. If long-term Treasury yields rise, that could pull down the value of preferred securities. With inflation still high and expected to stay elevated, Treasury yields could rise modestly higher.

Preferreds have modest to high credit risk. The fundamentals of a given preferred security, and its ability to make timely income payments, matters. Preferreds also generally rank lower than traditional bonds in an issuer's capital structure. In bankruptcy, for example, corporate bond owners are generally paid before holders of preferred securities. If the economic outlook were to deteriorate, or if the corporate earnings outlook deteriorated, that could weigh on preferred security prices.

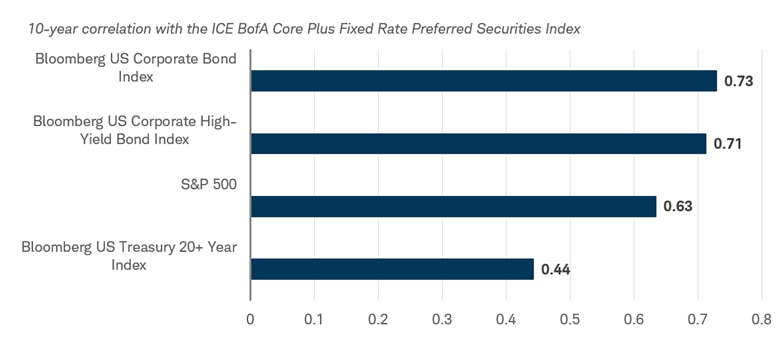

In fact, preferred securities tend to be correlated to both stocks and bonds. Over the last 10 years, the ICE BofA Core Plus Fixed Rate Preferred Securities Index has had a relatively high correlation with the S&P 500 as well as the investment-grade and high-yield corporate bond indexes. The correlation with an index of long-term Treasuries is a bit lower, but a 0.44 correlation highlights that there is still a relationship. That's important for investors to understand, as higher bond yields and/or falling stock prices can impact the values of preferred securities. With a lot of uncertainty around the economic outlook given the conflict in the Middle East, preferred securities prices could fluctuate over the short run.

Preferred securities tend to have high correlations with investment grade and high-yield corporate bonds, as well as stocks

Source: Bloomberg.

Bloomberg US Corporate Bond Index (LUACTRUU Index), Bloomberg US Corporate High-Yield Bond Index (LF98TRUU Index), S&P 500 (SPX Index) and Bloomberg US Treasury 20+ Year Index (LT11TRUU Index). Correlations shown represent an equal-weighted average of the correlations of each asset class with the ICE BofA Core Plus Fixed Rate Preferred Securities Index during the 10-year period between April 2016 through April 2026.

Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets. Past performance is no guarantee of future results.

What to consider now

Preferred securities appear attractive today. Their yields have generally risen more than corporate bond yields and long-term Treasury yields over the last few months, presenting a nice entry point for investors looking for higher income. Meanwhile, the yields are only slightly below the average yields offered by high-yield corporate bonds, and they have higher average credit ratings.

The potential tax advantages can make preferreds even more attractive when considering them in taxable accounts. For investors in high tax brackets, the after-tax yield advantage over high-yield bonds can be close to 100 basis points or more, as I noted in the chart titled "Preferred securities can offer tax advantages." However, it's important to keep in mind that not all preferreds pay qualified dividends, so it's important to do your homework.

But keep in mind the risks associated with preferreds, such as high-interest rate risk, where rising long-term yields could pull their prices lower, and potential volatility given the ongoing Iran war.

Investors willing to take a little extra risk might consider investing in preferred securities and there are a number of ways to do so. Schwab clients can use the Preferred Shares Screener when looking for individual preferreds, or they can explore funds on the ETF or Mutual Fund pages. Preferred funds can be found under the Morningstar category of "Preferred Stock." You can also consider a separately managed account.

About the author