Asset Management

Will the Bitcoin Halving Cycle Persist?

Key Takeaways:

- Bitcoin has historically shown relative resilience in some bear market recoveries compared to other crypto assets, although past patterns may not continue and prices have at times struggled to move above inefficient miner production costs without a catalyst.

- In our view, bitcoin's halving may continue to influence market behavior, but its effects could differ from prior cycles or diminish over time as the crypto market evolves.

- Our framework suggests bitcoin has at times been relatively stronger than digital asset treasury companies, miners, and altcoins at similar points in prior cycles, though this relationship may not continue.

- Investors have sometimes referred to the term when cryptocurrencies other than bitcoin outperform as "alt season." While the period has never been defined, when bitcoin is above inefficient miner production prices, altcoins have historically outperformed, suggesting this is a measure of when "alt season" begins.

- While past performance is no guarantee of future results, in our view, if seasonal patterns resemble prior periods and if the CLARITY Act passes, cryptocurrencies could experience more positive sentiment later in the year. However, seasonal patterns are not reliable predictors of future performance, and outcomes remain uncertain and subject to policy developments, market conditions, volatility, investor sentiment, and the risk of substantial losses. Risks to this view include the possibility that the CLARITY Act does not pass, is modified in a way the market views as less crypto-friendly, or that future election outcomes change the policy backdrop.

- Bitcoin has historically shown relative resilience in some bear market recoveries compared to other crypto assets, although past patterns may not continue and prices have at times struggled to move above inefficient miner production costs without a catalyst.

- In our view, bitcoin's halving may continue to influence market behavior, but its effects could differ from prior cycles or diminish over time as the crypto market evolves.

- Our framework suggests bitcoin has at times been relatively stronger than digital asset treasury companies, miners, and altcoins at similar points in prior cycles, though this relationship may not continue.

- Investors have sometimes referred to the term when cryptocurrencies other than bitcoin outperform as "alt season." While the period has never been defined, when bitcoin is above inefficient miner production prices, altcoins have historically outperformed, suggesting this is a measure of when "alt season" begins.

- While past performance is no guarantee of future results, in our view, if seasonal patterns resemble prior periods and if the CLARITY Act passes, cryptocurrencies could experience more positive sentiment later in the year. However, seasonal patterns are not reliable predictors of future performance, and outcomes remain uncertain and subject to policy developments, market conditions, volatility, investor sentiment, and the risk of substantial losses. Risks to this view include the possibility that the CLARITY Act does not pass, is modified in a way the market views as less crypto-friendly, or that future election outcomes change the policy backdrop.

Bitcoin has been rangebound since it appeared to find its bear market bottom in early February as of June 17, 2026. We previously made the case that bitcoin typically outperforms other cryptocurrencies in bear market recoveries and has historically taken over a year to surpass the cost of production for inefficient miners.

In "Bitcoin Mining Economics and the Pivot to AI," we posited that the fair value for bitcoin may be a small premium to the cost of production for inefficient miners—currently $95,000 according to data from Glassnode as of May 31, 2026. In past bear market recoveries, this level has also served as resistance until a fundamental catalyst has been able to push prices through it. The average cost basis for bitcoin investors is around $80,000 [$83,000 for exchange-traded product (ETP) owners and $78,000 for all investors excluding miners] according to data from Glassnode as of May 31, 2026. For investors who acquired bitcoin at these levels over the past year and a half, they may be inclined to sell after seeing their investment quickly grow nearly 60% through the bull market peak and then ultimately fall 50% to the bear market trough.

Given the lack of catalysts and weak sentiment following the bear market, it may take time to reignite fresh momentum into the crypto market. Given this, in "A Dream of Spring Amid Crypto Winter," we introduced more favorable views on bitcoin relative to other cryptocurrencies. We believe that when investors finally begin to see the bear market through their rearview mirror, they may reassess crypto exposures outside of bitcoin, although such assets remain speculative and may not be appropriate for all investors.

Common ways to add alternative bitcoin exposure include levered bitcoin equity proxies, which are equity securities that indirectly track bitcoin's price through a leveraged corporate treasury strategy, and altcoins, which are cryptocurrencies other than bitcoin. Understanding the historical performance of both can offer perspective as to when they have outperformed spot bitcoin, though keep in mind that past performance is no guarantee of future results.

Finally, following bitcoin's recent fall back to the low $60,000s, we also offer our perspective on another key crypto debate—has bitcoin historically had its own economic cycle and will the "bitcoin halving cycle" persist in the future?

Summary of key crypto debates

| Cryptocurrency | Sector | Industry | Industry Standard Network Effects | Leading Market Share | Scalability | Tokenomics | Key Debate(s) | Trading Range | Current Valuation |

|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | Foundational Networks | Store of Value | ✔️ | ✔️ | ❌ | Below Average |

|

0.75x-2x Inefficient Miner Production | 0.8 Miner Production |

| Ether | Foundational Networks | Smart Contract Platform | ✔️ | ✔️ | ❌ | Average | Ethereum scalability | 40x-70x Market Cap/ "GDP" | 33x Market Cap/ "GDP" |

| XRP | Foundational Networks | Stove of Value | ❌ | ❌ | ✔️ | Below Average | Store of value or smart contract? | 0.1x-0.4x Market Cap/Transfer Volume | 0.2x Market Cap/Transfer Volume |

| Sol | Foundational Networks | Smart Contract Platform | ❌ | ❌ | ✔️ | Above Average | Expand beyond meme trading? | 20x-100x Market Cap/ "GDP" | 18x Market Cap/ "GDP" |

Key debate: Will the bitcoin halving cycle persist?

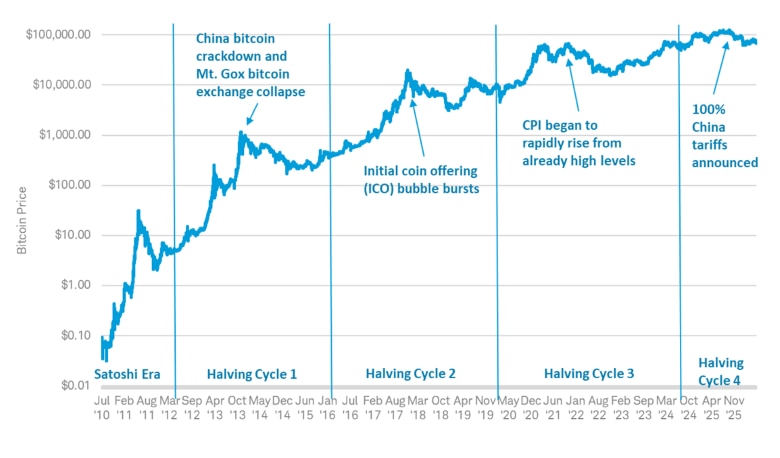

Many crypto investors have said bitcoin's halving has created a "cycle" that permeates across the cryptocurrency market. Historically, this has been accurate, and a key debate within the digital assets industry continues to be whether the cycle will persist in the future. Traditionally, this cycle kicked off at bitcoin's halving, resulting in an approximately two-year bull market, followed by a deep bear market into the third year. Prices have historically staged modest recoveries throughout the fourth year before entering a new bull market around the next year's halving. But the question remains: is this actually a cycle, or simply an exercise of data mining historic price action?

Bitcoin has historically exhibited its own unique four-year economic cycle

Source: Glassnode and Schwab, as of 5/31/2026.

In prior cycles, bitcoin peaks have often occurred in the period following a halving, though the historical sample is limited and the pattern may not continue.

Past performance is no guarantee of future results. For illustrative purposes only and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment.

Whether the "four-year cycle" is real or not comes down to studying "bitcoin winters," which are severe cryptocurrency bear markets that last several months and are accompanied by negative investor sentiment. While each cycle had the same starting catalyst—bitcoin's halving—each "winter" was triggered by a different event. Bitcoin's first halving cycle's bull market ended following China banning bitcoin, which ultimately led to a crypto exchange called Mt. Gox collapsing. The next cycle's bull market ended following the Initial Coin Offering (ICO) bubble bursting. The 2021-2022 bear market kicked off after consumer price index (CPI) had been growing more than 5% year-over-year and started accelerating even faster. This resulted in a bear market for all risk assets as the market discounted a rate hike cycle and economic slowdown.

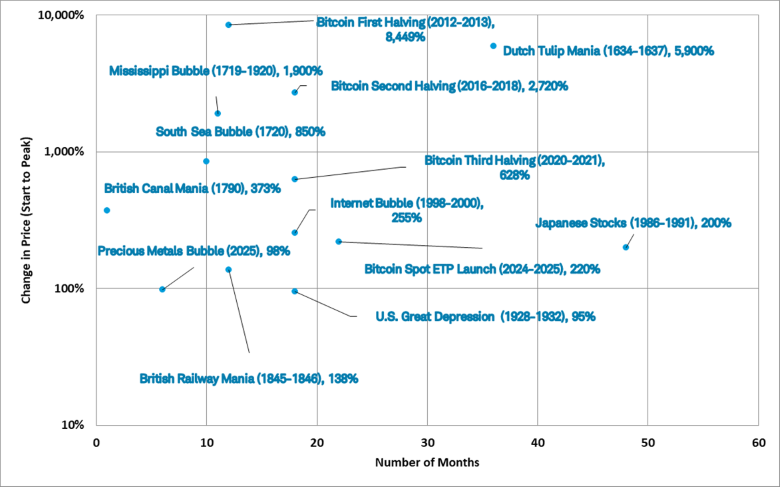

While each cycle had a different event that caused the bear market, a similarity in these cycles was the bull market peak in the fall of the second year following bitcoin's most recent halving. These peaks have historically been periods where speculation was rampant and leverage in the crypto ecosystem was very high. Looking at 13 major asset bubbles throughout history, the median bubble has lasted for about 18 months, suggesting it's not surprising that bitcoin's cycles have peaked anywhere from 18 to 20 months following its halving.

When thinking about how to add exposure to cryptocurrencies with the bitcoin halving in mind, one method has been to treat the third year following bitcoin's halving from the perspective of seasonality, because it has historically been a less favorable year for crypto exposure.

Major asset bubbles over the past 400 years have lasted around 18 months

Source: Schwab, as of 5/31/2026.

Past performance is no guarantee of future results. For illustrative purposes only and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment.

Due to the number of times this cycle has played out across bitcoin's 17-year history, the bitcoin halving cycle has cemented itself in the mind of many crypto investors. While it's important to point out that the future may not repeat—it's been over 100 years since Charles Dow first started publishing about moving averages and investors still use them to identify areas of support or resistance in asset prices. So regardless of whether bitcoin "has a cycle," that cycle has become a mainstream function of investors' perception of the world's largest cryptocurrency through enough market lore.

Shifting back to the debate, it's important to have a perspective as to whether this cycle will repeat in the future to figure out whether it's truly an economic cycle.

Schwab's perspective on the bitcoin halving cycle debate

Not everything in investing is black and white, and our take falls within the gray area of this debate. In our view, through enough market lore, the so-called "bitcoin halving cycle" has become a feature of bitcoin. While the halving cycle's impact may persist, the potential impact across the broader crypto market is uncertain and may diminish over time.

Much of the previous cycle's blow-off tops—when prices and trading volume surge rapidly and fall sharply in a sudden decline—during the bull markets can be attributed to bitcoin's market cap. Since bitcoin is a supply-constrained asset and new supply cannot come online, bitcoin's fair value overshot to the upside. When an adverse event occurred, there were no buyers left at that level, resulting in massive drawdowns.

It's important to note that often hidden leverage emerged throughout the bear markets. For example, during the first halving cycle in 2012, the Mt. Gox bitcoin exchange was already having issues following a hack in 2011. While China banning bitcoin may have kicked off the bear market, the collapse of Mt. Gox is what really accelerated it.

In 2021-2022 a similar situation occurred. While nearly all risk assets entered a bear market (crypto in 2021 and stocks in 2022) following the hot inflation data, hidden leverage exposed itself in bitcoin as several crypto institutions failed. Market stress impacted an algorithmic stablecoin issued on the Terra blockchain called TerraUSD, then the contagion spread to a cryptocurrency hedge fund called Three Arrows Capital, and finally to the cryptocurrency exchange FTX.

From an efficient market hypothesis perspective, bitcoin may be strong-form efficient. Strong-form efficient market hypothesis posits that market prices incorporate all public and private information, and beating the market is not possible. Since bitcoin has no private information—all information related to bitcoin is publicly available via blockchain data and future supply is known—the price over the long run should be the market equilibrium between supply of bitcoin and demand for it. This also aligns with our cost-of-production valuation framework. Each new halving results in the cost of producing bitcoin rising, because production costs have a reflexive relationship with bitcoin's price.

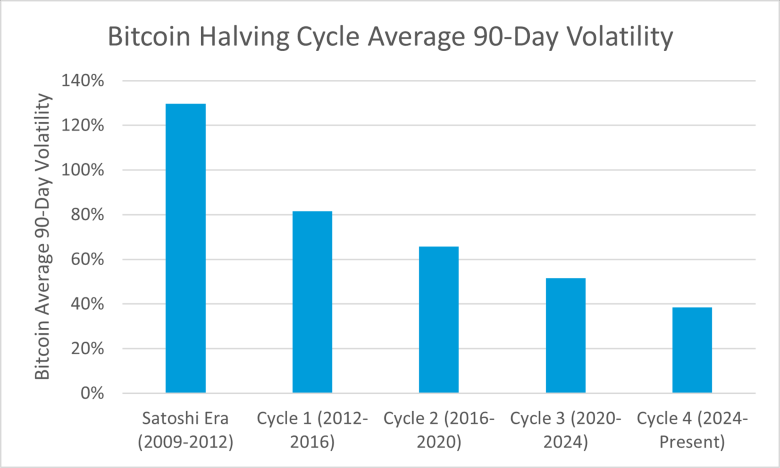

While the halving may continue to have an impact in the future, the story in bitcoin over its 17-year history has been lower volatility as it has grown. This is evidenced by the 8x return during the rise from its 2022 trough to its 2025 peak (which paled in comparison to other bull runs) followed by a 50% bear market (again, paling in comparison to other bear markets) that fell 75-plus percent.

This may be a function of the law of large numbers—a tenfold gain generally requires substantially more capital for a $1 trillion asset than for a smaller asset. Part of this might also be attributed to much of the speculation in crypto now happening outside of bitcoin—whether in altcoins, levered proxies, or products like prediction markets. Regardless of lower volatility and speculation outside of bitcoin, at the onset of the halving, bitcoin's price may still need to adjust to higher production costs and lower levels of new supply.

Bitcoin's average volatility has consistently fallen across its 17-year history

Source: Glassnode, Bloomberg, Schwab from January 1, 2009 to May 31, 2026.

Past performance is no guarantee of future results. For illustrative purposes only and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment. Volatility is measured as the annualized standard deviation of bitcoin's daily price changes over a rolling 90-day period. The percentages shown reflect the typical magnitude of price fluctuations, not returns. For example, a value of ~80% in Cycle 1 (2012 to 2016) indicates that, based on recent price movements, bitcoin's price would be expected to vary widely over a year (i.e., large and frequent price swings), whereas lower values in later cycles indicate comparatively smaller fluctuations.

It's also important to understand why bitcoin halving may have less impact on other cryptocurrencies going forward. As financial institutions begin to leverage blockchain technology, demand for other cryptocurrencies may be more heavily influenced by financial institutions beginning to leverage blockchain technology. Historically, bitcoin has determined the direction of travel for all other cryptocurrencies, as it is the largest cryptocurrency and makes up 50% of the broader crypto market cap as of May 30, 2026, according to data from CoinMarketCap. As bitcoin's price has risen, investors have often engaged in more speculative activities like futures trading through decentralized exchanges, meme trading, and using different decentralized finance (DeFi) protocols.

Using Ethereum as an example, last year, 50% of its fees came from stablecoins, the next 20% came from lending applications, another 20% came from liquid staking applications, and the balance came from trading and infrastructure applications. Much of the demand for these activities can be attributed to the rise in bitcoin's price.

As investors begin to get more confidence in the crypto ecosystem (because bitcoin's price is rising), they onboard traditional currencies into crypto exchanges, which are often swapped into stablecoins. Stablecoins are eventually swapped for volatile cryptocurrencies or used as margin collateral in trading applications or similar DeFi applications. As this activity increases, demand for ether also increases because ether is needed to pay for transaction, or "gas," fees on its network, resulting in higher prices. As prices rise, investors can deposit their ether into lending protocols and earn income on it. Proof-of-stake blockchains such as Ethereum also reward participants who stake their ether to provide network security, so as more ether is staked, demand for liquid staking products increases as well. All this activity creates a reflexive loop, driving greater demand for ether.

This same process happens on other smart contract platforms whose primary use cases are even more speculative and which have lower utility than the applications on Ethereum. Ultimately, as bitcoin's price starts to fall, demand for all of these uses falls, creating a reflexive price loop to the downside.

These dynamics may help explain why bitcoin has historically outperformed other cryptocurrencies during bear market recoveries. It takes time, and often a fundamental catalyst, to reignite momentum into cryptocurrencies. Historically, altcoin rallies have been short-lived during the recovery.

As traditional financial institutions and non-crypto companies adopt blockchain technology, this can potentially create a stream of fees not solely tied to bitcoin's price. That said, in the short term, bitcoin may continue to play a significant role in broader crypto ecosystem direction.

Understanding DATs

DATs are publicly traded equities entities that use combinations of share offerings, business operations, and debt offerings to acquire and hold cryptocurrencies on their balance sheet. These companies are often valued by dividing their market cap or enterprise value by the market value of their crypto holdings. This ratio is referred to as a multiple of net asset value, or mNAV. Because DATs have only existed for a relatively short period, historical mNAV patterns may not be a reliable indicator of future performance or valuation.

In general, DATs have an inflationary share supply. Historically during bull markets, as the holdings of their cryptocurrencies appreciate, their mNAV multiples have risen, resulting in the companies being valued at a premium to their underlying holdings. Management teams have often taken advantage of this by issuing new shares to acquire more underlying crypto holdings. This is dilutive to shareholders from an earnings per share perspective, however, many shareholders seek to increase their bitcoin per share, which this share issuance may accomplish. For DATs that rely on equity and debt issuance to acquire crypto, management teams and their investors are assuming that the cost of capital is less than the compound annual growth rate for the underlying cryptocurrencies.

Historically, as momentum has increased in the crypto markets, DATs have exhibited multiple expansion. When momentum begins to wane, their multiples have historically contracted. Some investors may view a DAT trading near 1x mNAV as relatively less expensive and a DAT trading at 2x or above as relatively more expensive, although mNAV has important limitations and does not determine future performance. DATs that trade at a steep discount to their mNAV reflect investor concern over their ability to issue shares, acquire cryptocurrencies on their balance sheets, and ultimately whether they can remain solvent without selling crypto holdings. Banks have similar valuation metrics and are typically valued using price-to-book ratios. A bank trading at a discount to its book value may be considered potentially insolvent.

There has been a debate as to how DATs should be classified as in general they do not have operating cash flows and have features similar to investment companies, like closed-end funds. Similar private equity and real estate products exist that acquire land under the assumption its value will increase over time—which is not too dissimilar to what DATs are doing. Cryptocurrencies are considered property, similar to real estate. While real estate investment trusts (REITs) are publicly traded entities that acquire properties, they are required to pay out 90% of their operating income to investors, something DATs cannot do. There are examples of publicly traded land trusts, which technically are not required to generate income, but their land is often monetized through mineral royalties. Again, we do not offer a perspective on how DATs should be classified or their viability as public equities, but since investors use them as a levered play on their underlying crypto holdings, it's important to understand when they have historically outperformed their underlying cryptocurrency.

When have bitcoin proxies and altcoins historically outperformed bitcoin?

Some crypto investors have historically tried to position around the bitcoin halving cycle but translating that into an allocation framework has been difficult and highly uncertain. While the general four-year directional cycle has repeated several times, it is difficult to determine when to shift your allocation among crypto assets in a live setting. We present a framework to consider that offers a way to invest across the crypto market regardless of whether the "bitcoin halving cycle" will persist.

Historically, there have been periods when bitcoin digital asset treasuries outperformed spot bitcoin. This occurs as the average investor is again in profit, meaning the average investor's bitcoin position is no longer reflecting a loss and prices are above their cost basis, yet mNAV premiums are still low. Later in some prior cycles, miners and altcoins have historically outperformed bitcoin, but it's important to note that this outperformance has always only been for a period of time. Ultimately bitcoin has outperformed all of these over a multi-year period.

Our framework models bitcoin across a supply-demand-leverage stack. Bitcoin's price relative to efficient and inefficient miner costs defines the activation of the supply curve, while investor profitability anchors demand. As investor profitability has historically risen, the equity layer introduces amplification via mNAV. During expansion, mNAV increases as capital flows into financial leverage vehicles like DATs, futures, and options. One outcome might be that once bitcoin exceeds inefficient production costs, at which point the entire mining base could become profitable, potentially driving operating leverage expansion and capital rotation into miners. With enough upside momentum across each different type of bitcoin exposure (spot, DATs, and miners), eventually altcoins may benefit from a capital rotation as investors seek the next leg up.

Relative performance across these layers may provide one systematic framework for capital allocation across the cycle. Ultimately, as these trades become crowded and momentum wanes, spot bitcoin and defensive positions have outperformed, but that pattern may not repeat.

One of the best ways to track leverage and crowding of trades in the crypto ecosystem is by observing the bitcoin basis trade. Early on in bull markets, as demand for leverage increases, crypto futures have historically traded at a premium to spot prices. As a result, arbitragers go long the future and short spot. As more investors realize this arbitrage opportunity exists, historically the annualized yield that can be gained from the basis trade begins to compress. Pairing this with other measures of leverage can be useful to assess changing risk conditions and when it might make sense to shift back to less volatile crypto exposure. Futures trading involves substantial risk and is not suitable for all investors.

Tying it all together

Historically, bitcoin has outperformed other altcoins and levered proxies while the price of bitcoin was below the average investor's cost basis. As bitcoin progressed throughout its cycle, and momentum accelerated, levered plays on bitcoin have historically outperformed bitcoin during different periods. This outperformance has typically started in DATs, then shifted to miners and eventually altcoins.

We believe that while bitcoin halving has historically acted as a fundamental catalyst to ignite a new bull market, should the CLARITY Act pass, it could add new support to the narrative of institutional adoption that powered the latest crypto bull market. And while past performance is no guarantee of future results, we do observe that historic seasonality patterns show that prices have rallied in the fall. On average, bitcoin's returns have been stronger in October, November, and December, following weaker returns in the summer and September. Should bitcoin seasonality repeat, with added momentum from the potential passing of the CLARITY Act, cryptocurrencies could experience periods of positive sentiment, although outcomes remain uncertain and losses can be substantial. Also keep in mind that seasonal patterns are not reliable predictors of future performance.

That said, there are risks to this perspective. It could be perceived as negative if the CLARITY Act were to not pass, or if it were to pass with changes seen as less crypto friendly. Since the current administration with a majority in Congress is viewed as crypto friendly—even though crypto currently has bipartisan support—results of mid-term elections could also be perceived as a negative catalyst.

Keep in mind that all cryptocurrencies are relatively new and due to their novel and unproven nature, reliable methods for estimating performance may not be available. The regulatory landscape for crypto is still evolving. Cryptocurrencies may be subject to potential encryption breaking, illiquidity and increased risk of loss. Theft, scams, and fraud have been a factor to deal with, and if you decide to invest in crypto directly remember that there may not be an effective way to recover assets if they're stolen or lost. Investing in cryptocurrencies involves risk, including the risk of total loss of principal invested. Cryptocurrencies such as bitcoin are highly volatile, are not backed or guaranteed by any central bank or government; are not deposits; are not FDIC insured; are not SIPC protected; and lack many of the regulations and consumer protections that legal-tender currencies and regulated securities have. Spot markets on which cryptocurrencies trade are relatively new and largely unregulated, and therefore, may be more exposed to fraud and security breaches than established, regulated exchanges for other financial assets or instruments. Due to the high level of risk, investors should view digital currencies as a purely speculative instrument.

About the author