Asset Management

Positioning Client Portfolios Amid Interest Rate Uncertainty

Why short-duration fixed income deserves a fresh look by clients

For investors, 2026 has been a reminder of how quickly the market narrative can shift. The year began with expectations for moderating inflation and a Federal Reserve likely to cut short-term interest rates. However, geopolitical conflict, higher energy prices, and firmer inflation have complicated the outlook, creating an unsettled market backdrop, shifting rate expectations, and driving the need for more nuanced portfolio decisions.

In the process, this backdrop has sharpened a practical question for advisors: how to position client portfolios when policy expectations remain fluid, longer-duration outcomes are harder to handicap, and equity markets have posted double-digit gains so far this year. As a result, the front end of the yield curve is worth another look—not as a call on any single outcome, but as a place to seek income, manage interest rate sensitivity, and potentially enhance resilience within a client’s broader asset-allocation framework.

Key takeaways:

- Plenty to consider at the front end: Still-elevated yields in short-duration fixed income offer a range of ways to pursue stability, income, and total return across different credit exposures and duration profiles.

- Attractive risk-adjusted return potential: Short-duration fixed income yields have climbed lately, and long-term experience suggests returns in this part of the yield curve have compared favorably with other fixed income segments on a volatility-adjusted basis.

- Resilience in a range of scenarios: For investors looking to limit duration risk and interest rate sensitivity, shorter-duration exposure may be worth considering in both more stable and more volatile market environments.

Investing implications with a changed yield curve

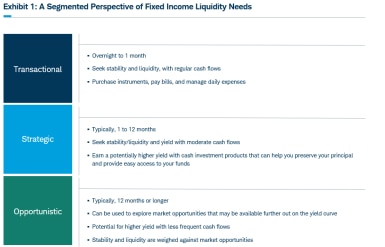

By now, advisors have heard the refrain that, "Fixed income is back." With yields elevated, different segments of the bond market are able to play distinct roles—helping to provide stability, generate income, or support risk-adjusted return objectives. As a result, fixed income allocation conversations have become more active, especially in shorter-duration strategies where liquidity needs can often be segmented into three buckets, as illustrated in Exhibit 1: transactional (typically overnight to 1 month), strategic (1 to 12 months), and opportunistic (12 months or longer).

Notably, despite earlier forecasts that short-duration fixed income would see meaningful outflows as the Fed began easing in late 2024, the opposite occurred. For example, funds captured in the Morningstar Short-Term Bond and Ultrashort Bond categories experienced a net inflow of nearly $150 billion in 2025, with another $69.5 billion through May 31, 2026. These flows came as investors sought to take advantage of still high yields as they awaited more clarity on the future direction of rates and the economic implications of tariff policies enacted in early 2025.

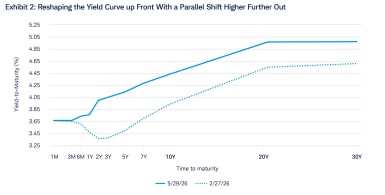

To illustrate how fixed income conditions have shifted this year, a useful starting point is the U.S. Treasury yield curve. In Exhibit 2, we compare the shape of the curve today with its shape just before the start of conflict in the Middle East.

Sources: Charles Schwab Asset Management®; Bloomberg. U.S. Treasury yield curves as of 02/27/26 and 05/29/26.

Three observations stand out to us from this exhibit:

- Earlier this year, the modest downward slope at the front end of the yield curve left investors exposed to reinvestment risk as upcoming maturities rolled into potentially lower yields. Today, that front-end curve is relatively flat, with only about 35 basis points (0.35%) separating one-month Treasury bills from two-year Treasury notes. In practical terms, investors may not need to take on much more duration to access yields similar to those available in very short Treasuries.

- The slightly upward-sloping shape of the yield curve also suggests less reinvestment risk for maturing fixed income proceeds than a few months ago. Yields rise beyond the two-year maturity point, but the 3.75% to 4.25% range available at the short end of the yield curve appears attractive for investors seeking returns competing with inflation, yet with lower average sensitivity to future rate moves, and still addressing strategic and opportunistic liquidity needs.

- Most of the yield curve reshaping since February has occurred in maturities of two years or less, while yields further out along the curve have shifted higher in a more parallel fashion. This wider range of outcomes for longer maturities underscores the difficulty of trying to forecast where interest rates may settle over time, even as the front end of the yield curve responds more directly to actual and expected policy moves.

Putting fixed income segments on an equal footing

How do short-duration approaches compare with the broader fixed income opportunity set? In Exhibit 3, we compare annualized total returns and volatility over the trailing 10-year period across a range of high-quality bond indexes. That span includes a highly dynamic interest rate backdrop: the Federal Reserve raised interest rates from 2016 to 2018, reversed course in 2019, employed a zero-interest-rate policy stance during the COVID-19 Pandemic, adopted an aggressive rate-hiking cycle from 2022 to 2023, and returned to easing short-term interest rates in 2024. Taken together, these shifts provide a useful test of the role short-duration fixed income can play in a balanced portfolio across changing regimes.

Sources: Charles Schwab Asset Management; Morningstar. The bond categories are represented by: ICE BofA 0–3 Month U.S. Treasury Bill Index, ICE BofA 0–1 Year U.S. Treasury Index, Bloomberg 1–5 Year Treasury Index, Bloomberg U.S. Aggregate Bond Index, and the Bloomberg U.S. Treasury Index. Past performance is no guarantee of future results. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For additional information about the indices and terms shown, please visit www.schwabassetmanagement.com/resources/glossary.

The takeaway from Exhibit 3 is that short-duration approaches—whether through Treasuries or investment-grade corporate bonds—have compared well with longer-duration strategies like those benchmarked on the Bloomberg U.S. Aggregate Bond Index and the Bloomberg U.S. Long Treasury Index. Many investors we've spoken with seem to still be anchoring core bond allocations to these broader benchmarks without fully weighing shorter-duration segments or considering modestly higher credit exposure. While longer-duration indexes currently offer somewhat higher yields, experience across rate regimes suggests the short end of the fixed income yield curve has the potential to deliver stronger volatility-adjusted outcomes. Adding corporate exposure can increase volatility relative to Treasury-only approaches, but it can also come with higher return potential.

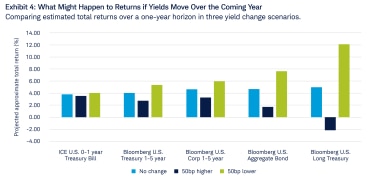

What might happen if rates move?

As this year has shown, the outlook for interest rates remains difficult to predict. Even experienced market participants know that forecasting short- or medium-term interest rate moves can be humbling. In Exhibit 4, we estimate the one-year total return of several high-quality fixed income indices under three simple illustrative scenarios: (1) no change in rates across the curve, (2) a one-time parallel shock of 50 basis points (0.50%) higher, and (3) a one-time parallel shock of 50 basis points lower. For simplicity, we set aside other curve-shape changes such as steepening or flattening. The indexes are ordered from left to right by increasing starting yield to worst and duration.

Under the no-change scenario, the estimated one-year total return would be relatively similar across indexes, but the range of potential outcomes widens meaningfully as we move to the right. This added variability largely reflects the higher duration. And this is the key point: given the shape of today’s yield curve, and absent a high-conviction view on where interest rates and bond yields might be in a year, short-duration fixed income may offer returns comparable to those of higher-duration strategies, while introducing less uncertainty and dispersion in potential outcomes.

Sources: Charles Schwab Asset Management; Bloomberg. Starting yields as of 5/31/26. This illustration is hypothetical. It does not represent a specific investment, and no forecast returns are guaranteed. Total return approximated as starting yield plus or minus the price return accounted as decline or increase in the yield times duration. Past performance is no guarantee of future results. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For additional information about the indices and terms shown, please visit www.schwabassetmanagement.com/resources/glossary.

Portfolio construction implications

With all of these points in mind, the current backdrop presents a timely moment for advisors to revisit how fixed income is positioned across clients' portfolios. With yields remaining attractive at the front end of the yield curve and interest rate expectations fluid, today's opportunity is less about trying to predict precisely where interest rates will go from here and more about building fixed income allocations that are aligned with a client's liquidity needs, income goals, and tolerance for duration risk. In today’s environment, this may make short-duration fixed income a particularly useful starting point for client portfolio construction conversations. And the good news is that this exposure is available in a variety of investment vehicles, including ETFs, mutual funds (including money market funds) and separately managed accounts. Each investment vehicle has its own relative strengths and weaknesses, so consider each client’s particular circumstances when building their short duration fixed income exposures.

Next steps to consider for clients:

- Revisit the role of core fixed income allocations. Review whether long-duration exposure still reflects your client’s objectives, or whether part of this allocation may be better positioned in shorter-duration strategies with less sensitivity to interest rate moves.

- Align fixed income allocations with time horizons. Consider matching your client's short-duration allocations to near-term spending, liquidity, and rebalancing needs so that assets intended for use over the next 12 months are protected from unnecessary duration risk.

- Pursue efficient yields without overreaching. Consider where high-quality short-duration Treasuries or investment-grade corporate bonds may help support income goals while maintaining a more controlled risk profile than longer-duration alternatives alone might provide.

- Use scenario analysis to sharpen client conversations. Show how similar starting yields can still lead to a wide range of outcomes as duration increases, helping clients understand why a shorter-duration exposure may deserve a more prominent place amid today’s fluid rate environment.

About the author