Beyond market cap—The strategic case for Fundamental Indexing

One quarter into the year, a prominent theme in our client conversations carries over from 2025: what to do about equity markets and client portfolios that despite the recent pullback and climb in volatility, still feel concentrated, given the outsized run-up in select companies and industries in recent years. Recent geopolitical events are certainly a wildcard with a range of potential outcomes near term. But the prospects for market broadening and sustained earnings growth, fiscal support, and the potential for further Federal Reserve easing leave us constructive on risk markets for investors with a strategic mindset. Equity market concentration remains top of mind for investors and allocators alike who are still searching for diversification opportunities to potentially reduce risk and volatility, while preferably not sacrificing long-term returns.

Key takeaways:

- Concentration risk persists: While S&P 500® index concentration peaked in late 2025, systemic exposure to the largest index constituents remains historically high.

- Unintended portfolio drift: This backdrop has left many investors with significant, unintended overweight positions in large-cap growth that are misaligned with their risk profiles.

- Strategic market broadening: Insights from our colleagues in the Schwab Center for Financial Research® suggest that market participation will continue to broaden throughout 2026.

- Fundamental indexing opportunities: Complementing core market-cap-weighted holdings with strategies based on company fundamentals may provide a more balanced portfolio approach.

- Enhanced performance potential: This complementary positioning could potentially enhance risk-adjusted portfolio returns, particularly if market concentration begins to normalize as forecasted.

Charting the shifting concentration landscape

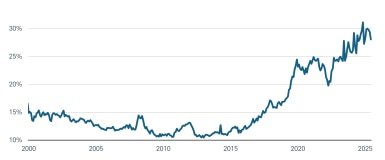

First, to put the market concentration issue into historical context, we track the weight of the top five stocks in the S&P 500 as a percentage of the overall index’s capitalization in Exhibit 1. It's important to recognize that the top five companies within the index have materially shifted over time, reflecting the underlying trends within the broader U.S. economy away from what was once manufacturing-based activity and toward technological revolution. For example, of the current largest companies—NVIDIA, Apple, Alphabet, Microsoft, and Amazon—only Apple and Microsoft were part of the S&P 500 Index prior to 2000. However, we note that the importance of the current top five companies—without taking a view of each company's valuation outright—to the future performance of this index is essentially unprecedented. Therein lies a material challenge to market capitalization-weighted index approaches: the larger the combined market size of just a few companies, the more dependent investors become on this same cohort, introducing the potential for risk creep and portfolio volatility.

Exhibit 1: S&P 500 index concentration risk in perspective

The top five stocks in the S&P 500 as a percentage of the overall index, based on market capitalization.

Sources: Charles Schwab; Bloomberg. Data as of 2/28/26. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on the indexes and terms shown, please see: www.schwabassetmanagement.com/resources/glossary. Past performance is no guarantee of future results.

"One way to address portfolio concentration when a subset of companies potentially defines an index's performance is to complement core holdings with an alternative weighting strategy."

Strategic diversification—fundamentally navigating market-cap drift

One way to address portfolio concentration when a subset of companies potentially defines an index's performance is to complement core holdings with an alternative weighting strategy. For example, there are products in the marketplace constructed to track an index comprised of those same companies in the S&P 500 but instead weight them equally. One example of this approach is the S&P 500® Equal Weight Index—which, as the name implies, is an equal-weight version of the widely used S&P 500. Year-to-date through February 28, this equal-weight index has returned 7%, while the S&P 500's total return over the same period has been essentially flat, as concentration within the index has fallen.1

But while we appreciate the merit of equal-weighted strategies, we think that these approaches can feel somewhat arbitrary, rather than being soundly rooted in a set of compelling investment principles. From our perspective, investors who are truly looking to gain broad equity exposure to macro growth and corporate profitability would be better off aligning with the size of the economic footprint of their holdings. This is where fundamentally weighted index strategies come into play.

"Schwab Asset Management first partnered with Research Affiliates nearly 20 years ago to develop a suite of mutual funds and ETFs that employ an analytically rigorous approach to equity solutions."

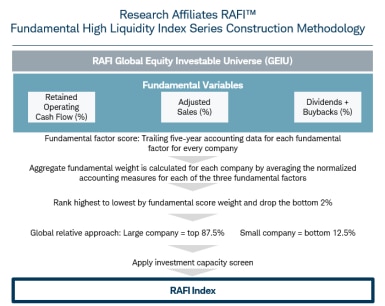

Schwab Asset Management® first partnered with Research Affiliates® nearly 20 years ago to develop a suite of mutual funds and ETFs that employ an analytically rigorous approach to equity solutions. The Fundamental Index® methodology is rooted in the Graham & Dodd economy-centric view—discussed in their 1934 work, Security Analysis, which is still in revised print today—where the weight of a company in an index is determined by three fundamental variables: (1) retained operating cash flow, (2) adjusted sales, and (3) total dividends plus buybacks. This construction methodology, to which each of Schwab Asset Management's Fundamental Index products are benchmarked, is summarized in Exhibit 2.

Exhibit 2: Shifting the conversation from market sentiment to economic substance

Sources: Schwab Asset Management; RAFI. The index construction methodology is available at: https://www.rafi.com/knowledge-center/questions/rkc-68. Note that RAFI Indices is expecting to evaluate potential methodology shifts to the RAFI Fundamental High Liquidity Index Series in 2026.

This transparent approach to index construction ultimately skews toward dynamic value and dividend yield factor tilts compared with traditional market cap-weighted index approaches. As fundamentals shift, the index methodology calls for a reduction in the weight of stocks whose prices have risen above their firms' fundamental footprints, while adding exposure to firms whose stock prices don’t fully capture their size.

"Is there a tie between the potential for falling equity market concentration and the opportunity in Fundamental Index strategies?"

The concentration inflection—A catalyst for potential Fundamental Index outperformance

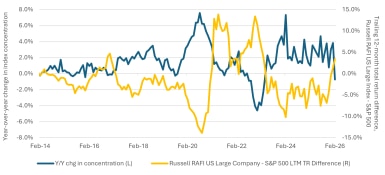

Is there a tie between the potential for falling equity market concentration and the opportunity in Fundamental Index strategies? In Exhibit 3, we track two time series. The first is the year-over-year change in S&P 500 concentration, measured the same way as in Exhibit 1—using the top five stocks’ combined weight as a percentage of the index's total market capitalization. The next is the difference between the trailing one-year performances of the Russell RAFI US Large Company Index, which is a fundamentally weighted index strategy of large-capitalization US companies, and the S&P 500. Note the inverse relationship between the two series: when market concentration has decelerated, or outright declined year-over-year, the Fundamental Index strategy’s return has improved or outright outperformed relative to the S&P 500 on a 12-month basis, and vice versa.

Exhibit 3: As top-five concentration has fallen, Fundamental Index strategies have outperformed

Sources: Charles Schwab; Bloomberg. Data as of 02/28/2026. The blue line represents the percentage shift in the S&P 500 of top five constituents. The yellow line represents the 12-month trailing total return of the Russell RAFI™ US Large Company Index minus the S&P 500 index. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on the indexes and terms shown, please see: www.schwabassetmanagement.com/resources/glossary. Past performance is no guarantee of future results.

For example, the December 2022 datapoint represents the biggest trailing-year decline in S&P 500's top-five concentration over the sampled timeframe, or about 4.6 percentage points. Over the same one-year period, the Russell RAFI US Large Company Index outperformed the S&P 500 by 11.5%. While the top-five S&P 500 constituents could potentially move even higher than current levels, we believe that today's composition compellingly argues for complementing existing market capitalization-weighted allocations with a Fundamental Index strategy. Doing so might provide diversification and downside mitigation should the fall in concentration levels we have already seen since mid-2025 continue through the remainder of 2026, as forecasted.

"Today's historically high levels of concentration risk within the S&P 500 deserve thoughtful consideration by investors and asset allocators alike."

Strategic next steps—Restoring portfolio equilibrium

Today's historically high levels of concentration risk within the S&P 500 deserve thoughtful consideration by investors and asset allocators alike. As a strategic next step, consider initiating a proactive diagnostic review of your equity allocations to expose any latent imbalances and the potential for "risk creep" that may have been masked by growth-driven performance over the last several years. Then, rather than adopting a binary approach or pursuing a wholesale departure from traditional market cap-weighted index strategies, consider adopting a sophisticated "better-together" framework.

By complementing core market capitalization-weighted holdings with Fundamental Index® strategies, portfolios may become better anchored to tangible economic substance—metrics like cash flow, adjusted sales, and shareholder distributions—rather than risk being tethered to market sentiment shifts. Such an approach might pave the way for a disciplined rebalance into companies whose stock prices don't yet fully reflect their fundamental footprint, potentially positioning your portfolio for more resilient, broad-based participation throughout the remainder of 2026.