Using fixed income ETFs to mitigate risk

Introduction

Investing in a broad range of businesses is less risky than investing in just one—because investing in just one would mean taking on the specific risk and performance of only that business. The same principle applies to investing in a range of asset classes rather than just equities. It spreads the risk. A fixed income exchange-traded fund (ETF) is one easy way to access a broad range of bonds that may help investors diversify, reduce downside risk, and dampen volatility.

A fixed income ETF is a pooled portfolio of bonds that trades daily on an exchange. This means that fixed income ETFs offer intraday trading and continuous transparent pricing while commonly seeking to replicate the return of a chosen index.

A single fixed income ETF can hold hundreds or thousands of bonds, providing potential diversification benefits as well as access at a lower cost than would be possible to obtain by buying each issue separately.

This installment of ETF Know:How shows some of the beneficial effects of adding bonds to a portfolio.

Key terms

While there are benefits to adding fixed income to a portfolio, there are risks, which include:

- Interest rate risk: Changes in interest rates may reduce the value of bonds an investor holds. Interest rate risk increases the longer the time period remaining until a bond’s maturity.

- Credit risk: The risk that a bond issuer will default on paying interest and principal.

- Inflation risk: If inflation increases faster than the income investment, purchasing power declines.

- Liquidity risk: If unable to sell a fixed income security at its market value, the investor may have to sell at a discount to market value.

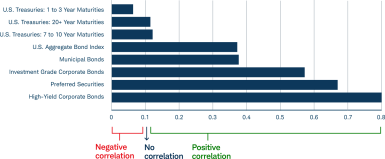

Correlation: Foundation of diversity

To start, it’s helpful to understand correlation, one of the foundational measures of portfolio diversification. Correlation is a measure of the extent to which two investments move in relation to one other. A correlation of +1 indicates a perfect positive correlation. In other words, when one asset moves up or down, the other asset does too. Conversely, a correlation of –1 is a perfect negative correlation. When one asset moves up or down, the other does the opposite.

Adding investments with a lower correlation can help diversify a portfolio and potentially mitigate risk. U.S. Treasuries, municipal bonds, and U.S. corporate bonds have historically shown low to negative correlations to equities as represented by the S&P 500® Index (see chart).

Higher returns come with higher risks

10-year correlation with S&P 500 Index

Source: Charles Schwab, Data by Bloomberg, as of 9/30/2024. Correlations shown represent the correlations of each asset class with the S&P 500 during the 10-year period between September 2014 and September 2024. Correlation is a statistical measure of how two investments have historically moved in relationto each other and range from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance does not guarantee future results.

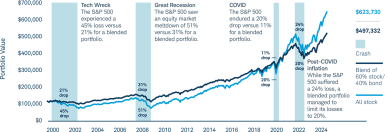

Managing downside risk

While diversification is one benefit of adding fixed income to a portfolio, it’s not the only one. Helping to manage downside risk and volatility are also key advantages. The example below shows a historical performance comparison between an all-stock portfolio and a 60% stock/40% bond portfolio. Through two dramatic downturns, the stock/bond portfolio didn’t decline as much as the all-stock portfolio. In other words, allocating a portion of a portfolio to bonds mitigated downside risk and improved performance.

A balanced portfolio has helped reduce volatility over time

(January 2000-September 2024)

Source: Schwab Center for Financial Research, with data provided by Morningstar, Inc. Stocks are represented by total annual returns of the S&P 500® Index, and bonds are represented by total annual returns of the Bloomberg US Aggregate Bond Index. The 60/40 portfolio is a hypothetical portfolio consisting of 60% S&P 500® Index stocks and 40% Bloomberg US Aggregate Bond Index bonds. The portfolio is rebalanced annually. Returns include reinvestment of dividends, interest, and capital gains. Indices are unmanaged, do not incur fees or expenses, and cannot be invested in directly. For additional information, please see Schwab.com/IndexDefinitions. Diversification does not eliminate the risk of investment losses. Past performance is no guarantee of future results.

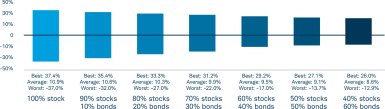

Dampening volatility

Evidence shows that the more bonds are included in the portfolio, the less volatility the portfolio typically experiences. The chart below illustrates the volatility-dampening effect of increasing levels of bonds versus equities in a portfolio. Across the board, adding fixed income securities to a portfolio reduced volatility and the dispersion of returns.

Fixed income investments can lower portfolio volatility

Range of annual returns (1970-9/30/24)

Source: Schwab Center for Financial Research with data provided by Morningstar, Inc. Stocks are represented by total annual returns of the S&P 500® Index, and bonds are represented by total annual returns of the Ibbotson U.S. Intermediate Government Bond Index. The return figures are the average, the maximum, and the minimum annual total return for the portfolios represented in the chart, and are rebalanced annually. Returns include reinvestment of dividends, interest, and capital gains. Indices are unmanaged, do not incur fees or expenses, and cannot be invested in directly. For additional information, please see Schwab.com/IndexDefinitions. Diversification strategies do not ensure a profit and do not protect against losses in declining markets. Past performance is no guarantee of future results.

Summary

Building a diversified portfolio is a sound investment strategy. Fixed income ETFs can help investors diversify while also seeking to protect downside risk, reduce volatility over time, preserve capital, and provide periodic income. Plus, fixed income ETFs typically offer liquidity, price visibility, and low costs.

But fixed income ETFs aren’t risk-free, and diversification doesn’t guarantee against investment loss. Investors should evaluate an investment based on its investment objectives and associated risks.

Explore more ETF insights

Discover ETF Know:How

Browse our full-spectrum curriculum of ETF tools and resources designed to help you boost your knowledge and gain a competitive advantage.

Explore Schwab ETFs

Help your clients get exceptional value from their investments with the product finder.