Chart in a Minute

Use these market charts to support your conversations with clients about asset-allocation opportunities.

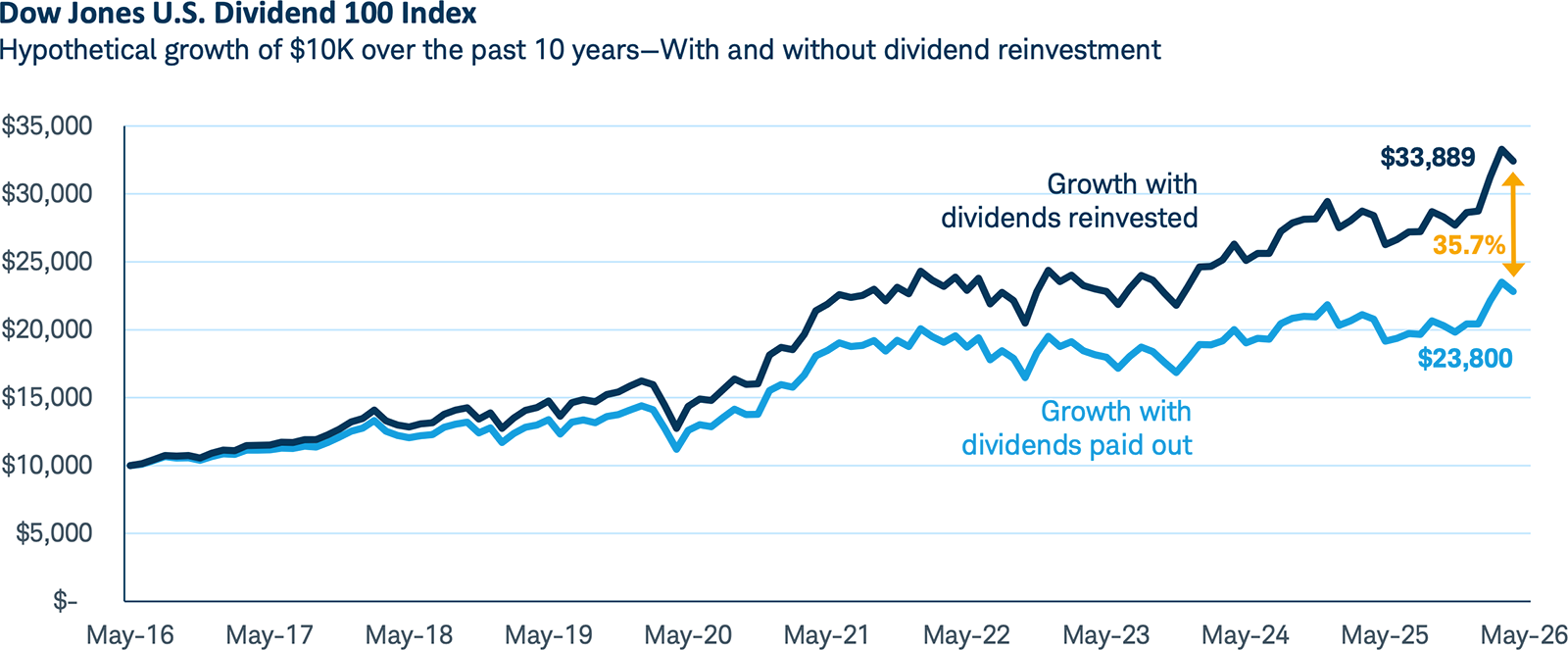

Help clients generate income amid market volatility

June 1, 2026

War with Iran, oil currently around $100 a barrel, and mounting global inflation pressures are fueling market turmoil. Amid the fallout, consider dividend-paying stocks for clients.

Key takeaways:

- Dividend-paying stocks offer many potential benefits, including the ability to generate income even during market volatility, when positive returns can be tough to capture.

- A hedge against inflation is another potential benefit. When reinvested, dividends may continue to grow over time, supporting an investment portfolio if prices on goods and services continue to rise.

- Offering income potential and exposure to quality and value, dividend-paying stocks can potentially help advisors position client portfolios for today’s uncertain and often sentiment-driven market backdrop.