How Could Higher Oil Prices Impact the Muni Market?

Key Points

- Higher oil prices may support some municipal bond issuers by boosting revenues tied to energy production. However, they can also strain household budgets, potentially slowing economic growth and lessening tax collections.

- Bondholders might feel the effects if revenues weaken, reducing an issuer's financial flexibility to meet debt service.

- We don't expect higher oil prices to meaningfully move the municipal market overall. Still, we suggest investors weigh the risks of bonds from smaller local governments where oil and gas are major sources of revenue.

Higher oil prices are an unwelcome sight at the gas pump, but they can benefit some municipal bond issuers. According to Bloomberg, crude oil has risen over 35% since late February and the move has already rippled through other markets. What might higher oil prices mean for municipalities, and what—if anything—should municipal bond investors consider doing about it?

Higher oil prices are likely a mixed bag for the municipal bond market

Higher oil prices are a mixed bag for municipal credit. On the positive side, they can lift revenues tied to energy production through extraction activity or taxes linked to energy prices. On the negative side, higher energy costs can function like an added tax on consumers, especially lower-income households with limited financial flexibility. If gas prices stay elevated for an extended period, spending could slow and economic growth could soften, pressuring sales and income tax collections. These effects are likely to be most acute for issuers in areas with a higher number of lower income households and with less diversified revenue streams.

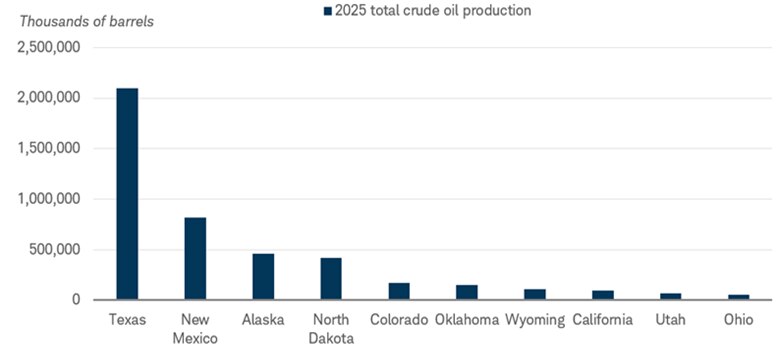

In our view, the impact will differ for states where oil and gas extraction is a major part of the local economy, versus local governments. State revenues are generally less exposed to the impact of higher oil prices—particularly those that do not rely heavily on the energy sector. U.S. oil production is also concentrated: Texas, New Mexico, Alaska, and North Dakota account for roughly 80% of total U.S. crude oil production excluding offshore production, according to the U.S. Energy Information Administration.

Oil production in the U.S. is concentrated in only a few states

Source: U.S. Energy Information Administration.

As of 12/31/2025, which is the most recent data available. 2025 is a sum of monthly data. "Alaska" is the total of "Alaska Field," "Alaska South Field" and "Alaska North Slope."

Local governments that rely heavily on oil and gas production may benefit if higher prices support employment and related revenues. But smaller communities with higher concentrations of lower-income households may be more vulnerable if elevated energy costs slow the broader economy. For bondholders, weaker revenues can translate into less financial flexibility to meet debt service.

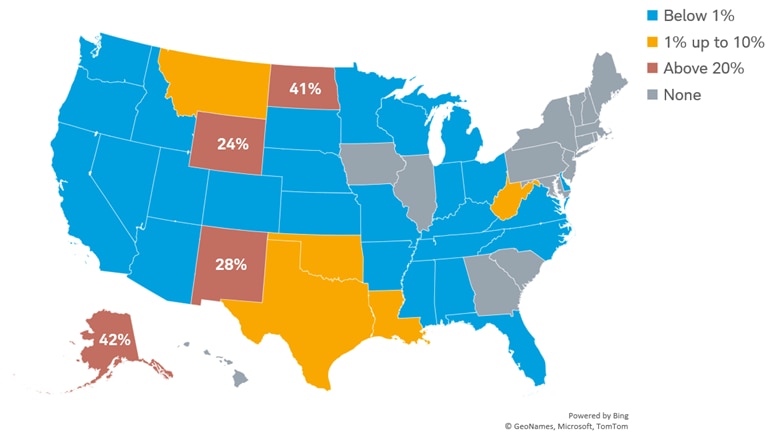

Oil and gas revenues vary substantially from state to state

States can receive revenues from several sources tied to oil and gas production. According to the U.S. Census Bureau's Annual Survey of State and Local Government Finances, 35 states collect severance taxes. Severance taxes are levied on the removal of nonrenewable natural resources, like the extraction and sale of oil and gas.

States typically tax production based on volume, value, or a combination of the two. In states that primarily tax volume, revenues may not change much if production is stable, even when prices move. As the map below shows, severance taxes are a relatively small share of total revenue for most states, but they can represent a meaningful portion for some energy-rich states such as North Dakota, Wyoming, Alaska, and New Mexico.

Severance taxes tend to be a low percentage of revenues for most states

Source: United States Census Bureau.

State and local Government Finances by level of government: U.S. and States: 2017-2023, which is the most recent data available. Note that "Severance taxes" may include items other than oil and gas extraction.

States with greater reliance on severance taxes may benefit more from higher oil prices than states with more diversified revenue streams. Colorado, for example, is the fifth-largest crude oil producer, but severance taxes account for less than 1% of its total tax revenue—so the state's collections may not move much from higher prices alone. Alaska may feel a larger effect, as severance taxes represent more than 40% of total tax collections, according to the United States Census Bureau.

Although severance taxes are generally collected at the state level, some states share a portion with local governments. The formulas to determine how much is shared vary widely by state—and sometimes within a state. Colorado, Montana, and North Dakota, for example, distribute a relatively large share to counties and local governments, while Texas and Wyoming distribute comparatively little.

Two big risks: Boom then bust and a weaker consumer

For some states and local governments, expansion of the oil and gas industry can increase economic concentration in a single sector—creating boom periods followed by busts. It could be a risk if oil prices remain elevated for an extended period and a local population booms due to improved economics. If prices then fall and producers pull back, local governments may be left supporting higher service demands tied to the prior expansion, including law enforcement, emergency services, and administrative capacity.

A second risk is a pullback in consumer spending that weakens economic growth. This is typically a bigger threat in areas with a larger number of lower income households that will likely feel the financial strain of higher energy prices more acutely. Issuers in regions with weaker demographic trends are often lower rated already, and a slowdown could further pressure revenues and reduce financial flexibility. For many municipal bond investors, we generally prefer they consider higher-rated issuers with stronger balance sheets and more resilient revenue bases—often found in areas with growing or stable populations and stronger-than-average financial demographics.

What should municipal bond investors consider now?

In our view, most states are unlikely to see a large, direct boost in tax revenue from higher oil prices. State revenue bases are generally broader and more diversified, which has historically supported financial resilience. However, local governments, where oil and gas production is the primary revenue driver, may experience more pronounced effects—both positive and negative—when oil prices rise.

These communities are often sparsely populated and may have limited revenue diversification. As a result, they tend to issue less debt and may carry lower credit ratings. We don't expect higher oil prices to have a significant impact on the municipal market overall; still, given recent oil-price volatility, investors should evaluate concentration risk in issuers where oil and gas is a major revenue source.

Investors who want additional guidance may consider professional management or consult a Schwab fixed income specialist.

About the author