TIPS for Inflation Protection

Key Takeaways

- Treasury Inflation Protected Securities, or TIPS, are a type of Treasury security whose principal value is indexed to inflation. When inflation rises, the TIPS' principal value is adjusted up. If there's deflation, then the principal value is adjusted lower.

- TIPS yields are "real" yields, already accounting for inflation. Most TIPS yields are positive today.

- While TIPS can offer inflation protection over the long run, they shouldn't be considered an inflation hedge.

- Treasury Inflation Protected Securities, or TIPS, are a type of Treasury security whose principal value is indexed to inflation. When inflation rises, the TIPS' principal value is adjusted up. If there's deflation, then the principal value is adjusted lower.

- TIPS yields are "real" yields, already accounting for inflation. Most TIPS yields are positive today.

- While TIPS can offer inflation protection over the long run, they shouldn't be considered an inflation hedge.

Inflation has proven to be sticky in recent years. While we've moved away from the highs of 2022, many inflation indicators, like the consumer price index (CPI), have held above 2% for five years, and higher oil and gas prices stemming from the conflict in the Middle East are likely to continue to pull it higher over the coming months. That has probably raised some concerns about how to help protect fixed income portfolios from rising consumer prices.

Treasury Inflation-Protected Securities, or TIPS, can help protect against inflation since their principal values are indexed to the CPI. When considering TIPS, however, it's important to understand their unique characteristics and complex nature. In this article, we'll cover TIPS' key characteristics, and then focus on a few key considerations for investors today, including:

- Positive "real" yields

- Breakeven rates that are below the current level of inflation

- Why TIPS can protect against inflation over the long run but shouldn't be considered a short-term inflation "hedge," and

- Individual TIPS versus bond funds

TIPS explained

TIPS are a type of Treasury security whose principal value is indexed to inflation. When inflation rises, the TIPS' principal value is adjusted up. If there's deflation, then the principal value is adjusted lower. Like traditional Treasuries, TIPS are backed by the full faith and credit of the U.S. government.

The coupon payments are based on a percentage of the adjusted principal, so investors can benefit from higher income payments when inflation is rising, as well.

At maturity, however, a TIPS investor would receive the higher of the adjusted principal or the original principal value at issuance. In other words, TIPS won't pay back less than their initial principal value at maturity.

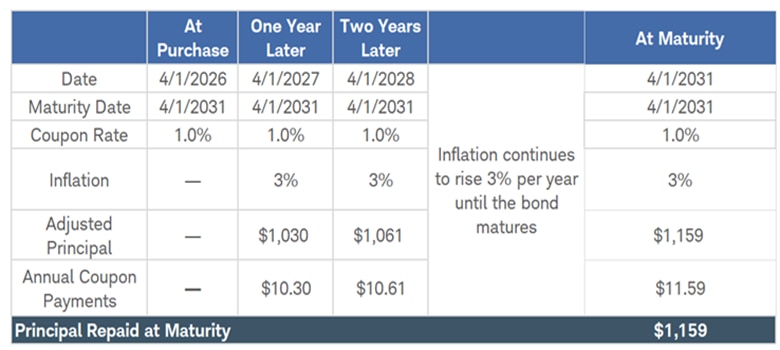

The table below illustrates how the principal value and coupon payments would rise if inflation averaged 3% every year for a hypothetical five-year TIPS. While the initial principal value is $1,000, after one year that principal value would grow to $1,030. The investor would still earn a coupon payment based on the 1.0% coupon rate, but because the principal value would have risen, the coupon payment would be $10.30 at the end of year one. By maturity, the principal value would rise to $1,159 if inflation continued to average 3% per year.

Principal adjustment and coupon payments for a hypothetical five-year TIPS

Source: Schwab Center for Financial Research.

Hypothetical data as of 4/1/2026. The initial hypothetical TIPS principal value is $1,000. For simplicity, this example shows an annual coupon rate, but TIPS make semiannual interest payments. The annual coupon payment equals the fixed coupon rate multiplied by the adjusted principal value. This hypothetical example is only for illustrative purposes.

Here we'll focus on four key considerations for investors looking into TIPS today (keep in mind this is not a comprehensive list):

1. Positive real yields. TIPS yields are "real" yields, already accounting for inflation. The annual rate of inflation over the life of a TIPS ultimately would be added to the stated yield when held to maturity to come up with the annualized "nominal" return. The chart below highlights that the five-year TIPS yield is currently near 1.2%. If inflation, as measured by the CPI, were to average 3% for the next five years, that 3% inflation rate would get added to the roughly 1.2% "real" yield that a five-year TIPS offers today, resulting in a nominal return of 4.2% annually. The higher (or lower) inflation comes in, the higher (or lower) that nominal total return would be.

If you invest in an individual TIPS with a positive real yield and you hold to maturity, you should beat inflation by the magnitude of that real yield.

TIPS yields are at the high end of their 20-year range

Source: Bloomberg.

US Generic Govt TII 5 Year (USGGT5 Index and US Generic Govt TII 10 Year (USGGT10 Index). Daily data from 4/21/2006 through 4/21/2026. Past performance is no guarantee of future results. For illustrative purposes only.

Although the yield for the five-year TIPS shown above is currently positive, the yields for very short-term TIPS turned negative after the Iran war began on February 28, 2026. A negative yield might look like a losing proposition, but the total return could still be positive depending on how high inflation might rise.

2. Breakeven rates. The difference between TIPS yields and yields offered by traditional Treasuries is important to consider when evaluating TIPS. That difference is known as the "breakeven inflation rate" and it can be considered a hurdle rate when trying to determine if a TIPS or a traditional Treasury will outperform the other.

The breakeven rate is the rate that inflation, as measured by the CPI, would need to average over the life of the TIPS for it to outperform a traditional Treasury security. If the CPI averaged more than that breakeven rate, investors would have been better off in a TIPS; if it were below, a traditional Treasury would have made more sense.

Five-year TIPS breakeven rate

Source: Bloomberg, using weekly data from April 21, 2011 through April 21, 2026.

US Generic Govt TII 5 Yr (USGGBE05 Index). Past performance is no guarantee of future results. For illustrative purposes only.

Over the last 15 years, the average five-year breakeven rate was 1.98%, so the current rate is above average. However, it's below the current inflation rate, as CPI rose by 3.3% in the twelve months ending in March 2026.

When considering breakeven rates, this helps frame the potential of a TIPS performance relative to nominal Treasuries. Investors simply looking for inflation protection to sleep better at night might prefer to focus on the real yields offered.

3. Inflation protection is not the same thing as a short-term inflation "hedge." TIPS' principal values adjust up (or down) with changes in the CPI, but their prices can still fluctuate in the secondary market. That means short-term performance may differ from what the inflation rate suggests.

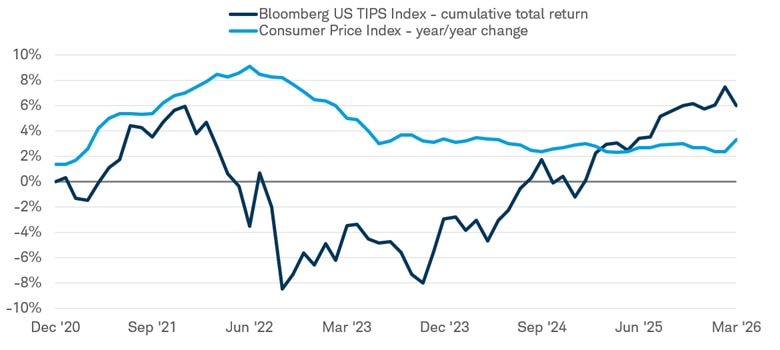

The chart below highlights the total return of the Bloomberg US TIPS Index, beginning at the end of 2020. Total returns were positive for most of 2021 as inflation rose, but price declines pulled total returns into negative territory later on in 2022. That's likely not the performance investors were expecting given that the year/year change in the CPI peaked at 9.1% in June 2022. The large price declines more than offset the rise in inflation-adjusted principal values. This is a key reason why TIPS can protect against inflation over the long run but shouldn't be considered an inflation "hedge" over the short run.

The combination of higher prices from falling TIPS yields and the inflation adjustments have helped boost returns lately, however, and the cumulative total return of the Bloomberg US TIPS Index since the end of 2020 is positive again.

TIPS total returns have rebounded

Source: Bloomberg, using monthly data as of from 12/31/2020 through 3/31/2026.

Total returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

TIPS are designed to help protect purchasing power over time because their principal adjusts with changes in the CPI. But that inflation adjustment does not eliminate short-term price volatility. Because TIPS trade in the secondary market, their prices remain sensitive to changes in interest rates, especially real yields. As a result, short-term returns can differ meaningfully from inflation itself.

Maturity plays an important role in how TIPS behave over shorter time horizons. Although all TIPS are linked to the same CPI-based inflation adjustment, shorter-maturity TIPS generally tend to be less volatile and are often less affected by changes in real yields. (Remember, bond prices and yields move in opposite directions and, all else equal, the prices on bonds with shorter maturities are less sensitive to interest rate changes than those with long-term maturities.) As a result, their returns may track realized inflation more closely over short periods than those of longer-maturity TIPS. Longer-maturity TIPS carry more interest rate risk, so over short periods their returns may be driven more by changes in real yields than by the inflation adjustment itself.

That was evident when inflation reached multi-decade highs in 2022 and 2023 but broad TIPS indexes posted negative total returns. During this time, real yields moved sharply higher as the Federal Reserve tightened policy aggressively, and those higher yields pushed prices lower by more than the inflation-driven increase in principal.

Over longer periods, inflation adjustments compound and the effects of price volatility generally become less important, particularly for bonds moving closer to maturity. That reinforces the role of TIPS as long-term inflation protection rather than as a precise short-term inflation hedge.

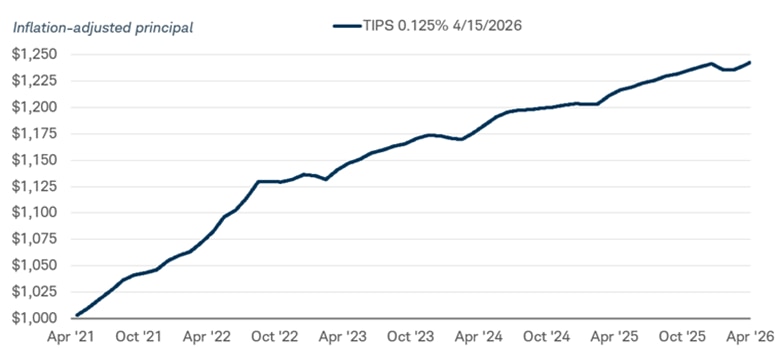

Those negative returns in the chart above aren't indicative of the whole TIPS market, especially individual TIPS. Price fluctuations in the secondary market are temporary as long as you hold to maturity. Although TIPS prices initially fell leading up to and during the Fed's rate hiking cycle, the principal values have risen. And bond prices tend to be self-healing—barring default—meaning a drop in price on the heels of rising yields is eventually reversed as the bond gets closer to maturity and its price amortizes toward its par value. Consider the TIPS depicted in the chart below that was issued in April 2021 and matured in mid-April 2026 since it was issued, a more than 22% increase.

The inflation-adjusted principal value of TIPS has risen lately

Source: Bloomberg, using daily data from 5/1/2021 through 4/15/2026.

Treasury Inflation Protected Security, 0.125% coupon rate, April 15, 2026 maturity date and US Inflation Indexed CPI Ratio 5-Year Bonds Issued April 2021. The line in the chart represents the inflation-adjusted principal value, using the CPI index ratio for this TIPS multiplied by its starting value of $1,000. Past performance is no guarantee of future results. This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned are not suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions. Any investments reflected are for illustrative purposes only. Individual situations will vary and are no guarantee of future performance or success. Not intended to be reflective of results you can expect to achieve.

Although prices fell sharply when TIPS yields rose, looking at the secondary market price doesn't tell the whole story since it doesn't include the inflation adjustment. The chart below illustrates this phenomenon. The blue line in the chart below represents the price of this TIPS in the secondary market and the red line multiplies that price by the TIPS' inflation index ratio (showing the inflation-adjusted value). Initially prices had declined more than the inflation adjustment. The average price of this TIPS began to hold relatively steady in late 2022, then gradually increased, and has since held near $100 until it matured on April 15, 2026. While the secondary market price held near $100 since the beginning of 2025, the inflation-adjusted principal increased through the bond's maturity as inflation rose. The chart below and the chart above both illustrate how holding individual TIPS to maturity can help protect against inflation surges.

TIPS secondary market prices compared to its inflation-adjusted price

![Chart shows the secondary market price of a TIPS with a 0.125% coupon compared with its inflation-adjusted price.]](https://www.schwabassetmanagement.com/sites/g/files/eyrktu361/files/Chart%206_75.png)

Source: Bloomberg, using daily data from 4/30/2021 through 4/15/2026.

Treasury Inflation Protected Security, 0.125% coupon rate, April 15, 2026 maturity date and US Inflation Indexed CPI Ratio 5-Year Bonds Issued April 2021. The blue line represents the secondary market price of the TIPS, while the red line multiplies that by the inflation adjustment. Past performance is no guarantee of future results. This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned are not suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions. Any investments reflected are for illustrative purposes only. Individual situations will vary and are no guarantee of future performance or success. Not intended to be reflective of results you can expect to achieve.

4. Individual TIPS versus bond funds. There are pros and cons to both holding individual TIPS or investing through a mutual fund or exchange-traded fund (ETF). One benefit that individual bonds offer—when holding bonds to maturity—is the ability to "look through" price declines in the secondary market, knowing the bonds will mature at their par value. TIPS are backed by the full faith and credit of the U.S. Government, so they are highly likely repaid at maturity, but inflation-protected bond funds do not provide such a guarantee. Bond funds generally do not offer a predictable value at a future date. A drawback, however, is that building a diversified portfolio of individual TIPS can require more time, larger investment amounts, and ongoing portfolio management than investing through a fund.

Consider once again the TIPS example shown above—it was issued in April 2021 and its inflation-adjusted price rose by more than 20% since it was issued, and that doesn't consider the semiannual interest payments. Over the same time frame, the Bloomberg US TIPS Index has gained just 7.2%. Keep in mind that past performance is no guarantee of future results.

What to consider now

With inflation proving sticky and likely to reaccelerate over the coming months, TIPS appear relatively attractive. Real yields are still positive, and breakeven rates are below the current rate of inflation. Investors can earn higher income today with TIPS than they generally could have earned for the 10-year period leading up to the COVID-19 pandemic, while also helping to protect against inflation over the long run.

For investors who invest in TIPS through ETFs or mutual funds, the value of the funds can fluctuate, but that doesn't mean you need to abandon your holdings (if you're interested in researching TIPS funds you can use Schwab's ETF Select List® to get information about ETFs that offer access to TIPS. Before considering any fund, you should consult the fund's prospectus to understand its investment objectives, risks, charges, and expenses). If yields were to in fact rise from here and the funds rebalance their holdings, investors may be rewarded with higher income payments to help offset potential price declines, while additional inflation increases would result in positive principal adjustments to the underlying holdings.

About the author