CD or Treasury? 5 Factors to Consider

Key Takeaways:

- Both CDs and Treasuries might be good choices for investors looking for relatively conservative investments that may provide steady investment income.

- Before deciding between CDs and Treasuries, investors should consider their objectives and potential benefits and risks.

- One strategy to consider when investing in CDs or Treasuries is a ladder, which is a portfolio of individual Treasuries or CDs that mature on different dates. This can help minimize exposure to interest rate fluctuations.

Two of the historically safest types of fixed income investments are certificates of deposit (CDs) and Treasury bonds. Both CDs and Treasuries can be a good choice when you want relatively conservative investments that can provide steady, predictable investment income—but how should you decide between the two?

Before choosing CDs or Treasuries, we suggest you first start with your objectives. Not considering your objectives before investing is like taking a road trip and only being concerned about the tires on the car—not where you're going. The benefits of both CDs and Treasuries are that they can generate income, protect your principal, and help diversify your portfolio. Additionally, Treasuries can have tax benefits when compared to CDs. However, brokered CDs and Treasuries are fixed income investments and subject to similar risks as other fixed income investments. For example, if interest rates rise, the price of a brokered CD or Treasury will fall and if you need the investment prior to maturity and have to sell it, you may lose money.

When considering between the two investment options, there are five factors that investors should consider.

1. Security

Both CDs and Treasuries are very high-quality investments and backed by some form of a guarantee. CDs are bank deposits that pay a stated amount of interest for a specified period of time and promise to return your money on a specific date. They are federally insured and issued by banks and savings-and-loans institutions. CDs are backed by FDIC insurance up to $250,000 per bank per depositor, principal and interest. There are bank-issued CDs and brokered CDs. The two are similar but have some important differences.

You can purchase multiple CDs from different banks while still holding them in the same account type to protect more than $250,000. For example, if you own two CDs in your brokerage account, $250,000 from one bank and $250,000 from a second bank, and you have no other deposits at those banks, you're covered for $500,000 even though they're held in the same account. We suggest that if you're investing more than $250,000 in CDs, be sure that you're not exceeding the FDIC insurance limits at each individual bank.

Treasuries, on the other hand, are issued by the U.S. Department of the Treasury and are backed by the full faith and credit of the U.S. government to an unlimited amount. Like CDs, they pay a stated amount of interest for a specified period of time and promise to return your money on a specific date. There's generally ample availability of Treasury bonds, whereas the availability of CDs can be limited and depends on the bank's capital needs and other factors. Therefore, there can be instances where there aren't enough CDs to insure an amount greater than the $250,000 FDIC insurance limits. In these instances, Treasuries could be the more appropriate option.

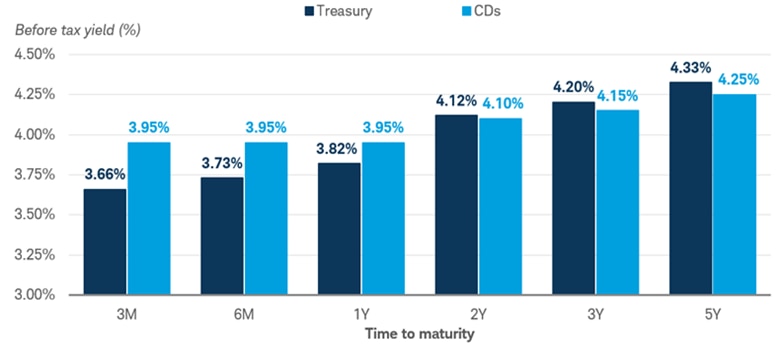

2. Yields

Yields, as represented by the 10-year U.S. Treasury, have mostly been in a range since October 2024 but are still elevated relative to the past 15 years,1 making both CDs and Treasuries a much more attractive option than in prior years. Currently, CDs maturing in a year or less yield somewhat more than Treasuries. However, at maturities beyond one year, Treasuries yield slightly more before taxes.2 Therefore, all things considered, it might make more sense to choose CDs over Treasuries for shorter-term investments, but it depends on your situation. It's also important to note that yields change over time so this relationship may not always hold.

Treasuries relative to CD yields

Source: Bloomberg for Treasury yields and Schwab BondSource ™ for CD yields, as of 5/19/2026.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve. CDs were chosen because they were the highest yielding, new issue CD for each maturity, based on a $25,000 purchase amount. New issue CDs have a selling concession that varies. Secondary CDs may have a transaction fee. CDs may not be available in all states and the availability of CD inventory may change. Treasury securities were chosen because they are on the run Treasuries; "on the run" means the most recently issued U.S. Treasury bonds or notes of a particular maturity. USGG3M Govt for 3-month Treasury, USGG6M Govt for 6-month Treasury, USGG12M for 12-month Treasury, GT2 Govt for 2-year Treasury, GT3 Govt for 3-year Treasury, and GT5 Govt for 5-year Treasury. Past performance is no guarantee of future results.

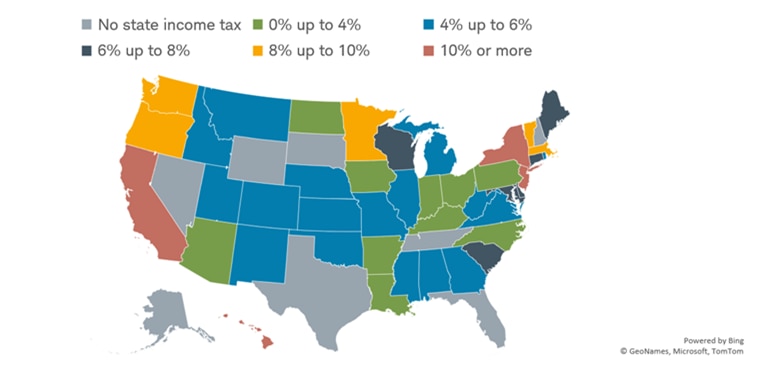

3. Taxes

Treasuries can offer tax benefits that CDs do not. Income from Treasuries are exempt from state income taxes, whereas CDs are subject to both federal and state income taxes. As a result, investors who are choosing between the two options should factor in what account type they are investing in, and also what their state tax rate is. If investing in a tax-sheltered account, like an individual retirement account (IRA) or a 401(k), the tax benefits that Treasuries provide don't apply, because earnings in these types of accounts are not subject to income taxes.

However, if investing in a taxable account, like a brokerage account, the impact of state income taxes can tip the scales one way or the other. For investors in high-tax states, like New York or California, after considering the impact of state taxes, investors may be able to achieve a higher after-tax yield with Treasuries.

For example, assume a one-year CD currently yields 3.95%, compared to a one-year Treasury that yields 3.82%.1 For an investor in the top tax bracket in California, which has a 13.3% state tax rate, after the impact of state taxes, the CD yields 3.42%. In this instance, the investor can achieve a higher after-tax yield with the Treasury versus the CD.

Investors in high-tax states may want to consider Treasuries over CDs due to their tax benefits

Tax Foundation, as of 1/1/2026.

4. Maturities

Treasuries have maturities ranging from as little as four weeks to as long as 30 years. On the other hand, the availability of CDs beyond five years is limited in many instances. For investors that desire a greater selection of maturities, Treasuries can make more sense.

5. Liquidity

We usually recommend holding a CD or Treasury to maturity, but situations can arise where an investor needs to "break" a CD or Treasury prior to maturity. Unlike CDs purchased directly from a bank, brokered CDs are bought and sold on a secondary market. If you need access to the funds you invested in a CD prior to maturity, you may be able to sell the CD at the current market rate by requesting bids on your CD through your broker. If you decide to sell, you'll receive the bid price plus any accrued interest. There are no guarantees that you'll get what you originally paid for the CD and there may be a fee to sell the CD.3

Treasuries can also be bought and sold on a secondary market; however, it's a much more active market than the CD market, which means there are more availability of quotes which generally lead to tighter bid/ask spreads. A Treasury investor could still lose money if they had to sell a Treasury prior to maturity, but the Treasury market is a much more liquid market than the CD market and therefore much easier to sell if needed.

We generally suggest that if there's the possibility that you may need the money prior to maturity, consider Treasuries over CDs because they're more liquid.

What to consider

One strategy to consider when investing in CDs or Treasuries is a ladder. A ladder is a portfolio of individual Treasuries or CDs that mature on different dates. This can help minimize exposure to interest rate fluctuations. Additionally, investors may want to consider a separately managed account (SMA) that can help build and manage a ladder. For help selecting investments for your particular situation, reach out to a Schwab representative.

1 Schwab BondSource and Bloomberg as of 5/19/2026.

2 Based on the highest yielding new issue CD available on Schwab BondSource™ as of 5/19/2026 for 3-month, 6-month, and 12-month maturities compared to USGG3M Govt for 3-month Treasuries, USGG6M Govt for 6-month Treasuries, USGG12M for 12-month Treasuries.

3 New-issue CDs have a selling concession which can vary by maturity/term. Secondary CDs frequently have transaction fees.

About the author