2022 Mid-Year Muni Market Outlook

There's good news and bad news in the municipal bond market today. The bad news is that it has been the worst start to a year in more than 40 years. The good news is that the sharp selloff has created potential opportunities that largely haven't existed for 15 years.

During the second half of the year, we believe the muni market may present opportunities. We suggest that muni investors consider taking advantage of the recent selloff by moving up in both credit quality and coupon structure, and moderately extending duration if they have been investing in very short-term munis.

Absolute yields have risen sharply

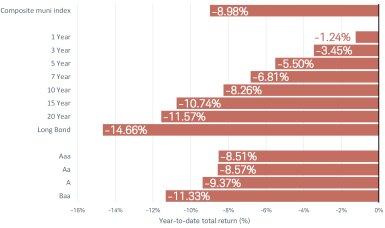

There's no denying that the start to the year has been brutal for municipal bond investors. The broad municipal bond index is down over 9%, led by lower-rated and longer-term munis, as illustrated in the chart below. It's not just long-term munis that have fared poorly; even returns for very short-term munis, which are usually very stable, are negative for the year. To put that in context, in the nearly 30-year history of the very short-term muni index, it has never posted a negative year-to-date (YTD) total return through the end of June.

Year-to-date total return is negative across the yield curve

Source: Bloomberg

Components of the Bloomberg Municipal Bond Index, total return from 12/31/21 to 6/30/22. Past performance is no guarantee of future results.

Returns should improve in the second half of the year

Although the start of the year has been rough, we don’t expect it to continue to the same degree during the second half of the year. Munis have performed poorly because Treasury yields rose sharply due to the Federal Reserve aggressively tightening policy in response to surging inflation. The Fed will continue to hike rates this year and likely into next year, but longer-term bonds already have priced in aggressive tightening, in our view. During the second half of the year, we don't expect yields to continue to move up as sharply as they have in the first half, which should slow the pace of negative returns for munis.

Fresh opportunities

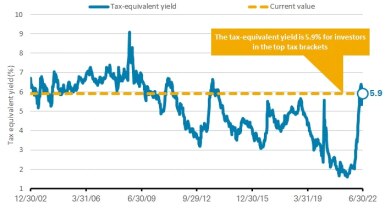

The rise in yields has created potential opportunities that largely haven't existed in the past 15 years. For example, the tax-equivalent yield—which is the yield a taxable bond would need to offer to compare favorably with a tax-exempt muni—is currently near 6% for investors in the top tax bracket. That's up more than 220 basis points1 since the start of the year.

The tax-exempt yield for the broad muni market is roughly 6% for investors in the top tax brackets

Source: Bloomberg Municipal Bond Index

As of 6/30/22 using weekly data. Munis assume a federal tax rate of 35% from 2006 to 2012, 39.6% from 2013 to 2017, and 37% from 2018 to 2022, a 5% state income tax rate, and a 3.8% ACA tax from 2013 to 2022. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Past performance is no guarantee of future results. For illustrative purposes only.

Intermediate-term munis look more attractive now

If we're correct that the bulk of the rise in yields is behind us, we think it's appropriate to target a closer-to-benchmark duration. Duration is a measure of how a bond's price will change relative to interest rates. Bonds with longer durations are generally more volatile than bonds with shorter durations.

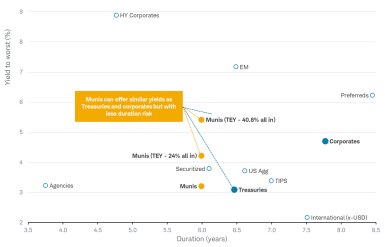

Compared to other fixed income investments, extending duration in the muni market looks attractive. One metric we track is the yield relative to duration. All things being equal, the more yield per unit of duration, the more attractive the fixed income security is. Muni yields relative to duration stack up well against other fixed income investments. For example, the yield to worst2 on the Bloomberg Municipal Bond Index is roughly 3.3%, but after adjusting for taxes, the tax-equivalent yield can be as high as 5.6% for an investor in the top federal tax bracket. However, the duration of the index is slightly longer than six years. In other words, investors are getting better compensated for taking interest-rate risk in the muni market relative to most other markets. The chart below differs from the tax-equivalent yield chart above because it does not include a state tax rate. The tax-equivalent yield in the chart below would be near 6% if a state tax rate were included.

Munis yields relative to their durations are attractive

Source Bloomberg, as of 6/30/22.

The tax-equivalent-yield (TEY – 40.8%) for munis assumes a 37% Federal tax rate and 3.8% ACA tax rate. The tax-equivalent-yield (TEY – 24%) for munis assumes a 24% Federal tax rate. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. See Important Disclosures below for a description of the indexes used. Past performance is no guarantee of future results. For illustrative purposes only.

The shape of the yield curve makes adding duration attractive

In addition, the slope of the muni yield curve is positively sloped compared to the Treasury yield curve, making munis worth consideration when adding duration to fixed income portfolios. As illustrated in the chart below, the difference in yields between two- and 10-year Treasuries is near zero, whereas it's more than 80 basis points for AAA-rated munis. In other words, a muni investor is better compensated for moving out the yield curve relative to a Treasury investor.

The AAA muni curve is more positively sloped compared to Treasuries

Source: Bloomberg, as of 6/30/2022

Munis are represented by the Bloomberg BVAL AAA Muni Curve. Past performance is no guarantee of future results. For illustrative purposes only.

Credit risk is low, but we suggest moving up in credit quality

By most measures, credit risk in the broad muni market is stable to strong. The ongoing economic recovery combined with multiple rounds of fiscal aid following the onset of the COVID-19 pandemic have strengthened state and local governments finances. Tax revenues have surged, rainy-day funds are at near-record levels, and pension plans, in aggregate, are in their best shape in nearly a decade.

Although credit quality is stable to strong, we believe it's appropriate to move up in credit quality and focus the bulk of a muni portfolio on higher rated (AA/Aa and AAA/Aaa) issuers for two primary reasons:

1. The risks of a recession are rising

Although fundamentals are currently strong, they could weaken if there's a recession or an economic slowdown. While recessions are impossible to predict, we think the risk of a recession occurring sooner rather than later has picked up. If a recession, or even a slowdown in economic growth, does occur, it would negatively impact the finances of lower-rated issuers more than higher-rated issuers, in our view. Therefore, we think that it's appropriate to focus more on higher-rated issuers given the potential headwinds.

2. The rise in yields and credit spreads means investors no longer need to stretch for yield in the lowest-rated parts of the market

Earlier this year we had suggested targeting some BBB/Baa rated issuers in moderation. As the year developed, we grew more cautious of lower-rated issuers mostly because yields for higher-rated issuers were becoming more attractive.

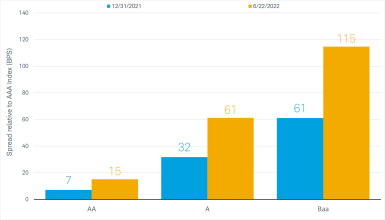

For example, at the beginning of the year, a generic AA rated muni yielded only seven basis points more than a AAA rated muni and a A rated muni yielded 32 basis points more than a AAA muni. Our view was that spreads for AA rated issuers were so tight that investors weren’t being adequately compensated for taking on the additional credit risk in AA and A rated issuers.

That has changed. Spreads for AA rated issuers and A rated issuers have increased to 19 and 65 basis points, respectively. Although spreads are still below their longer-term averages, the move up makes them more attractive today.

The rise in spreads makes higher-rated issuers more attractive, in our view

Source: Bloomberg

Components of the Bloomberg Municipal Bond Index, as of 6/30/2022. For illustrative purposes only. The “spread” is the difference in yield to worst between the AAA and AA, A, or Baa indices. Difference in yields may be due to different factors such as maturities, durations, or other factors.

Consider tax-loss harvesting

Tax-loss harvesting is a strategy that isn't usually associated with municipal bond investing. However, given the steep year-to-date price declines, we think muni investors should consider it. Tax-loss harvesting is a strategy in which an investor realizes a capital loss to offset capital gains elsewhere in their portfolio, with the goal of reducing their tax bill and better positioning the portfolio going forward. We are not advocating abandoning the muni market if you've experienced losses this year. However, consider realizing those losses and reinvesting the proceeds into other municipal bonds that aren’t considered a substantially identically security. Before implementing such a strategy, we would suggest reviewing Publication 550 or consulting with your tax advisor.

Higher coupons can mean higher income

Investors in individual bonds should also consider swapping out of low-coupon munis for higher-coupon munis, assuming all else is equal. Prices for higher-coupon munis should hold up better than those for lower-coupon munis if rates move higher. Although we believe longer-term rates aren’t likely to rise as sharply as they have to start the year, there's a risk that they will continue to increase.

If rates continue to rise, prices will fall, and the prices of lower-coupon bonds may fall below the de minimis threshold. The de minimis rule says that if you buy a muni at a large discount you may have to pay a higher tax rate on the accretion back to par, which can take a bite out of your after-tax yield.

If an investor owns an individual bond that drops in price and crosses the de minimis tax threshold, they won't have to pay the de minis tax. However, if they chose to, or had to, sell it, it would likely be at a lower value and with less liquidity than a muni that wasn’t subject to the de minimis tax. Therefore, we think investors in lower-coupon bonds should consider now an opportunity to swap out of low coupon bonds in favor of higher coupon bonds because higher coupon bonds are less likely to fall below the de minimis threshold.

Summing it up

We believe that the bulk of the sharp selloff in the muni market is likely behind us. Going forward, we don't expect yields will continue to rise as sharply as they did in the first half of the year. Although we think the muni market will be an area of opportunity in the second half of the year, we think it's prudent to move up in credit quality and coupon structure, focus on a benchmark duration, and consider tax-planning strategies.