Are TIPS Worth Considering Now?

Inflation has risen at its fastest rate in decades, but Treasury Inflation-Protected Securities are still down sharply this year. What gives?

Treasury Inflation-Protected Securities, or TIPS, can help protect against inflation over the long-run, but over the short run, their performance may be dictated more by price declines in the secondary market than by the inflation-driven principal adjustment. That's been the case so far this year.

When considering TIPS, it's important to understand their unique characteristics and complex nature. Below we'll discuss what drove the performance this year, and what investors can expect going forward. While the start of the year has been forgettable for TIPS investors, yields are now back in positive territory, and TIPS can help play an important role in protecting your portfolio from inflation over the long run.

TIPS: the basics

TIPS are a type of Treasury security whose principal value is indexed to inflation. As the level of the Consumer Price Index (CPI) rises and falls, so too does the value of a TIPS. Like traditional Treasury securities, TIPS have fixed coupon rates based off of the principal value—so coupon payments rise or fall with the level of the CPI as the principal value fluctuates.

This characteristic helps TIPS protect investors against the effects of inflation, because they'll be rewarded with a higher principal value at maturity as well as growing coupon payments if inflation is rising. (Traditional Treasuries simply mature at their $1,000 par value.) The opposite is true as well: In deflationary periods, the principal value of a TIPS will fall, resulting in smaller coupon payments. At maturity, however, a TIPS investor would receive either the adjusted higher principal or the original principal value. In other words, TIPS never pay back less than the initial principal value at maturity.

High inflation, negative returns

TIPS returns are in the red this year as price declines have more than offset the inflation adjustment to TIPS principal values. While they've outperformed traditional Treasuries, the Bloomberg U.S. Treasury Inflation-Protected Notes Index is still down sharply this year and is off to its worst start to a year1 since its inception in 1997. That's likely caught many investors off guard, considering the Consumer Price Index rose by more than 8% in the twelve months ending April 2022.

TIPS have outperformed nominal Treasuries this year, but total returns are still negative

Source: Bloomberg.

Total returns from 12/31/2021 through 5/18/2022. Bloomberg U.S. Treasury Index (LUATTUU Index) and the Bloomberg U.S. Treasury Inflation Protected Notes Index (LBUTRUU Index). Total returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

The total return of a TIPS over a specific time period consists of income payments, price change, and the inflation adjustment to its principal value. The TIPS index is down this year because the inflation adjustment to TIPS principal values has been more than offset by the drop in TIPS prices. TIPS are still bonds, and their prices and yields move in opposite directions.

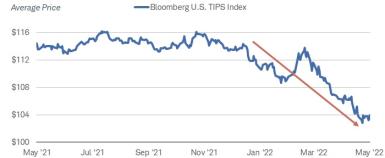

The Bloomberg U.S. TIPS Index lost 5.9% through May 18, 2022. The plunge in TIPS prices was the culprit—the average price of the TIPS index closed 2021 at $114.2 and then fell to $104.0, a decline of 8.9%. The rise in the CPI has helped offset some, but not all, of that price decline, as has the 0.22% year-to-date coupon return. (TIPS generally have low coupon rates given the low or negative TIPS yields.) In short, the year-to-date rise in the Consumer Price Index hasn't been enough to offset the steep price declines.

TIPS prices have declined more than the principal has been adjusted higher

Source: Bloomberg, using daily data as of 5/18/2022.

Past performance is no guarantee of future results.

TIPS yields are on the rise

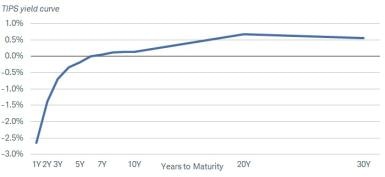

Many TIPS offer positive yields today, a marked improvement compared to the last two years. From March 2020 through the end of April 2022, most TIPS yields were negative. If you invest in a TIPS with a negative yield, you're essentially locking in an inflation-adjusted loss if held to maturity. That's less of an issue today, where yields on TIPS with maturities of seven years and beyond are now above zero.

TIPS with maturities of 7 years or more have positive "real" yields

Source: Bloomberg, as of 5/18/2022.

While those low, or even negative, "real" yields might not sound too attractive, consider the yields on nominal Treasuries. The 5-year nominal Treasury offers a yield of roughly 2.8%, but when the high rate of inflation is factored in, that inflation-adjusted yield is well below zero.

A low "real" yield can still produce high nominal returns. Consider the 10-year TIPS, which currently yields roughly 0.12%. If held to maturity, the inflation adjustment must be considered as well. If inflation averages 3% over the next 10 years, for example, the annualized nominal total return would be closer to 3.12%.

While the rise has presented investors a more attractive entry point, TIPS yields could still rise a bit further. While nominal Treasury yields are close to their peaks from the last Federal Reserve rate hike cycle, TIPS yields remain below the pre-COVID-19, five-year average. As the Fed pares back its TIPS purchases as it embarks on quantitative tightening, and if inflation expectations decline, TIPS yields could keep rising, potentially pulling prices even lower.

The 10-year TIPS yield is in positive territory for the first time since early 2020

Source: Bloomberg, using weekly data as of 5/19/2022.

US Generic Govt TII 10 Yr (USGGT10Y Index). Past performance is no guarantee of future results.

TIPS vs. traditional Treasuries

TIPS can be compared to nominal Treasuries through the breakeven inflation rate. The breakeven rate is the difference between the yield of a nominal Treasury and the yield of a TIPS with a similar maturity. TIPS yields tend to be lower than nominal Treasury yields because investors can benefit when inflation rises, as the principal values adjust higher; nominal Treasury principal values and coupon payments are fixed regardless of the level of inflation.

For TIPS investors, the breakeven rate can be considered a hurdle rate—it's what inflation would need to average over the life of the TIPS for it to outperform the nominal Treasury. The 10-year breakeven rate is currently around 2.7%. If the CPI averages more than 2.7% for the next 10 years, then the TIPS would outperform the nominal 10-year Treasury. Likewise, if CPI averaged less than 2.7%, then the nominal 10-year Treasury would outperform.

TIPS breakeven rates are near all-time highs

Source: Bloomberg using weekly data as of 5/13/2022.

US Breakeven 10 Year (USGGBE10 Index).

The breakeven rate can be helpful based on your own inflation expectations. How high do you think inflation will rise, and for how long? If you're expecting inflation to remain elevated for a while, then TIPS can still make sense despite breakeven rates being near all-time highs.

What to do now

Consider TIPS if you're worried that inflation will remain high or if you're looking to help protect against an unexpected rise in inflation. With TIPS principal values indexed to the rate of inflation, they can help portfolios keep pace with inflation in a way that most other investments can't.

Most importantly, remember that TIPS can help protect portfolios from inflation over the long run, but over the short run price fluctuations may be the key driver of performance. Many TIPS yields are now positive, which makes them more attractive, but there's a risk that yields will continue to trend gradually higher and prices decline. For individual TIPS holders, any potential price declines might not matter if they're held to maturity. For those who invest in TIPS through ETFs or mutual funds, that could mean modest declines from here, but that doesn't mean you need to abandon your holdings. If yields rise and the funds rebalance, investors may be rewarded with higher income payments to help offset some of the potential price declines.