Tax efficiency in exchange-traded funds

Introduction

Exchange-traded funds (ETFs) tend to be more tax efficient than traditional mutual funds, due to their unique fund structure and redemption mechanism. By understanding the mechanics behind ETFs, investors can potentially limit taxable events caused by their investment funds.

ETFs are generally tax efficient for three reasons:

1. Most ETFs track an index.

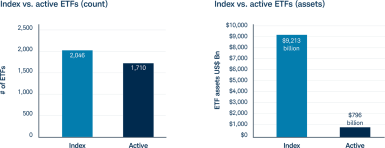

As of September 30, 2024, 54% of all ETFs tracked an index, and 92% of all ETF assets were tied to indexed products.1 Index-tracking funds tend to have less securities turnover compared with actively managed funds. This helps index-tracking funds minimize incurring capital gains and thus capital gains distributions to investors.

Source: Morningstar Direct, September 30, 2024.

2. ETFs are exchange traded.

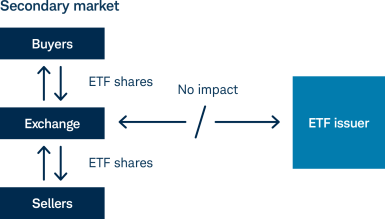

Like stocks, ETFs are traded throughout the day on exchanges, such as the NYSE Arca and Nasdaq. When investors want to sell their ETF shares, they usually sell them on an exchange without transacting directly with the ETF provider. The ETF shares are simply transferred from the seller to the buyer, and the underlying securities held in the ETF are unaffected.

Key terms

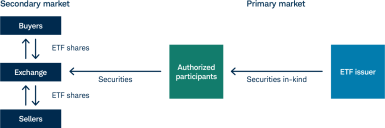

- Authorized participants: Large institutions that transact directly with the ETF provider to create or redeem shares of an ETF.

- Creation unit: The minimum number of ETF shares required to transact directly with the ETF issuer. This is typically at least 25,000 shares.

- Primary market: The direct exchange of securities for shares of an ETF between authorized participants and ETF issuers.

- Secondary market: The national markets system (e.g., the stock exchanges and other venues where listed securities can be traded). Shares of ETFs are continuously bought and sold throughout the day on an exchange or other trading venue by investors.

3. ETFs have a unique redemption mechanism.

When a mutual fund receives a redemption order from an investor, the fund may have to sell some of the securities it holds to raise capital to deliver cash to the investor. In contrast, an ETF’s unique redemption mechanism through authorized participants (APs) commonly allows the ETF to divest some underlying securities without having to sell those securities from the fund.

The AP effectively acts as an intermediary in the ETF redemption process. During a redemption, the ETF issuer delivers the underlying securities in the redemption basket to the AP.2 The AP, as opposed to the ETF issuer, sells those securities on an exchange in a seamless process with little to no impact to the investor’s year-end calculation of capital gains or losses.

Summary

Because ETFs maintain unique characteristics from mutual funds, such as trading throughout the day on an exchange and working with APs on redemptions, they have historically distributed lower capital gains than mutual funds. As the majority of ETFs are linked to an index, they may have lower trading volumes than an actively managed fund. All of these aspects combined have created an investment tool that has demonstrated tax efficiency for investors since their initial inception in 1993.

Explore more ETF insights

Discover ETF Know:How

Browse our full-spectrum curriculum of ETF tools and resources designed to help you boost your knowledge and gain a competitive advantage.

Explore Schwab ETFs

Help your clients get exceptional value from their investments with the product finder.