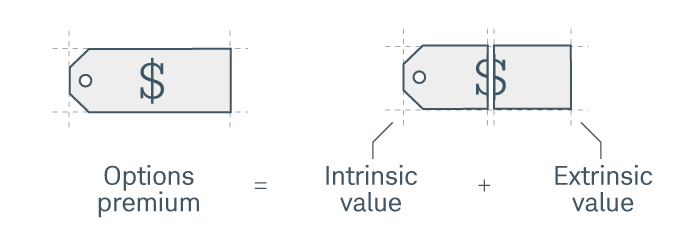

Intrinsic and Extrinsic Value

We've talked about the factors that comprise the options premium (price of the underlying security, time, and implied volatility). Option traders have another way of looking at the premium: intrinsic and extrinsic value.

Intrinsic value

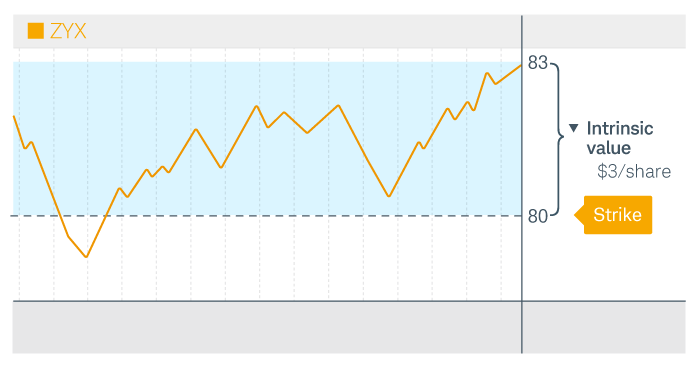

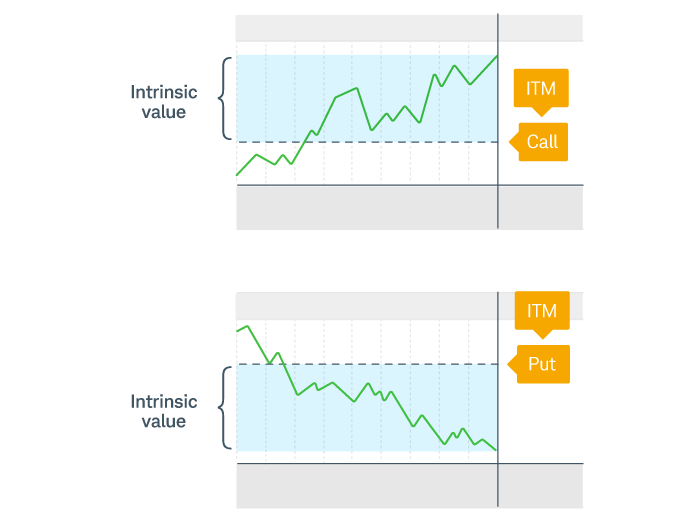

Intrinsic value is the value an option has at expiration, or the value an option would have if it expired right now. You can also think of it as the value that can't be taken away from an option. Intrinsic value is calculated by taking the difference between the strike price and the current price of the underlying security. For example, consider a long call option. A long call has intrinsic value if the strike price is lower than the current price—the intrinsic value is simply the difference between the two. Say ZYX is currently trading for $83. If you owned a long call with an $80 strike price, your option would have $3 of intrinsic value.

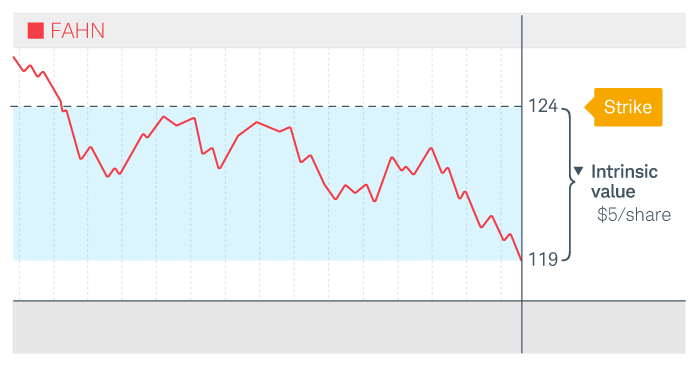

A long put, on the other hand, has intrinsic value if the strike price is higher than the current price of the underlying stock. Say FAHN is currently trading for $119. If you owned a long put with a $124 strike price, your option would have $5 of intrinsic value.

Extrinsic value

Intrinsic value is just one part of the equation. We also need to factor in extrinsic value. This is the value of an option due to time and implied volatility. Along with the price of the underlying stock, these factors represent an options premium's potential to increase in value before expiration. An option with more time to expiration has more time to make a move up or down, which translates to more extrinsic value. Likewise, an option with more implied volatility means the underlying stock is perceived as riskier and, therefore, more likely to make a large move up or down. Once again, this translates to more extrinsic value.

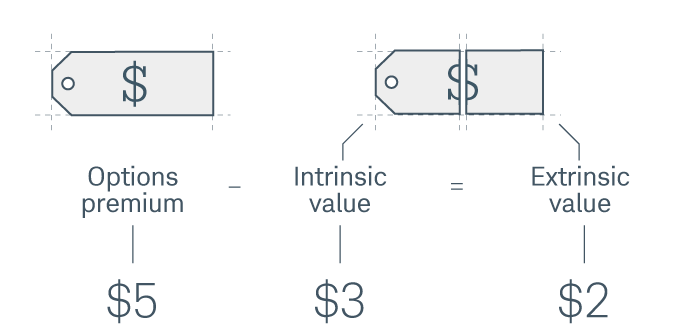

Time and implied volatility are the two primary components of extrinsic value, but factors like interest rates and dividends play a lesser role. Another way to think about it is that extrinsic value is the value that's left over if you subtract intrinsic value from the options premium. Let's look at an example using our same long call on ZYX, which has $3 of intrinsic value. Say this option sold for a $5 premium. To figure out the extrinsic value, subtract the intrinsic value from the premium ($5 – $3), which is $2.

Intrinsic and extrinsic value are important to option traders because they help differentiate between the inherent value of an option and the rest of the value that will melt away by expiration. When you consider that buyers suffer from the loss of extrinsic value while option sellers benefit from this loss, you can see how valuable this information is. As you'll see when we get into the strategies, selecting the option with the right amount of extrinsic or intrinsic value is a necessary step when trading options.

Now, let's look at intrinsic value another way. Depending on how much intrinsic value they have, options are classified as in the money (ITM), at the money (ATM), or out of the money (OTM).

ITM options have intrinsic value. Remember, a call has intrinsic value when the strike price is below the current price, and a put has intrinsic value when the strike price is above the current price.

Moneyness

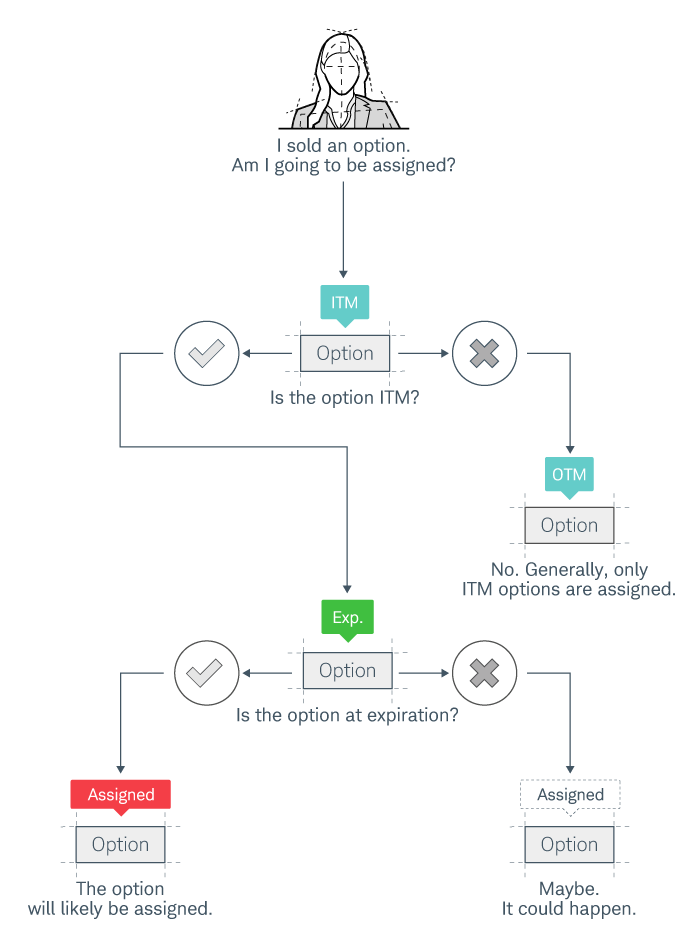

ITM options have intrinsic value and, for this reason, premiums for ITM options are usually more expensive than OTM or ATM options. Also, an option that is currently ITM is more likely to be ITM at expiration than an option that's OTM. Another important consideration for ITM options is that they're more likely to be exercised. This is particularly important when you're an option seller. When an option you've sold has gone ITM, your risk of being assigned increases significantly. Generally, this risk increases as an option approaches expiration and the option has little or no time value. If an option is ITM at expiration, it'll likely be automatically exercised.

Note, however, that if your long option is ITM at expiration and your account doesn't have enough money to support the resulting long or short stock position, your broker may, at their discretion, choose not to exercise the option. This is known as do not exercise, or DNE, and any profit that would’ve been realized by exercising the option is lost. DNEs can also be submitted by any option holder and instruct the broker not to auto exercise ITM options at expiration.

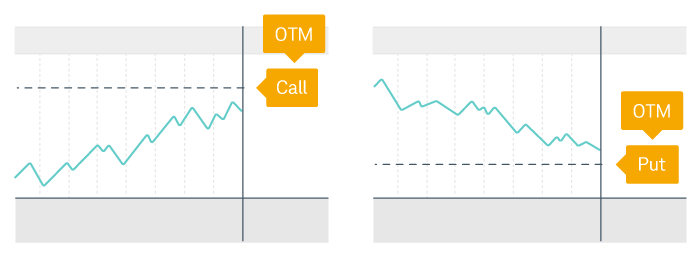

An OTM option has no intrinsic value. A call is OTM when the strike price is higher than the underlying security's current price, and a put is OTM when the strike price is lower than the underlying security's current price. OTM options prices are entirely made up of extrinsic value.

Extrinsic value melts away over time, and options that are OTM at expiration will expire worthless because there is no intrinsic value and no remaining extrinsic value. Likewise, except in rare situations, these options go unassigned.

The premiums for OTM options tend to be less expensive. The further OTM an option is, the cheaper it is, and the more confident traders are that it'll expire OTM. But all options are subject to price risk, or the possibility that the price of the underlying stock could make an unexpected move.

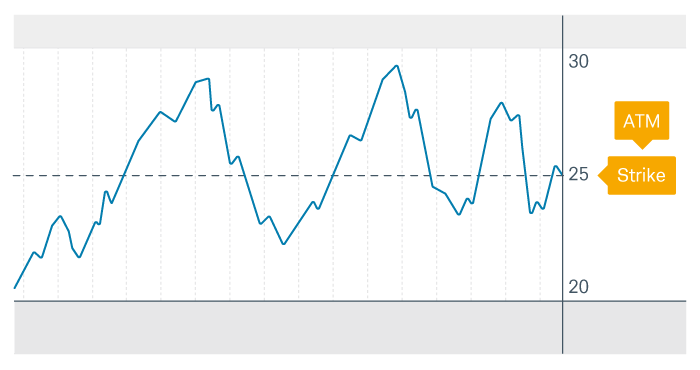

The option with a strike price equal or near the current price of the underlying stock is at the money. An ATM option might be slightly ITM (if the option has intrinsic value) or slightly OTM (if the option has no intrinsic value). If the stock price is exactly equal to the strike price, the contract is ATM and has no intrinsic value.

ATM options have the largest amount of extrinsic value of any option. Because the ATM strike price is the closest to the current market price, there's a lot of uncertainty—it could be ITM or OTM at expiration. However, because these options often have little or no intrinsic value, they tend to have lower premiums than ITM options.

An ATM option may or may not have intrinsic value and, therefore, it may or may not be exercised before or at expiration. Anytime an option has intrinsic value, its risk of being exercised greatly increases. And an option that expires with intrinsic value will likely be automatically exercised. It's worth noting that there are situations where an OTM option is exercised. However, these situations are far from the norm.

The value of an option changes over the life of a trade. Depending on what happens with the price of the underlying asset, an option can start ITM but expire OTM. Or it can start OTM and expire ITM. ITM, OTM, and ATM are helpful quick references that clue option traders into whether an option has intrinsic value and whether it's likely to be exercised.

As we get into specific strategies, you'll learn more about how to anticipate exercise or assignment.