Options Pricing

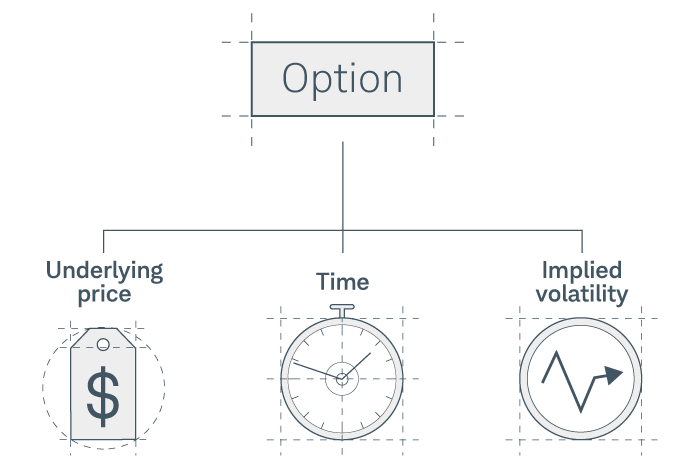

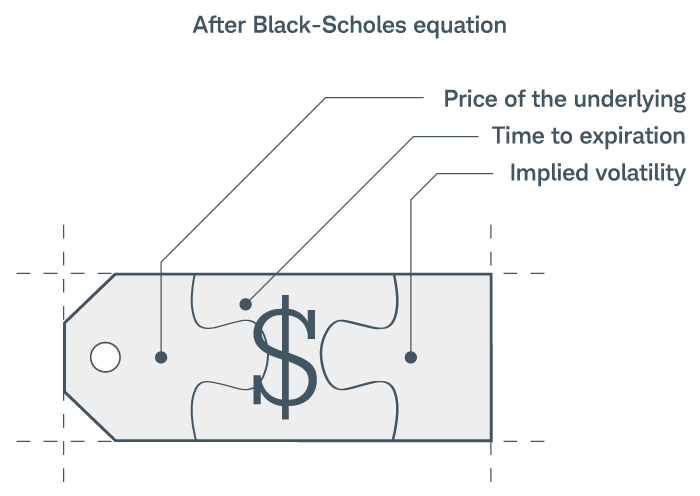

Now, let's figure out how options are priced. By this point, this should be clear: Options pricing is complex and impacted by several factors. The three most important are the price of the underlying security, time to expiration, and implied volatility.

Options pricing 101

It's important for option traders to understand options pricing—after all, if you don't know how your trade might make or lose money, how can you describe your results as anything but luck? We'll begin our investigation into options pricing by examining its history, and then we'll get into the specifics.

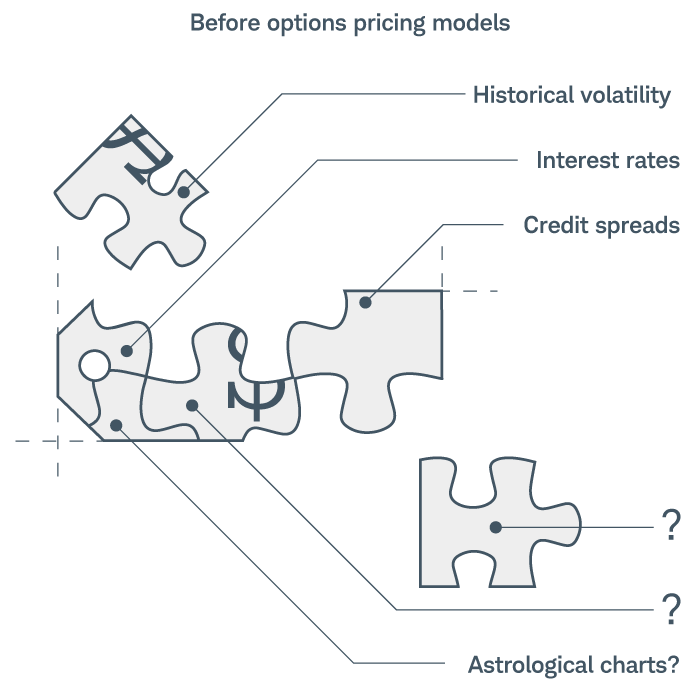

Back in the early days of options trading, options were priced by supply and demand, just as they are today. However, back then, nobody understood why options were priced the way they were. They weren't able to make a lot of sense of it and, instead, thought it was just a result of market forces.

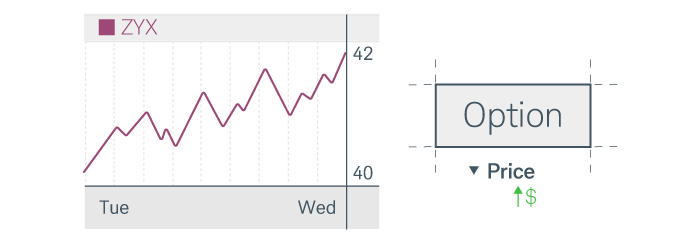

For example, the underlying stock might go up from $40 to $42, causing a small move in the options price.

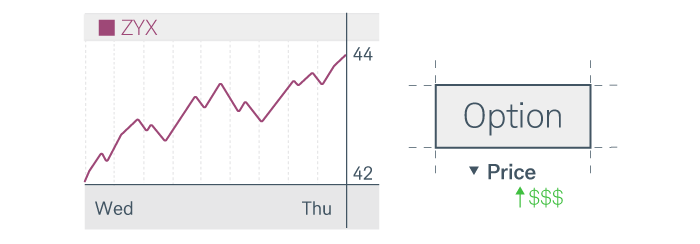

Then, the stock might make another $2 move. However, this time, the options price moved more than it did before. How would one explain or plan for this inconsistency?

These inconsistencies lead to more questions. For example, how would you know how many options to buy to hedge a position? How would you identify a fair price? Perhaps most important, how would you determine which factors mattered to the options price? For example, if the stock market crashed, would that have an impact? How about a stock's recent volatility—would that impact the options price?

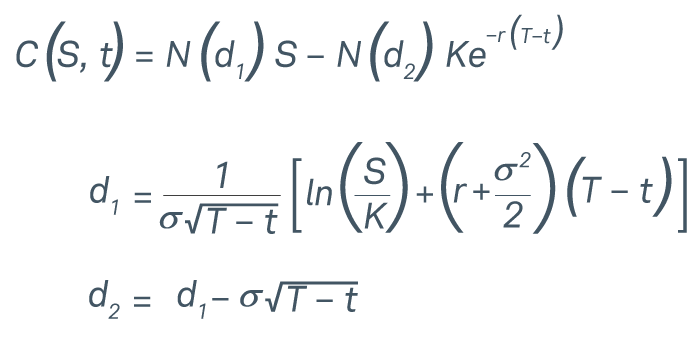

Enter two economists, Fischer Black and Myron Scholes, who published a paper in 1973 with an equation that estimates the price of an option over time. Fittingly, this equation is now known as the Black-Scholes formula, and it describes the relationship between the factors that impact the options price. Black, Scholes, and another economist, Robert Merton, won a Nobel prize in the '90s for their work on options pricing. The Black-Scholes formula is complicated.

However, understanding this formula isn't necessary to trade options. You just need to understand that the formula is the basis for one options-pricing model, which helps identify the main variables that influence the options price: the price of the underlying security, time to expiration, and implied volatility, among other variables.

Price matters most

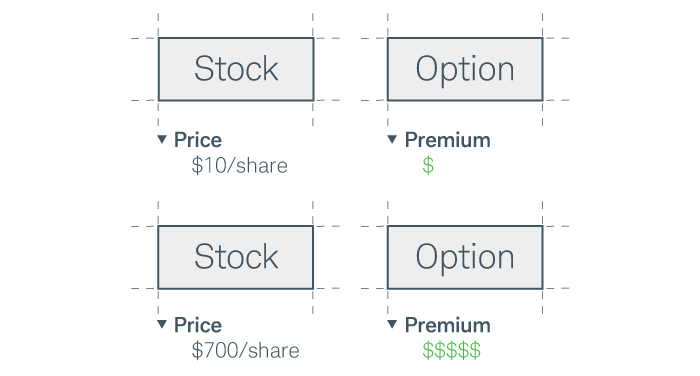

Let's discuss each of these factors, beginning with the price of the underlying stock. Price is often the factor that makes up the majority of an options premium. This makes sense when you consider the leverage inherent to options. Because options allow you to control a large amount of stock (specifically, 100 shares per standard contract), the price of the underlying stock has a big impact on the options price. As you might expect, an option for a stock that's priced at $10 per share is typically less than an option for a stock priced at $700 per share.

Another thing to note about changes in price is that its impact on an options premium isn't linear. For example, the underlying stock may move $1, and you may see the options premium increase $0.30. Then the underlying stock may move $1 more, and you may see the options premium increase $0.38. This nonlinear relationship is common to all aspects of options pricing and, as you'll learn, can be a valuable tool for certain strategies. Later in this lesson, we'll introduce additional concepts that will help you identify specifically how much an options premium might increase or decrease depending on changes in various factors.

Time

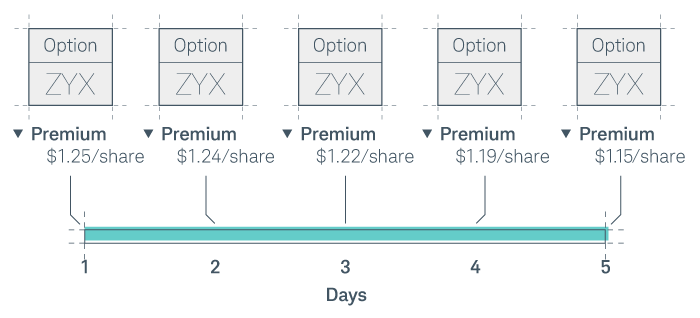

Now, let's examine the next factor that makes up the options premium: time. All options have an expiration date. The amount of time left until expiration is the time value of an option. Options with many months until expiration have a lot of time value, while options with only a few days until expiration have little time value. This is because more time to expiration means more time for the option to possibly become profitable—for which the market is willing to pay more.

Time value slowly erodes every minute of an options contract's life (including weekends). The loss due to the passage of time is often referred to as time decay, which describes the way time value melts as an option nears expiration. Time value doesn't melt at a steady rate either; it melts faster the closer it gets to expiration.

Volatility

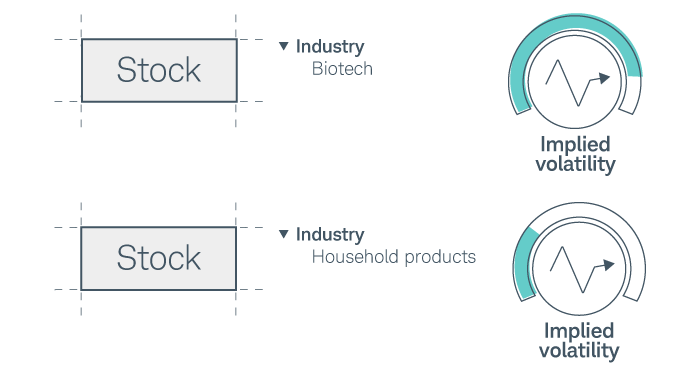

Implied volatility refers to the amount of an options premium attributed to a stock's perceived riskiness. Basically, it estimates how much price movement the market expects in that stock before the options contract's expiration. A stock that's more likely to make a big move in price (up or down) will typically have a higher level of implied volatility, and a stock that's less likely to make a big move has less implied volatility.

Because markets are forward-looking, implied volatility tends to spike before events that can have a big impact on a stock's price like earnings announcements.

The word "implied" refers to how it's calculated. Unlike stock price and time, which can be easily identified, implied volatility is not something you can determine from looking at a stock chart or a calendar. Instead, implied volatility is expressed as a percentage and is calculated by starting with the options price and working backward. Implied volatility is simply what's left over when all other inputs in an options-pricing model are accounted for. As you'll explore further on the next page, options prices are generally set by a market maker. When a market maker adjusts prices up and down due to supply and demand, they're essentially adjusting implied volatility levels. Because of the market maker's role in determining implied volatility, it's often considered a more subjective variable rather than something concrete.

Other factors like interest rates and dividends also impact an options price. But compared to time and implied volatility, they're much less important. That said, it's helpful to understand each factor and how they might impact your trading decisions.

Interest rates and dividends

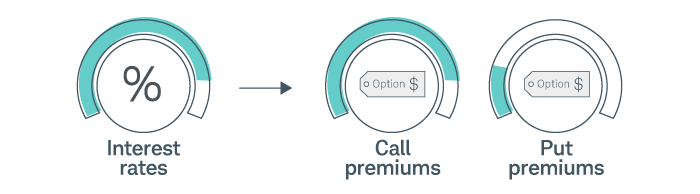

Like almost all securities in the financial world, options are impacted by interest rates. When interest rates rise, call premiums typically increase and put premiums typically decrease.

Here's why: Some investors use call options as substitutes for stocks. When interest rates are high, there's more incentive to buy calls, which are typically a fraction of the stock price, and invest the rest of the money in investments that pay interest, such as money markets or Treasury bills. Therefore, call buyers are willing to pay more when rates are high because they can collect more interest.

For example, if an investor buys 100 shares of a $100 stock, their investment is $10,000, excluding fees. But if they buy two six-month call options for $5 each instead, the investment is $1,000 (2 x $5 x 100). They can take the extra $9,000 and invest in an interest-bearing money market or Treasury bills. If the interest rate is 0.15%, then they'll earn less than $7 in interest over six months (.0015 x $9,000 x (182/365)). However, if the rate is 1%, they'll earn roughly $45 on the $9,000 over six months (.01 x $9,000 x (182/365)). The opportunity cost of buying stock versus call options increases as rates move higher.

Keep in mind that it isn't always appropriate to use options strategies as substitutes for stock-trading strategies because stocks do not expire and sometimes pay dividends. Options strategies have a limited life span and, unlike stock ownership, do not pay dividends or have voting rights.

In general, interest rates have less of an impact on puts than on calls; all else being equal, put premiums will be lower in a high-rate environment. While the opportunity cost of buying stock versus calls increases as rates move higher, the opportunity cost of buying long put options versus selling stock short (where an investor with an approved margin account collects interest on deposited funds) is greater in a high-interest-rate environment than in a low-interest-rate environment. That is, as rates rise, buying puts becomes less attractive compared to the bearish strategy of selling stock short in an interest-bearing margin account.

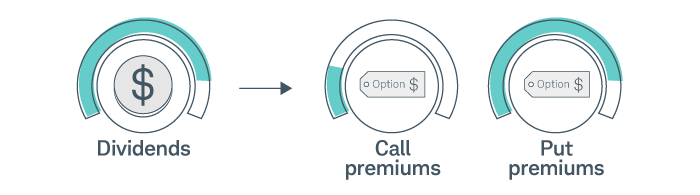

The impact of dividends is similar because it influences whether people prefer owning options or stock. The higher the dividend, the lower the call premium and the higher the put premium.

Let's break this down. When dividends are issued, the stock price drops by approximately the amount of the dividend. The call premium factors in this drop and is lower as a result. The put premium anticipates the lower stock price as well, but it increases as a hedge against the drop.

Dividends also impact the likelihood of assignment. Remember, you only receive dividends if you own the stock the day before the ex-dividend date. If you own a call option for a stock with an upcoming dividend and the ex-dividend date is before expiration, you may choose to exercise early to capture the dividend. For the same reason, if you've sold a call option and the price of the underlying stock is above the strike price, the chance of assignment increases as the ex-dividend date approaches, especially when the dividend payment is greater than the time value remaining in the option. Also, dividends have more of an impact on options with longer expirations than shorter ones because more dividend payments can be distributed during longer time periods. Remember, the risk of assignment is always greater as an option gets closer to expiration.

In the video below, Education Coach James Boyd breaks through the complexity of options pricing by comparing it to something we're all familiar with: car insurance.