Sector Views: Monthly Stock Sector Outlook

Schwab Sector Views is our six- to 12-month outlook for stock sectors, which represent broad sectors of the economy. The Schwab Center for Financial Research (SCFR) combines a factor-based approach with a market and economic assessment to determine the ratings. For the basics on sectors, please see Stock Sectors: What Are They? How Are They Used?

Industrials are supported by increased capital spending in key growth areas like electricity capacity, construction around the artificial intelligence-related (AI) infrastructure buildout, defense, and energy, which also supports Materials. The Health Care sector is expected to benefit from technological advances and improving operational efficiencies, particularly in groups like biotechnology. Communication Services ranks well on fundamental measures but lofty valuations and concerns about high AI spending have increased, contributing to the sector's underperformance relative to the S&P 500 in the second quarter. Energy sector earnings have jumped on higher oil prices driving earnings upgrades. But elevated earnings expectations and valuations are now a risk, especially if there is a near-term resolution to the conflict in Iran. Valuation, defensive characteristics, and low correlation to the increasingly crowded AI trade impacting other sectors add attractiveness to the Consumer Staples sector.

Consumer Discretionary fundamentals have weakened with softer revenue and free cash flow relative to other cyclical sectors (free cash flow is the amount of cash a company has left after spending on operations and capital asset maintenance). Low consumer confidence is also likely to continue impacting the group, which has been the worst-performing sector year to date, according to Bloomberg. Utilities has started to underperform after a strong run that has driven valuations and earnings expectations higher.

Real Estate continues to be challenged by supply imbalances in the commercial office segment, which have been in place since the COVID-19 pandemic in 2020. Even so, the sector has produced double-digit gains year to date, even in the face of potential interest rate increases. Higher interest rates have historically tended to hurt the sector.

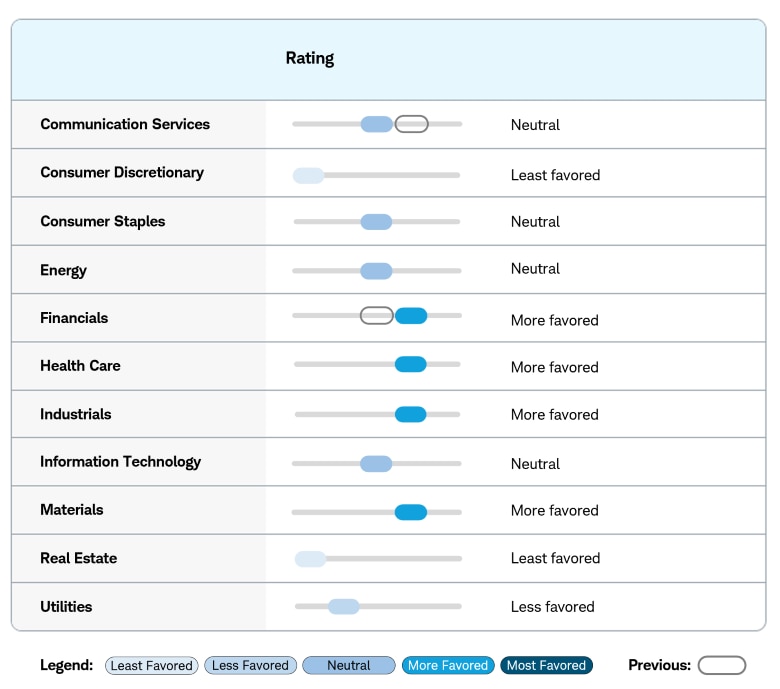

Sector ratings

Source: Schwab Center for Financial Research, as of 7/31/2026.

The ratings Most Favored, More Favored, Neutral, Less Favored and Least Favored reflect SCFR's opinions about the likelihood that the sector will perform better (Most Favored, More Favored), about the same (Neutral), or worse (Less Favored, Least Favored) than the broader S&P 500® index during the next six to 12 months. Sectors are based on the Global Industry Classification Standard (GICS®), an industry analysis framework developed by MSCI and S&P Dow Jones Indices to provide investors with consistent industry definitions. This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. Investing involves risk, including loss of principal.

Sector performance and concentration statistics

| Sectors (in alphabetical order) |

Weighting in S&P 500 (%) |

Trailing six-month performance (%) | Trailing 12-month performance (%) | Weight of 3 largest stocks (%) | Weight of 10 largest stocks (%) |

|---|---|---|---|---|---|

| Communication Services | 9.7 | -6.5 | 14.8 | 78.7 | 96.4 |

| Consumer Discretionary | 9.3 | -10.4 | -1.7 | 61.2 | 77.5 |

| Consumer Staples | 4.6 | 1.8 | 7.3 | 41.5 | 80.4 |

| Energy | 3.0 | 21.3 | 41.7 | 53.7 | 80.4 |

| Financials | 11.8 | 7.2 | 7.1 | 30.8 | 56.6 |

| Health Care | 8.9 | 5.5 | 21.3 | 34.5 | 61.7 |

| Industrials | 8.9 | 11.3 | 19.5 | 18.6 | 39.5 |

| Information Technology | 38.0 | 14.7 | 27.2 | 54.7 | 76.5 |

| Materials | 1.8 | 1.5 | 11.8 | 35.3 | 72.1 |

| Real Estate | 1.8 | 14.3 | 12.9 | 33.3 | 68.1 |

| Utilities | 2.2 | 8.1 | 12.7 | 27.8 | 57.9 |

| S&P 500 index performance for the trailing six or 12 months (%) | 6.8 | 17.4 |

Stock sector commentary

(Sectors are listed in alphabetical order)

Communication Services sector (rating: Neutral)

Positives: The sector is benefiting from growth in digital advertising, data consumption, and streaming services with support from ongoing digitization trends and telecommunications infrastructure investment. An increasingly AI-driven world might result in greater data consumption, which could benefit services providers in the sector.

Risks: Communication Services has a high exposure to advertising, which can be pressured during periods of economic slowdown. The sector is also exposed to competitive pressures in more mature markets like telecommunications and media. Technology disruption is another risk and large capital expenditures for AI may not translate to the strong future earnings that investors expect. The sector continues to be highly concentrated in a few individual stocks, with nearly 80% of the sector's weight attributed to just three stocks, raising idiosyncratic risk. There appear to be increasing concerns that consensus earnings-per-share (EPS) growth expectations may be too optimistic.

Consumer Discretionary sector (rating: Least Favored)

Positives: Structural trends in e-commerce and digital transformation are supporting long-term growth. The sector has benefited from economic expansion and rising consumer spending.

Risks: The sector is highly exposed to economic conditions and thus vulnerable to a slowing economy and reduced consumer confidence and spending. Tariffs and inflation could affect companies' profitability and consumers' discretionary spending. Concentration risk is also high for the sector, as more than 60% of its weight comes from three stocks.

Consumer Staples sector (rating: Neutral)

Positives: Consumer Staples is relatively insensitive to economic cycles and historically has provided stability during economic downturns. It may also provide outperformance during periods of market volatility and uncertainty. The sector's valuation is attractive relative to the broader market, and it has a low correlation to the aforementioned AI trade, which has become even more crowded recently.

Risks: The sector offers limited growth potential compared to cyclical sectors during economic expansion and is highly competitive, which can affect profitability. Tariffs and input cost inflation, especially those due to higher oil prices, can pressure profit margins.

Energy sector (rating: Neutral)

Positives: Energy stocks are generally supported by high oil prices, which have been a factor in the current geopolitical climate and Middle East conflict. Structural demand from the global energy transition and energy security provide support for the sector and is driving investment in production capacity.

Risks: The sector is vulnerable to regulatory changes and policy shifts toward renewable energy and decarbonization. While geopolitical risk can support oil prices, it can also cause supply disruptions and price controls that can be disruptive to earnings. Strong U.S. oil production has weighed on oil prices in recent years and prices could revert lower if geopolitical stress in the Middle East fades. This group is highly concentrated, with the largest three stocks making up over half of the sector's weight.

Financials sector (rating: More Favored)

Positives: Modest increases in interest rates and a steeper yield curve are driving net interest income for banks and insurance company returns on policyholder premium balances. Structural trends in digitalization and financial technology are creating new revenue opportunities. Stronger fundamental conditions are resulting in improved EPS and dividend payouts. The sector has lower valuations relative to the broader markets.

Risks: Financials are highly sensitive to interest rate changes and central bank policy decisions. Interest rate cuts were more widely expected at the start of 2026, but expectations have recently shifted toward a potential rate hike. Cyclical exposure to economic downturns can impact loan quality and credit losses. Financial tightening due to persistently high interest rates and heightened bank risk controls can weigh on growth. The rapid rise in private credit markets and associated products could cause broader financial-system stress. The new Federal Reserve chair could lead to unexpected changes in monetary policy, although after two Kevin Warsh-led meetings, interest rates remain unchanged.

Health Care sector (rating: More Favored)

Positives: Health Care is structurally supported by increasing health awareness, technological innovation, and demographic trends that include an aging population. Relatively steady demand characteristics may provide defensive positioning during economic uncertainty. Health care ETFs have tended to benefit from positive flows lately, particularly in biotechnology.

Risks: Regulatory uncertainty includes potential changes to Affordable Care Act subsidies, Medicaid cuts, tariffs, and pharmaceutical pricing. Subindustries that tend to have weaker fundamentals and are more volatile (like biotechnology) can reduce the attractiveness of the sector. Forward earnings growth is relatively weak given the strong growth expectations in Information Technology and other cyclical sectors like Consumer Discretionary and Industrials. Erosion of consumer purchasing power could negatively impact industry volumes.

Industrials sector (rating: More Favored)

Positives: Industrial demand is broad-based, driven by AI-fueled data center buildouts and higher defense spending. The growth outlook is structurally stronger than in the previous decade, supported by megatrends such as decarbonization, electrification, digitalization, and re-industrialization. The sector attracted the strongest net institutional flows in the first half of 2026.

Risks: The sector has high cyclical exposure to economic downturns. Core end-markets including Residential and Commercial & Industrial are highly sensitive to macroeconomic factors like interest rates, housing starts, and investment cycles. Industrials may underperform if tariffs eventually start to eat into profit margins and the manufacturing sector's recovery takes longer than expected. Airlines are vulnerable to elevated fuel prices. Strong investor interest in the sector has recently driven rapid fund inflows and pushed valuations (which are the highest among the cyclical sectors) to near-record levels.

Information Technology sector (rating: Neutral)

Positives: The sector's fundamental growth is being supported by factors including cloud computing, AI, digital transformation, the shift to electric vehicle and self-driving technology, and demand for labor-saving and automation solutions like robots.

Risks: Growth expectations and valuation have raised the bar for Information Technology (IT) performance. Certain parts of the sector are highly cyclical and vulnerable to shifts in customer sentiment and capital expenditure cycles. Some companies have high-cost bases that can lead to earnings losses in downturns. IT supply chains are under pressure from component shortages and rising input costs.

Materials sector (rating: More Favored)

Positives: The Materials sector is seeing structural demand from infrastructure spending, reshoring, and industrialization trends. A recovery in global manufacturing could be supportive for Chemicals and Basic Resources, while exposure to data center expansion could drive demand for specialty materials. The sector can also outperform during periods of high inflation.

Risks: Materials is a highly cyclical sector with earnings closely tied to global economic growth and industrial production. Commodity price volatility can create earnings unpredictability and margin pressure while trade policy shifts, tariffs, and supply-chain disruptions add to vulnerabilities. Growing bipartisan pushback against and local resident opposition to data center construction could become an issue.

Real Estate sector (rating: Least Favored)

Positives: Real Estate, which consists primarily of commercial real estate investment trusts (REITs), tends to benefit from economic growth, which supports rent collections and property prices. REITs are favored as defensive sectors typically offering earnings resilience during periods of macroeconomic uncertainty. Structural housing affordability and supply constraints can support the long-term case for renting.

Risks: Real Estate is a rate-sensitive sector highly vulnerable to interest rate increases and financing cost pressures. Most REITs borrow heavily, making them vulnerable to elevated interest rates. The sector faces structural headwinds in office and traditional retail segments, and some business models can be disrupted by AI technologies.

Utilities sector (rating: Less Favored)

Positives: Domestic-focused power infrastructure and solar players can benefit from structural growth drivers like AI data center expansion, industrial expansion, and the energy transition. The Utilities sector has non-cyclical demand characteristics providing defensive positioning during economic uncertainty.

Risks: The sector faces regulatory risks affecting rate approvals and return on investment. Utilities generally has higher financing needs due to capital-intensive infrastructure projects and is sensitive to interest rates that impact the cost of capital for long-term investments. The likelihood of rate cuts has decreased, and an interest rate increase in the second half of the year is now more likely, in our view.

How should I use Schwab Sector Views?

Investors should generally be well-diversified across all stock market sectors. You can use the S&P 500 allocations to each sector, listed in the Sector Performance chart above, as a guideline.

Investors who want to make tactical shifts in their portfolios can use Schwab Sector Views ratings as a resource. These ratings can be helpful in evaluating and monitoring the domestic equity portion of a portfolio. These favorability views are our preferences for investment assets relative to their peers shown in each section. The views reflect a six- to 12-month outlook and may change as markets evolve. Views do not guarantee future returns and are not a forecast that an asset will rise or fall. They are not a recommendation. An unfavorable view does not mean the investment should be avoided, nor does a favorable view mean the asset must be included in a portfolio. An asset can be held for diversification, income needs, risk control, tax constraints, etc. We suggest using these views as a guide, incorporating the accompanying rationale and other insights.

The views are positioned across a five-point spectrum: Least Favored, Less Favored, Neutral, More Favored, and Most Favored. The Schwab Center for Financial Research (SCFR) sets these views. The team employs a robust, data-driven approach to guide investors managing cross-asset positions in a globally diversified portfolio. The investment approach incorporates a wide range of quantitative data and qualitative inputs that assess the current market environment relative to historical context.

Schwab clients can log into their accounts and use Schwab's Portfolio Checkup tool to help assess their sector allocations. If they decide to make adjustments, they can use the Stock Screener to research particular sectors. Schwab's ETF Screener and Mutual Fund Screener also can help identify funds that specialize in particular sectors. Before considering any fund, you should consult the fund's prospectus to understand its investment objectives, risks, charges, and expenses. Investors and clients should consider sectors as only a single factor in making their investment decision while considering the current market environment.

About the author