When to Consider Out-of-State Munis

Key takeaways

- One benefit of municipal bonds, or "munis," is that the interest they pay is generally exempt from federal income taxes. They're also generally exempt from state income taxes if the issuer is from the investor's home state.

- Many muni bond investors may benefit from diversifying outside of just investing in munis issued by municipalities in their home state, even if it results in a higher state tax bill.

- We think that muni investors in all states, with the exception of two high-tax states—California and New York—could benefit from investing in a national, not state-specific, portfolio of muni bonds.

- One benefit of municipal bonds, or "munis," is that the interest they pay is generally exempt from federal income taxes. They're also generally exempt from state income taxes if the issuer is from the investor's home state.

- Many muni bond investors may benefit from diversifying outside of just investing in munis issued by municipalities in their home state, even if it results in a higher state tax bill.

- We think that muni investors in all states, with the exception of two high-tax states—California and New York—could benefit from investing in a national, not state-specific, portfolio of muni bonds.

A major benefit of municipal bonds, or "munis," is that the interest they pay is generally exempt from federal income taxes. They're also generally exempt from state income taxes if the issuer is from the investor's home state. That may seem like a compelling argument for sticking with in-state munis. However, many muni investors may benefit from diversifying outside of their home state, even if it results in a higher state tax bill.

We've identified five factors when it could make sense to consider munis from other states. After considering all five, we think that muni investors in all states, with the exception of two high-tax states—California and New York—could benefit from investing in a national, not state-specific, portfolio of muni bonds. There may be instances where even investors in California or New York who are not in a high state tax bracket could achieve higher after-tax yields by diversifying nationally.

1. You live in a state with low or no state income tax.

If you live in a state with low or no state income tax, you will likely benefit from diversifying your muni portfolio with munis from issuers outside your home state.

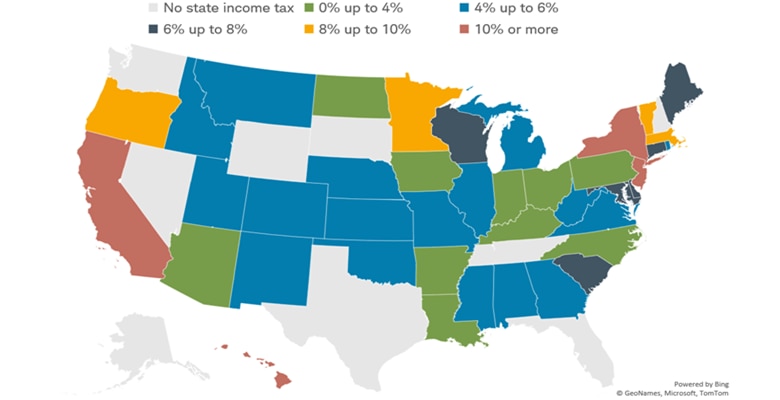

The map below shows the maximum marginal income tax rate by state for married taxpayers filing jointly.

Investors in states with low or no state income tax could benefit from out-of-state munis

Source: Tax Foundation, as of 2/17/2026.

Assumes the top tax rate for a married-filing-jointly filer. Does not include phaseouts or other exemptions or deductions, which could result in a different marginal tax rate. Local income taxes are not included. Washington state has no income tax but does tax capital gains when income exceeds certain limits, with the top capital gains tax rate being 9.9%. For illustrative purposes only.

For investors in states with no state income taxes, like Florida or Texas, there's no state tax benefit to staying within your home state. For investors in California, on the other hand, the benefit can be large because the state tax rate is the highest in the country—13.3% for the top bracket. Therefore, it may make more sense if you're in a high-income-tax state to buy bonds issued in your home state, all else being equal.

In some instances, some states tax in-state bonds in the same manner they tax out-of-state bonds. For example, bonds issued by municipalities in Illinois are often subject to state income taxes—even if the tax filer is a resident of Illinois. In other words, Illinois investors don't necessarily save on their state income tax bill by holding Illinois munis. The rules can get complicated at times, so it makes sense to consult with your tax advisor.

2. You could earn a higher yield, even without state tax breaks.

Some out-of-state muni bonds offer higher yields than in-state munis, even after accounting for any state income taxes.

It depends on where you look, though. The table below shows the yields investors in certain states would have to earn on out-of-state munis compared with the yield on an index of five-year general obligation munis issued by their home state to compensate for the lack of state income tax breaks. This assumes the investors are in their home states' highest marginal state tax bracket. The difference in yield is expressed in basis points (a basis point is one hundredth of one percent, or 0.01%). Florida and Texas, and Washington don't have state income taxes, so there's no spread.

Investors in various states would have to earn higher yields on out-of-state munis to make up for a lack of state income tax breaks

| State | Yield on a 5-year state GO (%) | Top marginal tax rate | State GO credit rating | Required out-of-state yield (%) | Difference in basis points |

|---|---|---|---|---|---|

| California | 2.59 | 13.30% | Aa2/AA- | 2.99 | 40 |

| New York | 2.45 | 10.90% | Aa1/AA+ | 2.75 | 30 |

| Texas | 2.78 | 0.00% | Aaa/AAA | 2.78 | 0 |

| Illinois | 3.13 | 4.95% | A3/A- | 3.30 | 17 |

| Florida | 2.68 | 0.00% | Aaa/AAA | 2.68 | 0 |

| Pennsylvania | 2.77 | 3.07% | Aa2/A+ | 2.85 | 8 |

| Massachusetts | 2.67 | 9.00% | Aa1/AA+ | 2.93 | 26 |

| New Jersey | 2.79 | 10.75% | A1/A | 3.12 | 33 |

| Washington | 2.74 | 0.00% | Aaa/AA+ | 2.74 | 0 |

| Ohio | 2.71 | 2.75% | Aaa/AAA | 2.79 | 8 |

| Yield for 5-year national index | 3.03 |

For example, the yield on an index of five-year general obligation bonds issued by the state of California is currently 2.59%. An investor in the highest marginal state tax bracket (which, in California, is 13.3%) would have to earn a yield of at least 2.99%—or 40 basis points more—on a bond from outside of California to achieve the same after-tax yield as on the in-state bond. It may be possible to achieve this higher yield if you invest in a bond issued by the state of Illinois, for example. However, Illinois has a lower credit rating than the state of California, and lower ratings imply higher credit risk.

Using a different example, an investor in the top marginal state tax bracket in Massachusetts would need to earn a yield of at least 2.93% to achieve the same after-tax yield as on the in-state muni. That's possible by investing in a nationally diversified index of munis with a similar maturity. However, the nationally diversified index may also contain lower-rated issuers, so it may not be a perfect apples-to-apples comparison.

3. You live in a state with few choices.

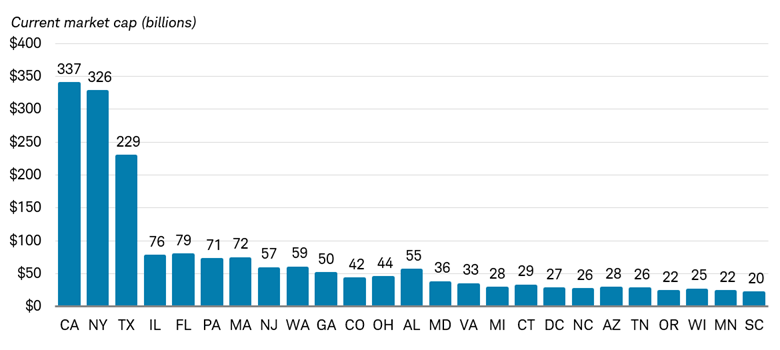

We generally suggest holding at least 10 different bonds from issuers with dissimilar credit characteristics to create sufficient diversification in a portfolio of individual bonds. This could be difficult if your home state has a relatively small number of issuers with similar risks, but easier to achieve in larger states such as California, New York, and Texas, which have many issuers. In fact, bonds from California, New York, and Texas account for approximately 44% of all issuers in the Bloomberg U.S. Municipal Bond Index. But in-state diversification is difficult for smaller states—as the chart below shows, many states have a small number of issuers based on the market value of bonds outstanding.

Bonds from California, New York, and Texas account for the vast majority of munis outstanding

Source: State indices for the Bloomberg Municipal Bond Index, as of 7/9/2026.

Only the top 25 states, based on market value of the indices, are shown. The Bloomberg Municipal Bond Index (LMBITR) is a benchmark for the USD-denominated long-term tax-exempt investment-grade municipal bond market.

For illustrative purposes only.

4. You may find more highly rated issuers by searching nationally.

We suggest focusing on an average credit rating of AA/Aa for an attractive balance of risk and reward in today's environment. That means having some lower-rated (A/a or below) munis, but the bulk of the munis in your portfolio should carry higher ratings. It's easier to find highly rated munis if you live in a state like California, New York, or Texas, where there are large numbers of bonds rated in the AAA and AA categories. It's more difficult if you live in a state like Illinois, Pennsylvania, or New Jersey, where the majority of bonds are lower than AA rated. Consider diversifying nationally if you live in a state with fewer highly rated options.

5. You live in a state where issuers face similar risks

There are approximately $4.4 trillion of muni bonds outstanding1 spread among tens of thousands of issuers, and the credit quality of each state and issuer is affected by different factors. Even if you live in a state with many highly rated issuers, it could be beneficial to diversify nationally because those highly rated issuers may be subject to similar credit risks, such as economic, political, and demographic risks. Credit quality is generally stronger in areas with steadily increasing populations, skilled workforces, and diverse economies.

Although historically it has been rare for municipalities to fail to pay interest or make principal payments on time, it does occur occasionally. If the conditions in your home state, or regions of your home state, aren't favorable, other states' bonds might be more appealing.

Summing it all up

Considering all five factors, we generally suggest investors in all states other than New York and California consider munis outside of their home state. Investors in higher tax brackets in California and New York may benefit from investing in an all-in-state portfolio because of high state income tax rates and access to many different issuers with different credit risks. However, even investors in New York and California who are not in high state income tax brackets could achieve higher after-tax yields combined with greater diversification by diversifying nationally.

As always, your individual situation may vary. So choose a single-state muni or nationally diversified portfolio of munis based on your needs and situation.

Schwab clients can log in to research individual municipal bonds, view pre-screened municipal bond exchange-traded funds (ETFs) on Schwab's ETF Select List® or municipal bond mutual funds on Schwab's Mutual Fund OneSource Select List®. For additional help in selecting an appropriate solution for your needs, a Schwab Financial Consultant or Fixed Income Specialist can help.

1Source: Bloomberg, as of 7/10/2026.

About the author