ETF trading and liquidity

Introduction

“Liquidity” is broadly defined as the relative ease with which a security can be bought or sold without impacting its price. For individual stocks, liquidity is often defined by trading volume and the bid/ask1 spread. High trading volumes and narrow spreads indicate that a stock can be bought or sold in significant volume without impacting (or moving) its price. But in the case of exchange-traded funds (ETFs), because of their unique structure, trading volume isn’t the only—or even primary—indicator of liquidity. Uncovering the full measure of ETF liquidity requires a deeper dive into the mechanics of the creation and redemption process and the role of authorized participants (APs) and market makers.

Sources of ETF liquidity

It’s frequently heard that ETFs trade “just like” stocks. While it’s true that both ETFs and stocks trade on exchanges during trading hours, there are key differences between the two in terms of what drives trading, liquidity, and pricing.

Multiple layers of market liquidity

Individual stocks tend to have a static number of shares in circulation. The price of the stock at any given moment is determined by the forces of supply and demand. More buyers than sellers will push the price up and vice versa. For this reason, average daily trading volume is generally a clear indicator of stock liquidity.

While an ETF is bought and sold on a national stock exchange (and other secondary market venues), a lower than average daily trading volume does not necessarily indicate limited liquidity. As with a traditional mutual fund, the number of shares of an ETF in circulation can change on any trading day as a result of the product’s open-ended structure—meaning that shares can be added or subtracted to balance supply and demand in the market.

Key terms

- Authorized participants (APs): Large institutions that transact directly with the ETF issuer to create or redeem shares of an ETF.

- Market maker: Large institutions that help maintain an orderly market by selling and buying ETF shares from potential buyers and sellers. For larger trades, a market maker may decide an AP is needed in order to create or redeem shares.

- Creation unit: The minimum number of ETF shares required to transact directly with the ETF issuer. This is typically at least 25,000 shares.

- Primary market: The direct exchange of securities for shares of an ETF between APs and ETF issuers.

- Secondary market: The national markets system (e.g., the stock exchanges and other venues where listed securities can be traded). Shares of ETFs are continuously bought and sold throughout the day on an exchange or other trading venue by investors.

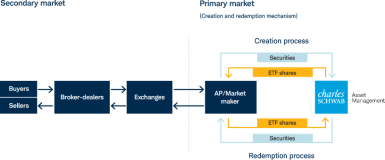

Creation and redemption: Primary liquidity

The creation and redemption process is restricted to large broker-dealers known as APs. They effectively act as wholesalers for the ETF, transacting directly with the ETF issuer—often referred to as “the primary market”—and making shares of the ETF available to investors in smaller quantities through stock exchanges—sometimes referred to as the “secondary market.” AP transactions with an ETF issuer are done in bulk amounts, known as “creation units,” typically containing at least 25,000 shares.

An ETF that is thinly traded on an exchange (otherwise known as the secondary market) does not necessarily indicate limited liquidity. That’s because ETFs combine many of the same attributes of traditional mutual funds and individual stocks to provide investors with two levels of liquidity: primary and secondary.

To create additional shares of an ETF, an AP typically will purchase all the securities that constitute the ETF in appropriate proportion to the overall portfolio and will then exchange this “basket” of securities with the ETF issuer for one or more creation units of the ETF.

To redeem shares of an ETF, an AP will accumulate enough shares of the ETF to constitute at least a creation unit and will then exchange them with the ETF issuer for a basket of securities of equivalent value.

How ETF shares are created, traded, and redeemed

Arbitrage is the key to fair prices

APs engage in the creation and redemption process for one of two primary reasons: (1) to capture commissions from an ETF market maker who is not an AP but wants to buy or sell ETF shares in bulk or (2) to earn a profit by selling ETF shares at a premium to the value of the basket of securities purchased to create new shares (or the opposite transaction—buy the ETF shares at a discount to its value, and receive the basket of securities).

This second reason, known as “arbitrage,” is defined as making a profit by trading similar products at different prices. This profit opportunity, unique to ETFs, is essential for ensuring that an ETF’s share price in the secondary market remains tightly correlated to the value of the securities held in the ETF portfolio itself—the ETF’s intrinsic fair value.2

To the extent that the ETF share price strays from the fair value of the portfolio securities, APs will arbitrage the difference.

An additional layer of liquidity

An ETF should always be at least as liquid as its underlying holdings. The primary market (i.e., the buying and selling of an ETF’s portfolio of securities to support the creation and redemption process) determines the product’s minimum liquidity level. Trading daily on an exchange provides an additional level of liquidity due to the natural daily trading activity that occurs in this secondary market.

Summary

Although transactions in both primary and secondary markets can have significant impact on the liquidity of an ETF, other factors should be considered as well, such as the market environment and the periodic imbalance of buyers and sellers. To determine the liquidity of an ETF, investors must look beyond the volume of ETF shares being traded and understand the unique creation and redemption mechanism of ETFs that allows shares to adjust to market demand.

Explore more ETF insights

Discover ETF Know:How

Browse our full-spectrum curriculum of ETF tools and resources designed to help you boost your knowledge and gain a competitive advantage.

Explore Schwab ETFs

Help your clients get exceptional value from their investments with the product finder.