Fixed income ETFs: Understanding premiums and discounts

Introduction

Investors are drawn to fixed income exchange-traded funds (ETFs) for many reasons, including diversification, liquidity, transparent pricing, and ease of trading. In this article, we explore a key concept of ETF mechanics: premiums and discounts.

When prices diverge

Premiums and discounts can arise when an ETF’s trading price diverges from its calculated net asset value (NAV). In the fixed income ETF marketplace, certain elements can make this more likely, including supply and demand in the secondary market, liquidity and volatility in the relevant bond market, transaction costs (arbitrage and creation), and timing differences. Let’s take a closer look at what influences premiums and discounts in fixed income ETFs.

Key terms

While there are benefits to adding fixed income to a portfolio, there are risks, which include:

- Arbitrage: Buying and selling an asset simultaneously in different markets to take advantage of differences in its price

- Authorized participants: Large institutions that transact directly with ETF issuers to create or redeem shares of an ETF

- Discount: When an ETF is trading at a lower price than its NAV

- Premium: When an ETF is trading at a higher price than its NAV

Market characteristics and liquidity

Fixed income ETFs trade on an exchange with publicly accessible prices, while the underlying securities of the ETF trade privately in the over-the-counter market. Because the underlying securities trade over-the-counter and not on the secondary market like stocks, current prices of these underlying securities may be hard to obtain, which could make it more difficult to quickly identify if an arbitrage opportunity exists. Therefore, a premium or discount may persist in the ETF.

In arbitrage, authorized participants (APs) earn a profit by selling ETF shares at a premium to the value of the basket of securities purchased to create new shares (or by selling the basket of securities at a premium to the value of the ETF shares purchased to redeem shares).

This profit opportunity, unique to ETFs, is essential for ensuring that an ETF’s share price in the secondary market remains tightly correlated to the value of the securities held in the ETF portfolio itself. To the extent that the ETF share price strays from the fair value of the portfolio securities, APs will arbitrage the difference. However, if current prices are hard to obtain, the premium or discount may persist in the ETF, as the arbitrage opportunity may not be easily identified.

Consider municipal bonds, for example, which may sometimes go weeks or even months between each trade. Calculating a NAV requires a daily valuation. Bond pricing services may provide daily valuations that use evaluative models or dealer surveys to estimate a bond’s daily price based on recent trades in similar bonds. However, these pricing services are only as timely as their inputs. If similar bonds don’t trade, the models’ daily price may not reflect the price at which the bond could trade. The uncertainty and price of the bond is reflected in the premium or discount.

During periods of high volatility and low liquidity, APs may not be able to act on an arbitrage opportunity and an ETF’s premium or discount may grow to be wider than in typical markets. These periods are often referred to as an illiquid market or a stressed market—in which there are more sellers than buyers. In these markets, larger-than-normal premiums or discounts can be prevalent, prices may decline rapidly, and ETFs may trade at a discount to the NAV. The discount arises due to the challenge of pairing the over-the-counter bond pricing with the transparency of ETF trading. Simply put, APs do not know if they can liquidate the basket of bonds redeemed from an ETF at the prices the ETF values the basket.

Transaction costs

Investors can better evaluate fixed income ETFs by understanding attributes that influence their pricing, such as arbitrage costs and creation costs.

Arbitrage. As an ETF’s share price drifts from the fair value of its portfolio securities, APs will arbitrage the difference. If the difference isn’t large enough to trigger an arbitrage opportunity, the ETF’s trading price will continue to differ from its calculated NAV as a premium or a discount. The size of the premium or discount will be constrained by the transaction costs APs would incur in performing the arbitrage transaction. If the premium or discount is less than these transaction costs, there is no economic incentive to execute the arbitrage transaction.

Creation. Costs of creating new fixed income ETF shares are a component of fixed income ETF premiums. A common ETF creation methodology, known as “in-kind,” is where an AP exchanges bonds to the ETF provider in exchange for ETF shares, and costs are associated with the AP acquiring the bonds in the market. Over time, liquidity may change for the bonds, which can change the transaction costs. This in turn increases creation costs for the ETF share, which could be reflected in the ETF premium.

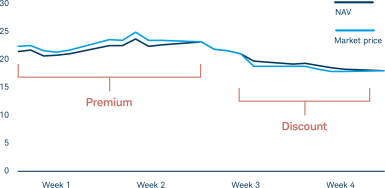

In this hypothetical example, which is for illustrative purposes only, we see the theoretical ETF traded at a premium to NAV earlier in the month. Later in the month we see the ETF trading at a discount to NAV.

Market price at a premium/discount to NAV

Timing difference

Timing difference refers to the discrepancy between when the trading day ends for ETFs versus when fixed income holdings are priced for the daily NAV. For example, most indices and fixed income funds will value underlying holdings for a fixed income ETF at 3 p.m. ET, but the ETF continues to trade until 4 p.m. ET. This means that price movements and discrepancies may occur, and the ETF’s trading price may diverge from its calculated NAV.

One hour time difference may affect premiums and discounts

Summary

The value of the underlying portfolio, the level of supply and demand in the secondary market, costs of share creation, volatility and liquidity in the bond market, and timing differences can all affect an ETF’s premium and discount.

Bringing the over-the-counter bond markets to an exchange through ETFs can make pricing discrepancies visible to investors, which is not necessarily a bad thing. Discounts and premiums don’t necessarily mean that a fixed income ETF is priced incorrectly. Indeed, the structure and transparency of fixed income ETFs can aid in price discovery for the underlying bonds themselves—making an ETF’s market price perhaps another gauge of the total value of the underlying bonds.

Explore more ETF Insights

Discover ETF Know:How

Browse our full-spectrum curriculum of ETF tools and resources designed to help you boost your knowledge and gain a competitive advantage.

Explore Schwab ETFs

Help your clients get exceptional value from their investments with the product finder.